ARCHIVED – Canada’s Energy Future 2018 Supplement: Natural Gas Production

This page has been archived on the Web

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please contact us to request a format other than those available.

Canada’s Energy Future 2018 Supplement: Natural Gas Production [PDF 1706 KB]

Data and Figures [EXCEL 6929 KB]

May 2019

Copyright/Permission to Reproduce

ISSN 2369-1476

Table of Contents

Chapter 1: Background

The National Energy Board’s (NEB) Energy Futures (EF) series explores how possible energy futures might unfold for Canadians over the long term. EF analyses consider a range of impacts across the entire Canadian energy system. In order to cover all aspects of Canadian energy in one supply and demand outlook, the extensive crude oil, natural gas, and natural gas liquids (NGL) production analyses are described at a relatively high level. A series of supplemental reports is able to address impacts specific to the supply sector, creating an opportunity to provide additional detail.

Natural gas prices are a key driver of future natural gas production and a key uncertainty to the projections in the Canada’s Energy Future 2018: Energy Supply and Demand Projections to 2040 (EF2018). Natural gas prices could be higher or lower depending on demand, technology, geopolitical events, and the pace at which nations enact policies to reduce GHG emissions

EF analysis assumes that over the long term, all energy produced, will find markets. The timing and extent to which particular markets emerge, whether demand growth over/undershoots local production, whether export/import opportunities arise, and whether new transportation infrastructure is built, are difficult to predict. This is why simplifying assumptions are made. The analysis in this supplemental report continues the EF tradition of assuming these short–term disconnects are resolved over the longer term.

The EF series of natural gas, crude oil, and natural gas liquids (NGL) supplement reports include four EF cases.

Table 1.1 EF2018 Natural Gas and Crude Oil Production Assumptions/Cases

| Variables | Reference | High Price | Low Price | Technology |

|---|---|---|---|---|

| Oil Price | Moderate | High | Low | Moderate |

| Gas Price | Moderate | High | Low | Moderate |

| Carbon Price | Fixed nominal C$50/t | Fixed nominal C$50/t | Fixed nominal C$50/t | Increasing CO2 cost reaching nominal C$336/t in 2040 |

| Technology Advances | Reference assumption | Reference assumption | Reference assumption | Accelerated |

| Notes | Based on a current economic outlook and a moderate view of energy prices | Since price is one of the most influential factors in oil and gas production, and varies over time, the effects of significant price differences on production are analyzed | Considers the impact of greater adoption of select emerging energy technologies on the Canadian energy system, including technological advances in oil sands production; and the impact on the Canadian energy system of higher carbon pricing | |

This natural gas production supplemental report includes a detailed look at the Reference Case, followed by results from the other three cases. In the Technology Case, technological advances focus on oil sands production and not natural gas; therefore, natural gas prices are assumed to be the same in the Technology Case. The natural gas price assumptions in the High and Low Price cases differ significantly from the other cases.

All cases have the same assumption for liquefied natural gas (LNG) exports from British Columbia (B.C.)’s coast. LNG exports start at 0.75 billion cubic feet per day (Bcf/d) in 2025 and double in 2026 to reach 1.50 Bcf/d. Additional volumes are assumed in 2030, increasing total LNG exports to 2.25 Bcf/d in 2030 and 3.0 Bcf/d in 2031. Figure 2.5 in EF2018 shows the assumed LNG export volumes. Additional natural gas production from LNG exports leads to additional NGL production.

The Appendix includes a description of the methods and assumptions used to project natural gas production, and detailed data sets for all cases – including annual wells drilled, production decline curve parameters, and monthly production, all by stratigraphic and geographic grouping. The Appendix is available in this document, and the data from the Appendix and chart data in this supplemental report is also available [EXCEL 6929 KB].

Chapter 2: Reference Case

2.1 Production by Type of Gas

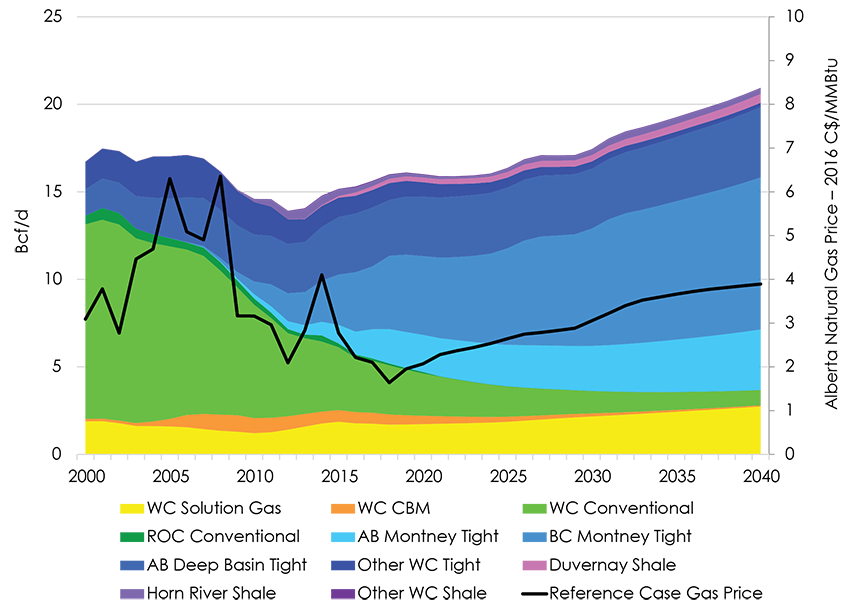

- Canadian gas production has remained steady in the last few years despite declining gas prices since 2014 (Figure 2.1). This was driven by, in part, drilling to evaluate gas resources expected to supply LNG exports off Canada’s West Coast. Meanwhile, new gas–processing plants helped debottleneck some gas–gathering systems. Most importantly, however, natural gas liquids in some gas plays drove gas drilling and production despite low gas prices, while the cold winter of 2017–18 increased seasonal demand. Production is expected to remain steady to 2025 as low, western Canadian natural gas prices persist in the near term and are slowly alleviated by 2025 as infrastructure is built. After 2025, when LNG exports are assumed to begin, production starts to increase as gas pricesFootnote 1 rise and additional drilling to supply LNG exports occurs. Historical production in Canada peaked in 2001 at 495 million cubic metres per day (10 6m3/d) or 17.5 billion cubic feet per day (Bcf/d); in 2017 production was 442 10 6m3/d (15.6 Bcf/d) and by 2040 it’s projected to increase by 34% to 593 10 6m3/d (20.9 Bcf/d).

- Production from the Montney Formation, a large gas resource extending from northeast B.C. into northwestern Alberta, has grown significantly over the past six years. Production of Montney tight gas increased from no production prior to 2006 to almost 149 10 6m3/d (5.3 Bcf/d) in 2017, or 34% of total Canadian natural gas production. The majority of Canadian production growth over the projection period comes from the Montney, with its production reaching 344 10 6m3/d (12.1 Bcf/d) in 2040, or 58% of total Canadian gas production. The majority of gas that will supply LNG exports is assumed to be sourced from the Montney, leading to faster production growth around 2025 and 2030, as seen in Figure 2.1.

- The Alberta Deep Basin – a tight gas play which flanks the Alberta foothills – produced 95 10 6m3/d (3.4 Bcf/d) in 2017. Production grows modestly as natural gas and NGL prices increase, reaching 114 10 6m3/d (4.0 Bcf/d) by 2040.

- The Duvernay and Horn River Basin shale gas plays currently produce small amounts of natural gas, and production from both grows modestly over the projection period. The Duvernay is an emerging shale play in Alberta that contains natural gas, NGLs and crude oil. The Horn River in northeastern B.C. is more established, but the formation lacks NGLs, and is currently uneconomic to drill. However, a small amount of the gas to be exported as LNG is assumed to come from Horn River Basin, and the slight increases in production can be seen in Figure 2.1. Combined, production from the two plays increases from 14 10 6m3/d (0.5 Bcf/d) in 2017 to 24 10 6m3/d (0.9 Bcf/d) in 2040, with the Duvernay making up 60% of the total in 2040.

- Production from conventional and coalbed methane natural gas resources – which do not rely on horizontal drilling and multi–stage hydraulic fracturing – declines steadily over the projection period as new drilling in them is uneconomic using Reference Case price assumptions. Western Canadian (WC) conventional production – not including solution gas – made up 55% of total production in 2006 and 23% in 2017; it continues declining to 4% in 2040.

- Solution gas production is based on Reference Case oil production from conventional, tight, and shale oil production (Canada’s Energy Future 2018 Supplement: Conventional, Tight, and Shale Oil Production). It increases gradually over the next 25 years, making up 13% of total Canadian production in 2040.

- Production from the Rest of Canada (ROC) is minimal over the projection period and is discussed in more detail in the next section.

Figure 2.1 Reference Case Production and Gas Price

Note: WC = Western Canada (British Columbia, Alberta, Saskatchewan, Manitoba)

Description:

This graph breaks down the Reference Case projection for Canadian marketable natural gas production by area and type of gas, and also includes the Alberta natural gas price. Western Canada solution gas is projected to increase from 1.76 Bcf/d in 2017 to 2.74 Bcf/d in 2040. Western Canada CBM is projected to decrease from 0.63 Bcf/d in 2017 to 0.07 Bcf/d in 2040. Western Canada conventional is projected to decrease from 2.96 Bcf/d in 2017 to 0.87 Bcf/d in 2040. Rest of Canada conventional production is projected to decrease from 0.14 Bcf/d in 2017 to less than 0.003 Bcf/d by 2040. Alberta Montney tight gas production is projected to increase from 1.67 Bcf/d in 2017 to 3.46 Bcf/d by 2040. British Columbia Montney tight gas production is projected to increase from 3.59 Bcf/d in 2017 to 8.69 Bcf/d in 2040. Alberta Deep Basin tight gas is projected to increase from 3.37 Bcf/d in 2017 to 4.01 Bcf/d in 2040. Other western Canada tight gas is projected to decrease from 0.99 Bcf/d in 2017 to 0.25 Bcf/d in 2040. Duvernay shale gas is projected to increase from 0.22 Bcf/d in 2017 to 0.51 Bcf/d in 2040. Horn River shale gas is projected to increase from 0.26 Bcf/d in 2016 to 0.33 Bcf/d in 2040. Other western Canada shale gas is projected to decrease from 0.04 Bcf/d in 2017 to 0.01 Bcf/d in 2040. Total Canadian natural gas production is projected to increase from 15.62 Bcf/d in 2016 to 20.94 Bcf/d in 2040. The Alberta natural gas price, in 2016 Canadian dollars per MMBtu, is projected to increase from $2.10 in 2017 to $3.89 in 2040.

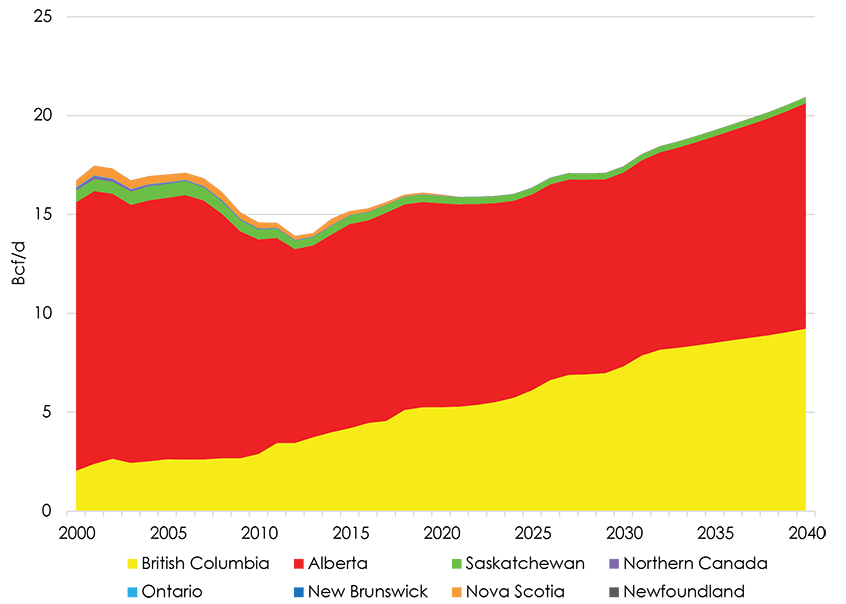

2.2 Production by Province

- Alberta continues to be the largest natural gas producer, though B.C.’s share increases over the period as Montney production grows (Figure 2.2). Saskatchewan gas production, which is mostly solution gas (see Appendices C1–C4 [EXCEL 6929 KB] for gas production by grouping), declines slightly then gradually increases over the projection period.

Figure 2.2 Reference Case Production by Province

Description:

This graph breaks down the Reference Case projection for Canadian marketable natural gas production by province. British Columbia natural gas is projected to increase from 4.56 Bcf/d in 2017 to 9.22 Bcf/d in 2040. Alberta production is projected to go from 10.53 Bcf/d in 2017 to 11.41 Bcf/d in 2040. Saskatchewan is projected to go from 0.40 Bcf/d in 2017 to 0.30 Bcf/d in 2040. Northern Canada is expected to decrease from approximately 0.01 Bcf/d in 2016 to less than 0.002 in 2040. Ontario is projected to decrease from approximately 0.01 Bcf/d in 2017 to almost zero by 2040. New Brunswick is projected to decrease from approximately 0.01 Bcf/d in 2017 to almost zero in 2040. Nova Scotia is projected to decrease from 0.12 Bcf/d in 2017 to zero by 2021. Newfoundland has no marketable natural gas production.

- Natural gas production in Atlantic Canada continues to decline over the projection period. Onshore natural gas production in New Brunswick falls to near zero by 2040. Offshore natural gas production in Nova Scotia is assumed to decline steadily and ceases at the end of 2020 for both the Deep Panuke and Sable projectsFootnote 2. Given relatively high costs for offshore exploration and current provincial policies for onshore gas exploration, no new Atlantic Canada gas fields are projected to come online.Footnote 3

- Ontario and northern Canada natural gas production continue to decline over the projection period. Northern Canada’s natural gas production at Norman WellsFootnote 4 stopped in February 2017 after the line that carries Norman Wells oil south, Line 21, was shut down after a riverbank near Fort Simpson became unstable. The line has since been approved to re-open, and production is expected to re-start with an estimated time of January 2019. Gas production out of Norman Wells is estimated to be at the level it was before the shutdown, and then declines over the projection.

- Significant natural gas resources exist outside western Canada (see section 2.5), but are not projected to be developed over the projection period given economics, distance to markets, drilling moratoriums, and other factors.

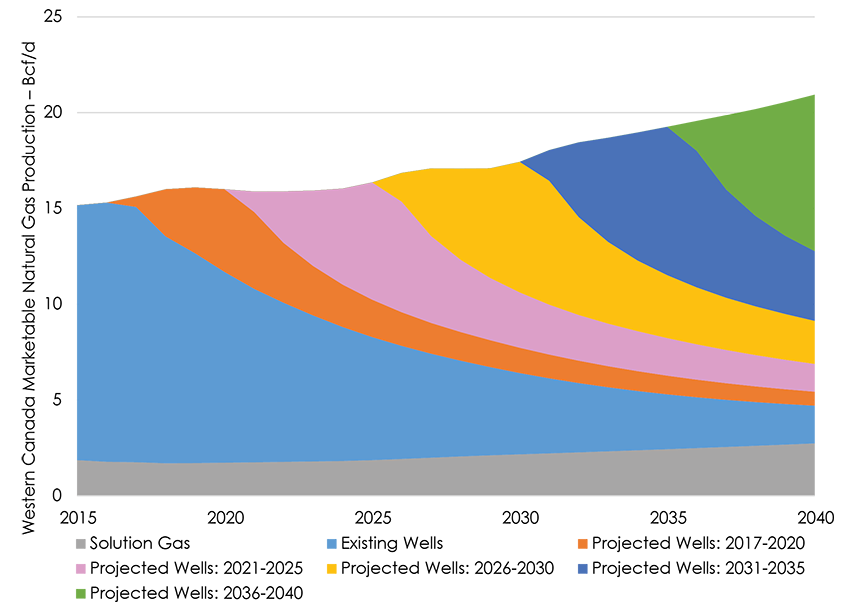

2.3 Production by Well Vintage

- Figure 2.3 shows production by groups of well years. If no new wells were drilled from 2017 onwards, production would drop to 56 10 6m3/d (2.0 Bcf/d) by 2040, not including solution gas.

- Production in each of the five–year increments increases over the projection period as gas prices and capital expenditures increase, increasing drill days and wells drilled (see Appendices B1.1 – B1.4 and Appendices B2.1–B2.4 [EXCEL 6929 KB] for detailed drill days and wells by year for each grouping).

Figure 2.3 Reference Case Production by Well Vintage

Description:

This graph breaks down the Reference Case projection for Canadian marketable natural gas production by gas well vintages, grouped together in about 5 year increments starting in 2017. Solution gas is also included and is projected to increase from 1.86 Bcf/d in 2015 to 2.74 Bcf/d in 2040. Production from all wells drilled before 2017 is projected to decrease from 13.31 Bcf/d in 2015 to 1.97 Bcf/d in 2040. Production from wells drilled from 2017 to 2020 increases from 0.54 Bcf/d in 2017 to 4.32 Bcf/d in 2020, and then decreases to 0.73 Bcf/d in 2040. Production from wells drilled from 2021 to 2025 increases from 1.07 Bcf/d in 2021 to 6.12 Bcf/d in 2025, and then decreases to 1.45 Bcf/d in 2040. Production from wells drilled from 2026 to 2030 increases from 1.50 Bcf/d in 2026 to 6.81 Bcf/d in 2030, and then decreases to 2.25 Bcf/d in 2040. Production from wells drilled from 2031 to 2035 increases from 1.60 Bcf/d in 2031 to 7.74 Bcf/d in 2035, and then decreases to 3.64 Bcf/d in 2040. Production from wells drilled from 2036 to 2040 increases from 1.56 Bcf/d in 2036 to 8.17 Bcf/d in 2040.

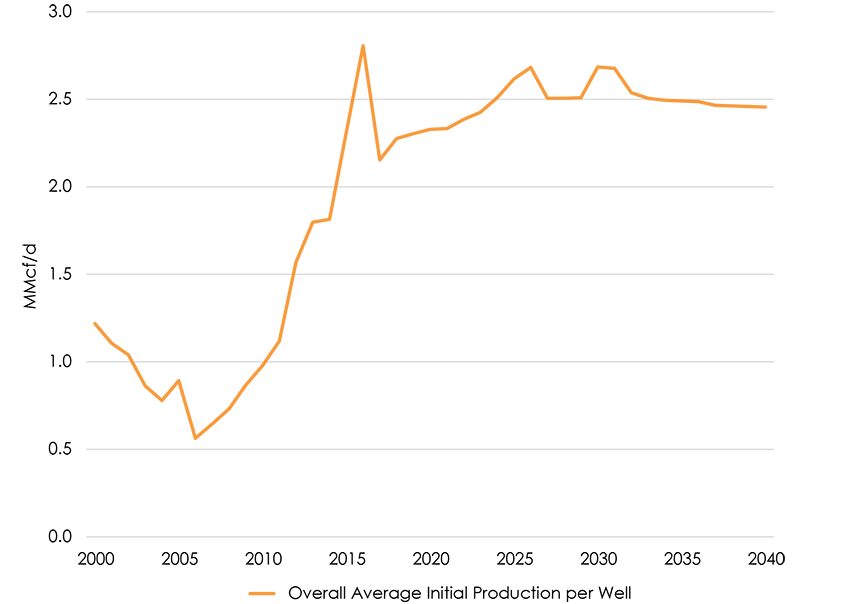

2.4 Well Initial Productivity

- Industry focus on deeper resources has increased the average initial production (IP) rate of western Canadian gas wells. The average IP per well was lowest in 2006 at 0.56 million cubic feet per day (MMcf/d) as many low productivity, shallow wells were being drilled (Figure 2.4). In contrast, the average IP for all wells drilled in western Canada was 2.15 MMcf/d in 2017 – a large jump over the last decade because of increased targeting of deeper resources with horizontal drilling and multi–stage hydraulic fracturing. The average IP over the projection is expected to remain high as operators continue focusing on productive, deeper wells. IPs are also expected to remain steady over the projection: improved drilling and completion technology is expected to offset increased development of non–coreFootnote 5 areas after operators fully develop their core acreage.Footnote 6 The bumps in 2025 and 2030 reflect the additional drilling of the Montney and Horn River plays for LNG export – both of which have high IP rates (see Appendices A3.3, A4.1, and A4.2 [EXCEL 6929 KB] for IP and other decline parameters by year for each grouping).

Figure 2.4 Western Canada Average Well Initial Production by year

Description:

This graph includes the average initial production rate for all gas wells drilled in western Canada, per million cubic feet per day. The average for wells drilled in 2000 was 1.22. In 2017 the average was 2.15 and is projected to be 2.46 in 2040.

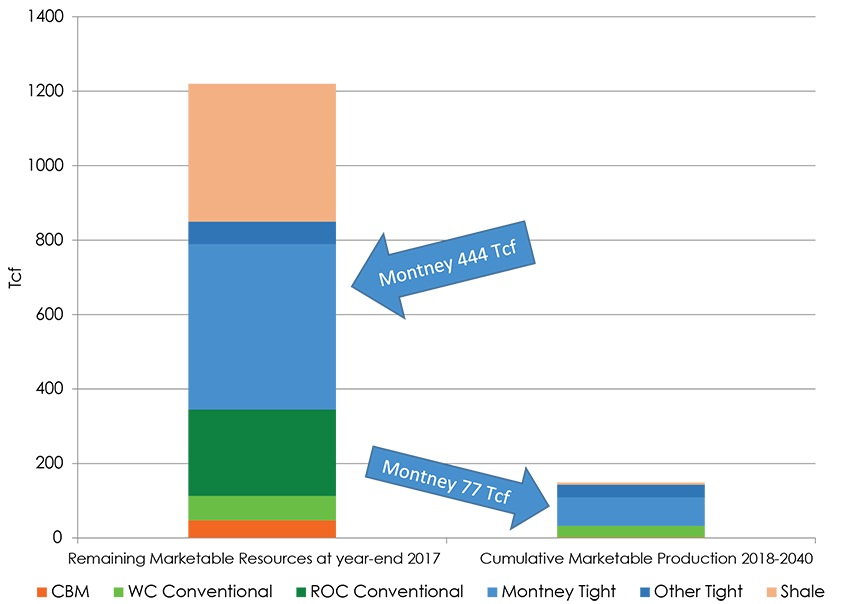

2.5 Marketable Natural Gas Resources

Canada has abundant natural gas resources. With existing technology, the amount of remaining marketable gas available to be developed as of year–end 2017 is estimated at 1 220 trillion cubic feet (Tcf) or over 200 years of supply at current production. Canada currently produces 5.7 Tcf per year. From 2018 to 2040, total production will be 149 Tcf – just 12% of Canada’s 1 220 Tcf potential. For the Reference Case, Canadian resources are still projected to contain 1 071 Tcf at the end of 2040, or 188 years of production at 2017 production. See the EF2018 Appendices for a breakdown of resource by type of gas and area.

Figure 2.5 Gas Resources versus Projected Production

Description:

This chart breaks down the remaining marketable natural gas resources in Canada as of 31 December 2017 and cumulative Canadian marketable natural gas production in the Reference Case by area and type of gas over the projection period from 2018 to 2040. At the end of 2017 there was 47.37 Tcf of remaining marketable CBM resource and 2.02 Tcf are projected to be produced over the projection period. At the end of 2017 there was 65.83 Tcf of remaining marketable conventional gas resource in western Canada and 30.75 Tcf are projected to be produced over the projection period. At the end of 2017 there was 231.60 Tcf of remaining marketable conventional gas resource in the rest of Canada and 0.16 Tcf are projected to be produced over the projection period. At the end of 2017 there was 444.05 Tcf of remaining marketable Montney tight gas and 76.58 Tcf are projected to be produced over the projection period. At the end of 2017 there was 60.80 Tcf of remaining marketable other tight gas in western Canada and 33.91 Tcf are projected to be produced over the projection period. At the end of 2017 there was 370.13 Tcf of remaining marketable shale gas in western Canada and 5.62 Tcf are projected to be produced over the projection period. In all of Canada as of 31 December 2017 there was a total of 1219.79 Tcf remaining marketable natural gas and over the projection period 149.04 Tcf is projected to be produced in the Reference Case.

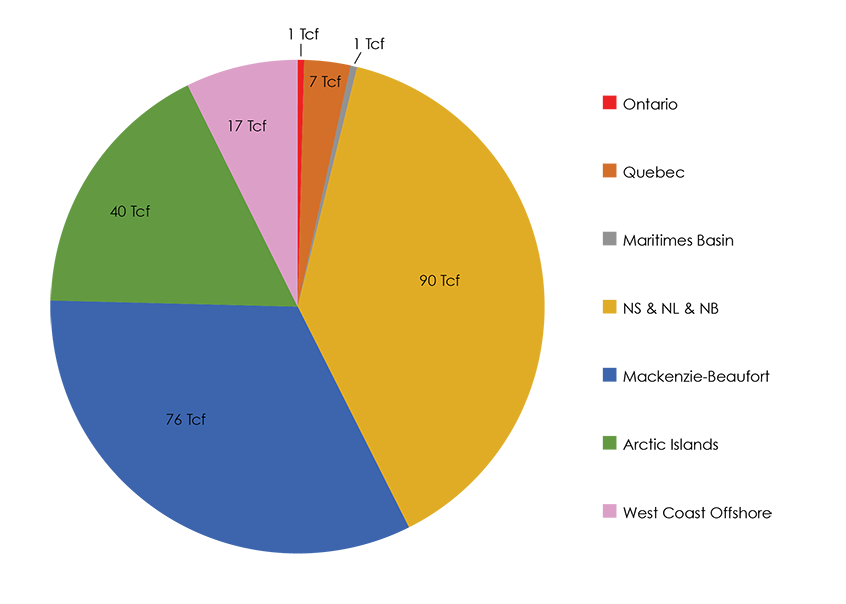

- Western Canada contains a significant amount of Canada’s natural gas resource. The rest of Canada also has significant resources with the majority located in northern Canada (Figure 2.6).

Figure 2.6 Rest of Canada (ROC) Gas Resources

Description:

This chart breaks down the remaining marketable natural gas resources in the rest of Canada by area, as of 31 December 2017. In Ontario there was 0.97 Tcf. In Quebec there was 7.0 Tcf. In the Maritimes Basin there was 1.00 Tcf. In Nova Scotia, Newfoundland and Labrador, and New Brunswick there was 89.63 Tcf. In Mackenzie–Beaufort there was 76.00 Tcf. In the Arctic Islands there was 40.00 Tcf. In West Coast offshore there was 17.00 Tcf.

Chapter 3: All Cases

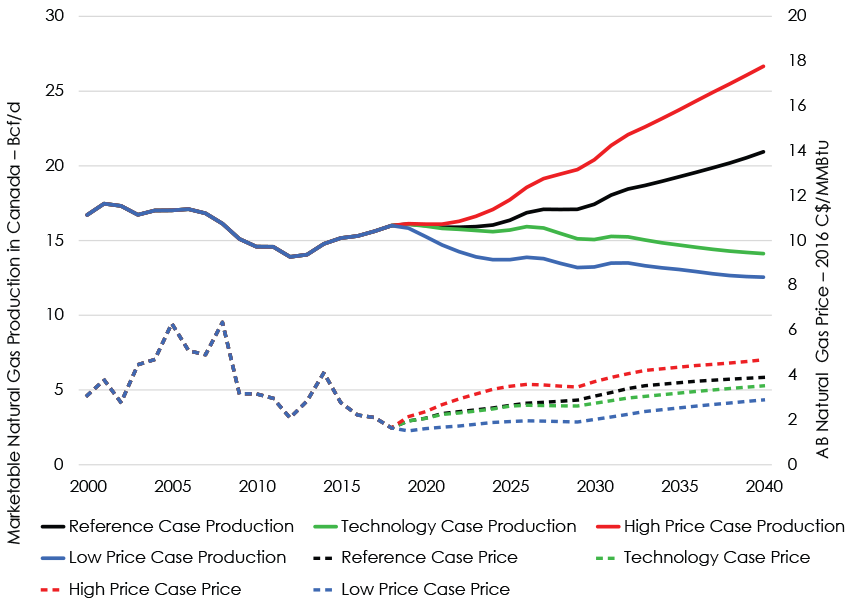

- Natural gas production varies between the cases, especially for the High and Low Price cases (Figure 3.1). All cases show the same focus on more economic deep and tight gas resources. The projections for the rest of Canada, and for LNG exports, are the same in all four cases.

- In all cases except for the Low Price Case, production is expected to decline over the short term before eventually increasing from year to year to the end of the projection period. In the Low Price Case, sub–$4 per million British thermal units gas prices are not high enough to enable sufficient revenues to fund capital expenditures to drill enough new wells for production from new wells to outpace the decline in production from older wells. As a result, total production declines over the entire projection. Production drops to 355 10 6m3/d (12.6 Bcf/d) in 2040, or 40% lower than the Reference Case.

- The High Price Case projection reaches 755 10 6m3/d (26.7 Bcf/d) in 2040, or 27% higher than the Reference Case. This is largely from a compounding effect over the duration of the projection, where higher prices cause more drilling and more production – which in turn leads to more revenue. These higher revenues generate higher capital expenditures and more drilling and production in subsequent years, and so onFootnote 7. However, this analysis makes the assumption that markets will exist and infrastructure will be built as needed and does not address the question of where this production would be consumed.

- The Technology Case has carbon prices rising to $336/tonne in nominal dollars by 2040 – almost seven times as much as the other cases’ carbon price of $50/tonne. Gas prices are also slightly lower that the Reference Case (Figure 3.1). Lower gas prices and higher carbon costs result in less revenue and, therefore, less capital expenditures and less gas drilling, leading to lower gas production. Solution gas is also lower in this case since the projection of conventional oil production in the Technology Case is also lowerFootnote 8. Production drops to 355 10 6m3/d (12.6 Bcf/d) in 2040, or 40% lower than the Reference Case.Footnote 9

Figure 3.1 Gas Price and Production Projections by Case

Description:

This graph shows the projections for Canadian marketable natural gas production and Alberta natural gas price for all four cases. The Alberta natural gas price is in 2016 Canadian dollars per MMBtu. In the Reference Case price is projected to increase from $2.10 in 2017 to $3.89 in 2040, and production is projected in increase from 15.62 Bcf/d in 2017 to 20.94 Bcf/d in 2040. In the Technology Case gas price is projected to increase to $3.52 in 2040, and production is projected to decrease to 14.13 Bcf/d in 2040. In the High Price Case gas price is projected to increase to $4.68 in 2040, and production is projected to increase to 26.67 Bcf/d in 2040. In the Low Price Case gas price is projected to decrease to $2.89 in 2040, and production is projected to decrease to 12.55 Bcf/d in 2040.

Chapter 4: Considerations

- This analysis assumes that over the long term, all energy production will find markets and infrastructure will be built as needed. However, a lack of markets for Canadian natural gas production could reduce the prices Canadian producers receive relative to the Henry Hub price and impact gas production trends.

- These projections describe what is possible today given price, economics, technology, geology, and other assumptions. Actual production could be different given other unforeseen factors like demand, weather, processing plant outages, etc.

- Gas production depends on price, but also on recovery technology, drilling efficiency and costs. Should technology or costs advance differently than assumed, capital expenditures and well production projections would be different than modelled here.

- Canada has abundant natural gas resources.

Appendix

Appendix A

Appendix A1 – METHODS (DETAILED DESCRIPTION)

Canadian natural gas production from 2018 to 2040 will consist of conventional and tight gas production from the WCSB with contributions from Atlantic Canada, Ontario, coalbed methane (CBM) production from Alberta, and shale gas production from Alberta and B.C. Analysis in this report includes trends in well production characteristics and resource development expectations – used to develop parameters that define future natural gas production from the WCSB. Different approaches were used for other regions of Canada where production is sourced from a smaller number of wells.

A1.1 WCSB

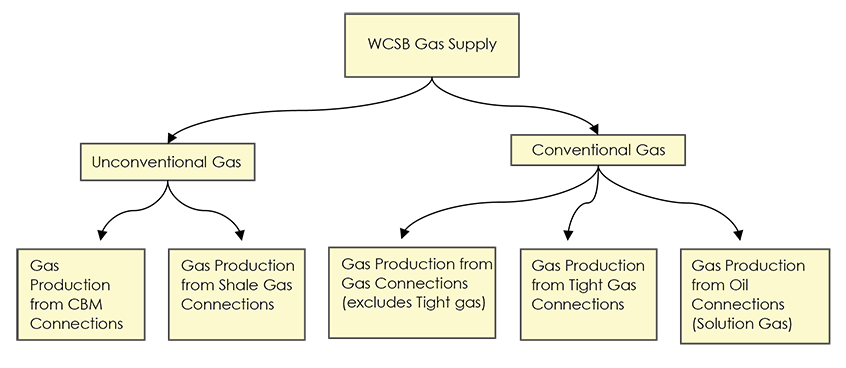

To assess gas production for the WCSB, gas production was split into five type categories as shown in Figure A1.1.

Figure A1.1 - WCSB Major Gas Production Categories

The method to determine gas production associated with conventional gas wells (including tight gas), CBM wells, and shale gas wells is described below. Production decline analysis on historical production data was used to determine parameters that define future performance. The method to determine gas production related to oil wells (solution gas) is described in Section A1.1.2 of this appendix.

A1.1.1 Groupings for Production Decline Analysis

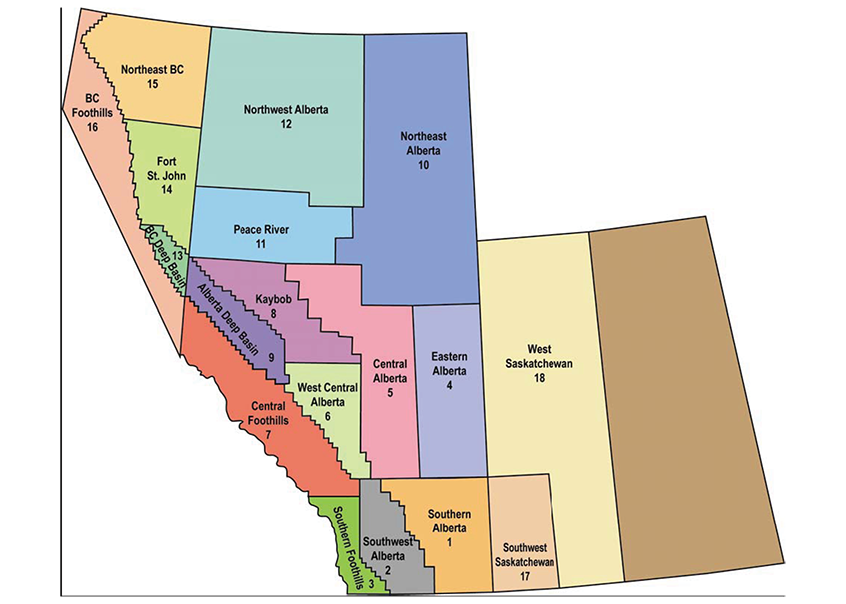

Different groupings by type of gas well were made to assess well performance characteristics. Conventional, tight, and shale gas wells were grouped geographically on the basis of the Petrocube areas in Alberta, B.C., and Saskatchewan, as shown in Figure A1.2. These wells were also grouped by geological zone. In this analysis, gas production from the Montney Formation is separate from the other tight gas sources.

Figure A1.2 - WCSB Area Map

Within each Petrocube area and zone, gas wells were grouped by year, with all wells existing prior to 1999 forming a single group, and separate groups for each year from 1999 through 2040.

CBM wells in Alberta were also grouped primarily by zone into three categories:

- Horseshoe Canyon Main Play

- Mannville CBM, and

- Other CBM

Within each of the three categories of CBM resources, wells were also grouped by well year. For the Horseshoe Canyon Main Play and Other CBM categories, there is a single grouping for all wells existing prior to 2004, and separate groupings for each year thereafter. For Mannville CBM, a single grouping was made for all wells existing prior to 2006, and separate groupings for each following year.

In total there are about 150 gas resource groupings representing western Canada, each with its own set of decline parameters for each year.

A1.1.2 Method for Existing Wells

The method applied to make the gas production projections for existing wells differs from what is done to project production for future wells. For existing wells, production decline analysis on historical production data is done on each grouping (gas type/Petrocube area/geological zone and by well year) to develop two sets of parameters.

- Group production parameters - describing production expectations for the entire gas resource grouping.

- Average well production parameters - describing production expectations for the average gas well in the grouping.

The method for the production decline analysis on existing wells is described below. The group production parameters and average well production parameters resulting from this analysis are contained in Appendices A.3 and A.4, respectively.

In the model, the group production parameters are used to make the production projection for existing wells. For each of these groupings, a data set of group marketable production history is created. The data sets for group marketable production are generated as follows:

- Raw well production for gas connections in each grouping is summed by calendar month getting total group raw production by calendar month.

- The total group raw production by calendar month is multiplied by an average shrinkage factor that applies to the grouping and divided by the number of days in each month to get total monthly marketable gas production and marketable gas production rate (MMcf/d) for each calendar month.

- Using this data set, plots of total daily marketable production rate versus total cumulative marketable production are generated for each grouping.

The data sets for average well production history are created as follows.

- The raw well production by month for each connection in the grouping is put in a data base.

- For each entry of production month for each well, a value of normalized production month is calculated as the number of months between the month the connection began producing and the actual production month (this is the normalized production month).

- The raw production for wells in the grouping is summed by normalized production month and then multiplied by the average shrinkage factor that applies to the grouping, providing total marketable production by normalized production month.

- The marketable production for normalized production month is then divided by the average number of days in a month, or 30.4375, giving the production rate for the average well in the grouping by normalized production month.

- Using this data set, daily marketable production rate versus cumulative marketable production for the average well were generated for each grouping.

For conventional gas wells, the following procedures are applied in performing production decline analysis using the group and average well historical production data sets:

- Production Decline Analysis for the Pre – 1999 Wells

In each grouping, the group rate versus cumulative production plot for the grouping of gas wells on production prior to 1999 is the first to be evaluated. In all groupings a stable exponential decline for the past several years was exhibited. The group plot for all the wells prior to 1998 yields a current marketable production rate, a stable decline rate applicable to future production, and a terminal decline if seen fit. - Production Decline Analysis for 1999 – 2017 Wells

After the initial aggregate well year is evaluated for a grouping, each year is evaluated in sequence, from 1999 through 2017.

- Production Decline Analysis for the Average Well:

For each well year, the rate versus cumulative production plot for the average well is evaluated first to establish the following parameters that describe the production profile of the average well over the entire productive life: -

- Initial Production Rate

- First Decline Rate

- Second Decline Rate

- Months to Second Decline Rate- usually around 18 months

- Third Decline Rate

- Months to Third Decline Rate- usually around 45 months

- Fourth Decline Rate

- Months to Fourth Decline Rate- usually around 100 months.

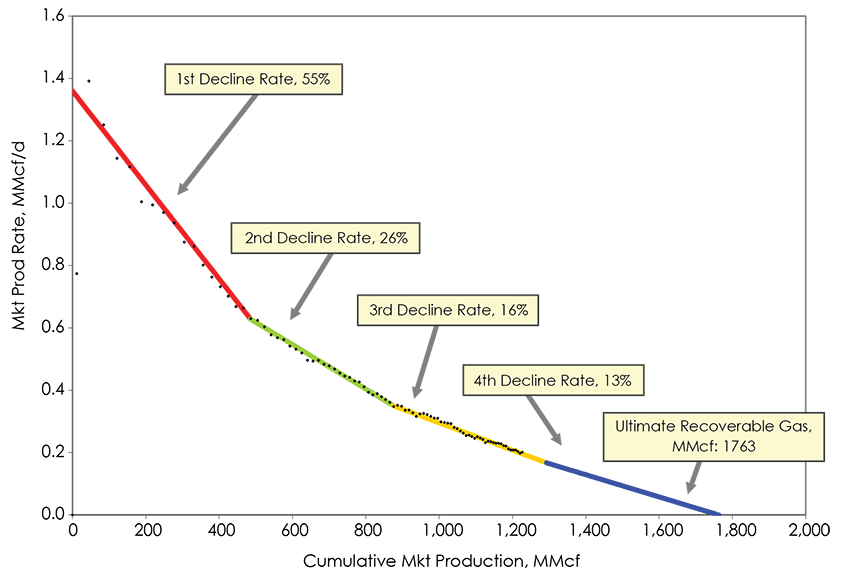

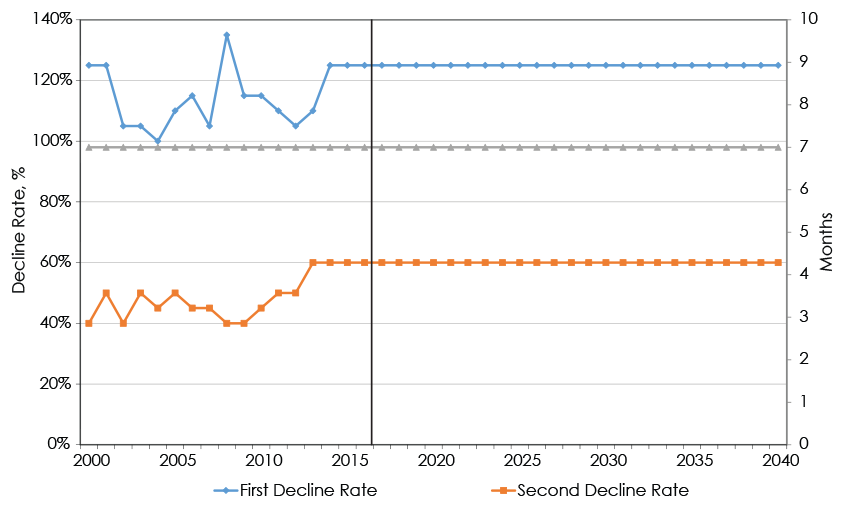

Figure A1.3 shows an example of the plots used in evaluation of average well performance, and the different decline rates that are applied to describe the production.

Figure A1.3 – Example of Average Well Production Decline Analysis Plot

Source: NEB analysis of Divestco Geovista well production data

For the earlier well years, the available data is usually sufficient to establish all of the above parameters. For more recent well years, the duration of historical production data becomes shorter and the parameters describing the later life decline performance must be taken from that determined for earlier well years. In the example shown in Figure A1.3, the available data is sufficient to determine parameters defining the first, second, and third decline periods for the well, but the parameters defining the fourth decline period must be assumed based on the analysis of earlier well years.

It is assumed that, unless the historical data for the well year indicates otherwise, the fourth decline rate will equal the terminal decline rate for the grouping established through evaluation of all pre – 1999 wells, and that period of the terminal decline rate will commence after 120 months of production.

The decline parameters determined in this manner for average wells are available in Appendix A4.

- Production Decline Analysis for the Group Data:

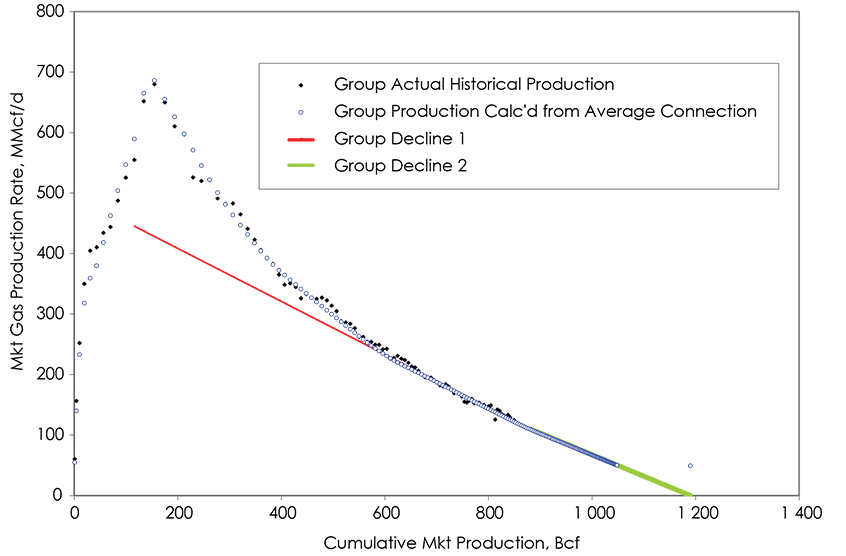

Once the performance parameters for the average well are established, the procedure focuses on evaluation of group performance parameters.

As a first step, the average well performance parameters are combined with the known 12–month well schedule to calculate the expected group performance. This is plotted with the actual group performance data. If the data calculated from average well performance data does not provide a good match with the actual historical production data for the group, then the average well parameters may be revised until a good match is obtained between calculated group production data (from average well data) and actual group production data. An example of the group plots described here is shown in Figure A1.4.

Figure A1.4 – Example of Group Production Decline Analysis Plot

Source: NEB analysis of Divestco Geovista well production data

The following group performance parameters are determined from the group plot:

- Production Rate as of month one

- First Decline Rate

- Second Decline Rate (if applicable)

- Months to Second Decline Rate (if applicable)

- Third Decline Rate (if applicable)

- Months to Third Decline Rate (if applicable)

- Fourth Decline Rate (if applicable)

- Months to Fourth Decline Rate (if applicable)

In the earlier well year groupings (2001, 2002, etc.), the actual group data is usually stabilized by the current date at or near the terminal decline rate established via the pre–1999 aggregate grouping. In these cases a single decline rate sufficiently describes the entire remaining productive life of the grouping. In these cases the expected performance calculated from average well data has little influence over determination of the group parameters.

In later well years (2015, 2016, etc.) actual group production history data cannot provide a good basis upon which to project future production. In these cases the expected performance calculated from average well data is vital to establishing the current and future decline rates.

Group performance parameters determined in this manner are available in Appendix A3.

The production decline analysis procedure described above is also applied to the CBM groupings and shale gas. Mannville CBM connections have a different performance profile than the other gas resources in the WCSB. While gas wells for all other groupings can be described by an initial production rate that declines in a relatively predictable manner, Mannville CBM connections go through a dewatering phase with gas production increasing over a period of months to a peak rate. After the peak rate is reached decline will occur. Thus a slightly different set of parameters is used to describe performance of the average well for Mannville CBM, with initial production rate being replaced by “Months to Peak Production” and “Peak Production Rate”.

The shorter production history of shale gas makes it more difficult to establish long-term decline rates based on historical data. Nevertheless, decline rates that describe the full productive life of shale gas wells are still estimated based on the NEB’s view of ultimate gas recovery for the average well.

A1.1.3 Method for Future Wells

For future wells, production is estimated based on the number of projected wells and the expected average performance characteristics of those wells. The drilling projection is used to estimate the number of future gas wells. Historical trends in average well performance parameters, obtained from production decline analysis of existing gas wells, are used to estimate average well performance parameters for future well years.

A1.1.3.1 Performance of Future Wells

The performance of future wells is obtained in each grouping by extrapolating the production performance trends for average wells in past years. The performance parameters estimated are initial productivity of the average well and the associated decline rates.

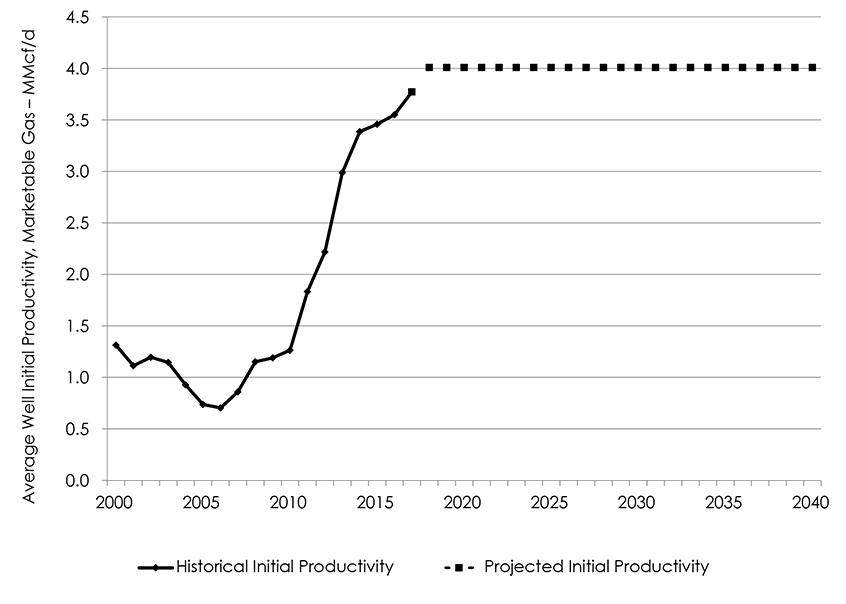

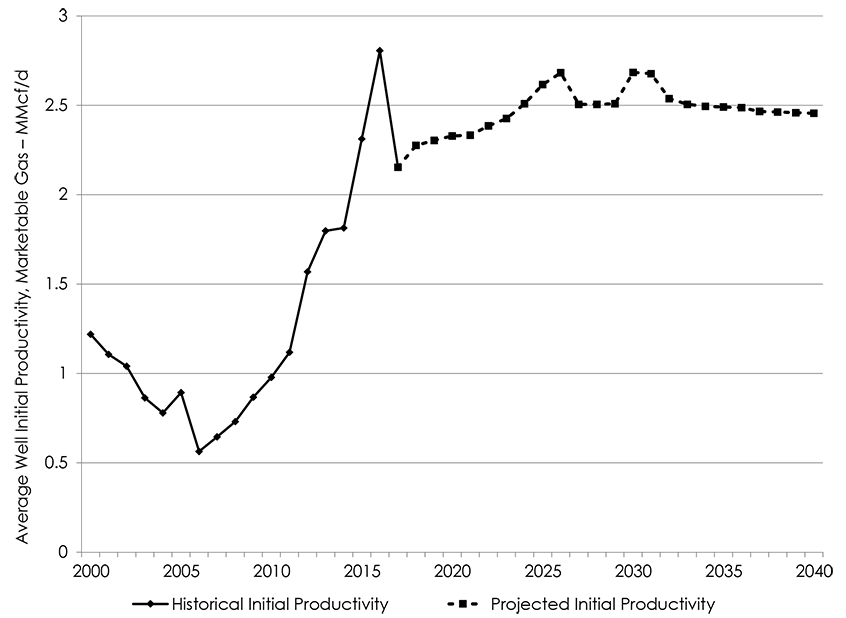

In many groupings there are trends of decreasing or increasing initial productivity for the average gas well. Figure A1.5, which shows the initial production rate over time for tight gas wells in the Alberta Deep Basin Upper Colorado grouping. The IP was trending down until about 2006 when horizontal drilling and multi–stage hydraulic fracturing technologies started taking off, which increased the IP over the last decade in this grouping. The initial production rate for future gas wells is estimated by extrapolating the trend in each grouping, and are adjusted if there are any other assumptions such as technological or resource changes. Historical and projected initial productivity values for the average well for all groupings are contained in Appendices A3 and A4.

Figure A1.5 – Example of Average IP by Year – Alberta Deep Basin Mannville Tight Grouping

Source: NEB analysis of Divestco well production data

The key decline parameters impacting the near term are the first decline rate, second decline rate, and months to second decline rate. Figure A1.6 shows the historical and projected values of these key decline parameters for the average well in the Alberta Deep Basin Mannville Tight grouping. As shown in Figure A1.6, trends seen in the decline parameters in past years are used to establish these key parameters for future years.

Figure A1.6 – Example of Key Decline Parameters Over Time – Alberta Deep Basin Mannville Tight Grouping

A1.1.3.2 Number of Future Wells

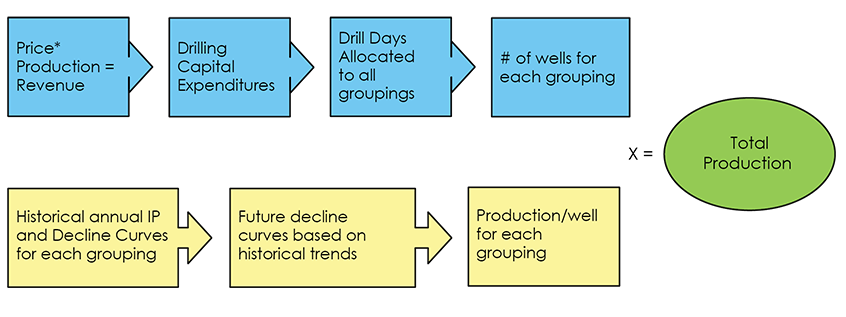

Figure A1.7 shows the method for projecting the number of gas wells for each year over the projection period. The key inputs are amount of re-investment of revenue and the drill day cost. Adjustments to these two key inputs can significantly change the drilling projections. The values projected for the other inputs are estimated from an analysis of historical data.

The Board projects an allocation of gas drill days for each of the groupings. The allocation fractions are determined from historical trends, recent estimates of supply costs, and the Board’s view of development potential for the groupings. The allocation fractions reflect the historical trends of an increasing focus on the deeper formations located in the western side of the basin, increasing interest in tight gas and gas shales in B.C. and Alberta, and further development of liquids rich/wet natural gas. Tables of drill days by year by grouping for each case are in Appendices B1.1 to B1.4.

The number of gas wells drilled in each year is calculated by dividing the drill days targeting each resource grouping by the average number of days it takes to drill a well. Future drill days per well for each grouping are based on historical data, and any assumptions on drilling efficiency or resource changes. Tables of wells by year by grouping for each case are in Appendices B2.1 to B2.4.

Figure A1.7 – Flowchart of Drilling Projection Method

A1.1.4 Solution Gas

Solution gas is gas produced from oil wells in conjunction with the crude oil and currently accounts for over 10% of total marketable gas production in the WCSB. Solution gas analysis is by Petrocube area and is projected by using historical trends and projected conventional, tight, and shale oil production by province (Canada’s Energy Future 2018 Supplement: Conventional, Tight, and Shale Oil Production). The projected solution gas production is deemed to represent all solution gas production (i.e. production from both existing and future oil wells).

A1.1.5 Yukon and Northwest Territories

No production from the Mackenzie Delta and elsewhere along the Mackenzie Corridor is included over the projection, as lower prices have rendered production uneconomic. The Norman Wells field produces small amounts of gas that serve local purposes and is not tied into the North American pipeline grid. Natural gas production at Norman WellsFootnote 10 has been halted since February 2017 after the line that carries the gas south, Line 21, had been shut down after a riverbank beneath a portion of the line near Fort Simpson had become unstable. The line has been approved to re–open, and production is expected to re–start with an estimated time of January 2019. Gas production out of Norman Wells is estimated to be at the level it recently was before the shutdown, and then declining over the projection. Cameron Hills production ceased in February 2015.

A1.2 Atlantic Canada

Natural gas production in Atlantic Canada continues to decline over the projection period. Onshore natural gas production in New Brunswick falls to near zero by 2040. Offshore natural gas production in Nova Scotia is assumed to decline steadily and ceases by 2021 for both the Deep Panuke and Sable projects. Given relatively high costs for offshore exploration and current provincial policies for onshore gas exploration, no new Atlantic Canada gas fields are projected to come online.Footnote 11

Onshore production from the McCully Field in New Brunswick was connected into the regional pipeline system at the end of June 2007 and now operates on a seasonal basis.

Shale gas potential exists in New Brunswick and Nova Scotia, however, provincial policies currently prohibit hydraulic fracturing which is required for shale gas development. It is assumed these policies do not change over the projection period.

A1.3 Other Canadian Production

A minor remaining amount of Canadian production is from Ontario. Production from Ontario is projected by extrapolation of historical production volumes. Shale gas potential exists in Quebec, however, provincial policies currently prohibit hydraulic fracturing which is required for shale gas development. It is assumed these policies do not change over the projection period.

Appendix A2 – Production Parameters – Results

A2.1 WCSB

A2.1.1 Production from Existing Gas Wells

The future production of existing wells of the resource groupings comprising conventional (including tight gas), and unconventional (including shale gas and CBM), and all solution gas was determined via the production analysis procedures described in Appendix A1. The decline parameters for these groupings are the same for all cases.

The parameters describing future production for all of these groupings are the production rate as of December 2017 and as many as four future decline rates that apply to specified time periods in the future. For the older wells where production appears to have stabilized at a final decline rate, only one future decline rate is needed to describe future group deliverability. For newer wells, the decline rate that applies over future months changes as the group performance progresses towards the final stable decline period. For these newer wells, three or possibly four different decline rates have been determined to describe future performance.

The projected production from existing wells represents the production that would occur from the WCSB if no further gas wells started producing after December 2016. Production from future gas wells supplements the declining production from existing wells.

A2.1.2 Production from Future Gas Wells

Production associated with future gas wells is calculated for each resource grouping using estimates for production performance of the average well and the number of wells in future years. The parameters associated with both of these inputs are discussed in the sections below.

While past projections for existing gas wells have enjoyed a high degree of accuracy, the certainty associated with the projections for future gas wells is less. The key uncertainties are the level of gas drilling that will occur and the production levels of wells. The high and low price cases aim to address the uncertainty inherent in the gas drilling projections.

A2.1.2.1 Performance Parameters for Future Average Gas Wells

The production decline analysis procedures described in Appendix A.1 provide the basis for establishing performance parameters for future gas wells. The trends seen in average well performance for the various groupings of existing wells are used to make an estimate of performance parameters for future gas wells

With respect to initial productivity of the average gas well, the overall trend for the WCSB is shown in Figure A2.1. After decreases in initial productivity over 2001 to 2006, the trend reversed upward for 2007, remained fairly stable through 2009, and continued upward through to 2015 as higher initial productivity rates from tight gas and shale gas wells began to represent a growing share of the wells drilled in a year. Initial productivity over the projection is almost flat primarily due to holding the rates constant for most gas wells.

Figure A2.1 – WCSB Production–Weighted Average IP by Year, Reference Case

Source: NEB Analysis of Divestco Well Production Data

Table A2.1 shows the historical production-weighted average IP for wells by area by year. Appendices A3 and A4 provide historical and projected performance parameters for all groupings.

Table A2.1 – Production–Weighted Average IP by Year by Area, Reference Case (MMcf/d)

Source: NEB Analysis of Divestco Well Production Data

The performance parameters projected are the same in all cases assessed in this report. Variance between the cases is affected by applying different levels of gas drilling activity as discussed further in Section A2.1.2.2 of this appendix.

A2.1.2.2 Number of Future Gas Wells

The projected number of wells by year and the projected production performance of the average wells in those years determine projected production of future gas wells. To determine the number of future gas wells, projections of gas drilling activity by grouping are made.

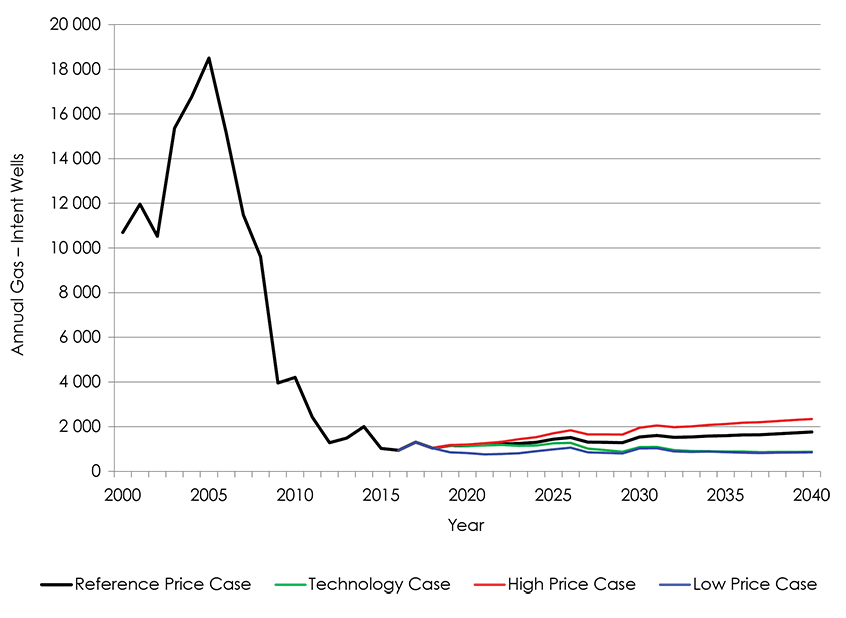

Volatile and unpredictable market conditions are expected to be the primary influences on gas drilling activity. As a result, there is a high degree of uncertainty in the gas drilling activity that could occur over the projection period. The High Price Case and Low Price Case reflect a range of market conditions that may occur over the projection period. Figure A2.2 shows the total projected number of gas wells by year by case.

Projected annual gas wells and drilling days for each grouping are provided in Appendices B1.1 to B1.4 and B2.1 to B2.4.

Figure A2.2 – WCSB Gas Wells by Case

A2.2 Atlantic Canada, Ontario, and Quebec

As indicated in Appendix A1, production from Atlantic Canada and Ontario is based on extrapolation of prior trends. No additional wells over the projection period are assumed to be drilled that would contribute to production at this time.

Marketable production from the Deep Panuke development started in fall 2013. Deep Panuke has begun producing seasonally in the winters, however incursion of water into the reservoir could adversely impact the amount of natural gas recoverable over the lifetime of the project. In this report offshore natural gas production in Nova Scotia declines steadily over the projection period and production ceases by 2021 for both the Deep Panuke and Sable projects.

Provincial policy in New Brunswick and Nova Scotia currently prohibits hydraulic fracturing which is required for shale gas development. It is assumed that these policies do not change and no additional onshore gas wells are drilled over the projection period. Ontario production continues to decline with no additional drilling expected over the projection period.

Provincial policy in Quebec currently prohibits hydraulic fracturing which is required for shale gas development. It is assumed that these policies do not change and no additional gas wells are drilled over the projection period.

Appendix A3 – Groupings and Decline Parameters for Existing Wells

Table A3.1 – Formation Index

| Formation | Abbreviation | Group Number |

|---|---|---|

| Tertiary | Tert | 02 |

| Upper Cretaceous | UprCret | 03 |

| Upper Colorado | UprCol | 04 |

| Colorado | Colr | 05 |

| Upper Mannville | UprMnvl | 06 |

| Middle Mannville | MdlMnvl | 07 |

| Lower Mannville | LwrMnvl | 08 |

| Mannville | Mnvl | 06;07;08 |

| Jurassic | Jur | 09 |

| Upper Triassic | UprTri | 10 |

| Lower Triassic | LwrTri | 11 |

| Triassic | Tri | 10;11 |

| Permian | Perm | 12 |

| Mississippian | Miss | 13 |

| Upper Devonian | UprDvn | 14 |

| Middle Devonian | MdlDvn | 15 |

| Lower Devonian | LwrDvn | 16 |

| Horseshoe Canyon | HSC | - |

| Mannville CBM | Mannville | - |

Table A3.2 – Grouping Index

| Area Name | Area Number | Resource Type | Resource Group |

|---|---|---|---|

| CBM Area | 00 | CBM | Main HSC |

| CBM Area | 00 | CBM | Mannville |

| Southern Alberta | 01 | Conventional | Tert;UprCret;UprColr |

| Southern Alberta | 01 | Conventional | Colr |

| Southern Alberta | 01 | Conventional | Mnvl |

| Southern Alberta | 01 | Tight | UprColr |

| Southwest Alberta | 02 | Conventional | Tert;UprCret;UprColr |

| Southwest Alberta | 02 | Conventional | Colr |

| Southwest Alberta | 02 | Conventional | MdlMnvl;LwrMnvl |

| Southwest Alberta | 02 | Conventional | Jur;Miss |

| Southwest Alberta | 02 | Conventional | UprDvn |

| Southwest Alberta | 02 | Tight | UprColr |

| Southwest Alberta | 02 | Tight | Colr |

| Southwest Alberta | 02 | Tight | LwrMnvl |

| Southern Foothills | 03 | Conventional | Miss;UprDvn |

| Eastern Alberta | 04 | Conventional | UprCret;UprColr |

| Eastern Alberta | 04 | Conventional | Colr;Mnvl |

| Eastern Alberta | 04 | Tight | UprColr |

| Eastern Alberta | 04 | Shale | Duvernay |

| Central Alberta | 05 | Conventional | Tert;UprCret |

| Central Alberta | 05 | Conventional | Colr |

| Central Alberta | 05 | Conventional | Mnvl |

| Central Alberta | 05 | Conventional | Miss;UprDvn |

| Central Alberta | 05 | Tight | Colr |

| Central Alberta | 05 | Tight | Mvl |

| Central Alberta | 05 | Tight | Montney |

| Central Alberta | 05 | Shale | Duvernay |

| West Central Alberta | 06 | Conventional | Tert |

| West Central Alberta | 06 | Conventional | UprCret;UprColr |

| West Central Alberta | 06 | Conventional | Mnvl |

| West Central Alberta | 06 | Conventional | LwrMnvl; Jur |

| West Central Alberta | 06 | Conventional | Miss |

| West Central Alberta | 06 | Conventional | UprDvn |

| West Central Alberta | 06 | Tight | Colr |

| West Central Alberta | 06 | Tight | Mnvl |

| West Central Alberta | 06 | Tight | Montney |

| West Central Alberta | 06 | Shale | Duvernay |

| Central Foothills | 07 | Conventional | UprColr |

| Central Foothills | 07 | Conventional | Colr;Mnvl |

| Central Foothills | 07 | Conventional | Jur;Tri;Perm |

| Central Foothills | 07 | Conventional | Miss |

| Central Foothills | 07 | Conventional | UprDvn;MdlDvn |

| Central Foothills | 07 | Tight | UprColr;Colr |

| Central Foothills | 07 | Tight | Mnvl |

| Central Foothills | 07 | Tight | Jur |

| Central Foothills | 07 | Tight | Montney |

| Central Foothills | 07 | Shale | Duvernay |

| Kaybob | 08 | Conventional | UprColr;Colr |

| Kaybob | 08 | Conventional | Mnvl;Jur |

| Kaybob | 08 | Conventional | Tri |

| Kaybob | 08 | Conventional | UprDvn |

| Kaybob | 08 | Tight | Colr;Mnvl |

| Kaybob | 08 | Tight | Tri |

| Kaybob | 08 | Tight | Montney |

| Kaybob | 08 | Shale | Duvernay |

| Alberta Deep Basin | 09 | Conventional | UprCret |

| Alberta Deep Basin | 09 | Conventional | UprColr |

| Alberta Deep Basin | 09 | Conventional | Mnvl;Jur |

| Alberta Deep Basin | 09 | Conventional | Tri |

| Alberta Deep Basin | 09 | Conventional | UprDvn |

| Alberta Deep Basin | 09 | Tight | UprColr |

| Alberta Deep Basin | 09 | Tight | Colr |

| Alberta Deep Basin | 09 | Tight | Mnvl;Jur |

| Alberta Deep Basin | 09 | Tight | Tri |

| Alberta Deep Basin | 09 | Tight | Montney |

| Alberta Deep Basin | 09 | Shale | Duvernay |

| Northeast Alberta | 10 | Conventional | Mnvl;UprDvn |

| Peace River | 11 | Conventional | UprColr |

| Peace River | 11 | Conventional | Colr;UprMnvl |

| Peace River | 11 | Conventional | MdlMnvl;LwrMnvl |

| Peace River | 11 | Conventional | UprTri |

| Peace River | 11 | Conventional | LwrTri |

| Peace River | 11 | Conventional | Miss |

| Peace River | 11 | Conventional | UprDvn;MdlDvn |

| Peace River | 11 | Tight | UprColr |

| Peace River | 11 | Tight | MdlMnvl;LwrMnvl |

| Peace River | 11 | Tight | UprTri |

| Peace River | 11 | Tight | LwrTri |

| Peace River | 11 | Tight | Tri |

| Peace River | 11 | Tight | Miss |

| Peace River | 11 | Tight | Montney |

| Peace River | 11 | Shale | Duvernay |

| Northwest Alberta | 12 | Conventional | Mnvl |

| Northwest Alberta | 12 | Conventional | Miss |

| Northwest Alberta | 12 | Conventional | UprDvn |

| Northwest Alberta | 12 | Conventional | MdlDvn |

| Northwest Alberta | 12 | Shale | Duvernay |

| BC Deep Basin | 13 | Conventional | Colr |

| BC Deep Basin | 13 | Conventional | LwrTri |

| BC Deep Basin | 13 | Tight | Colr |

| BC Deep Basin | 13 | Tight | Mnvl |

| BC Deep Basin | 13 | Tight | LwrTri |

| BC Deep Basin | 13 | Tight | Montney |

| Fort St. John | 14 | Conventional | Mnvl |

| Fort St. John | 14 | Conventional | Tri |

| Fort St. John | 14 | Conventional | Perm;Miss |

| Fort St. John | 14 | Conventional | UprDvn;MdlDvn |

| Fort St. John | 14 | Tight | Mnvl |

| Fort St. John | 14 | Tight | Tri |

| Fort St. John | 14 | Tight | Perm;Miss |

| Fort St. John | 14 | Tight | Dvn |

| Fort St. John | 14 | Tight | Montney |

| Northeast BC | 15 | Conventional | LwrMnvl |

| Northeast BC | 15 | Conventional | Perm;Miss |

| Northeast BC | 15 | Conventional | UprDvn;MdlDvn |

| Northeast BC | 15 | Tight | UprDvn |

| Northeast BC | 15 | Shale | Cordova |

| Northeast BC | 15 | Shale | Horn River |

| Northeast BC | 15 | Shale | Liard |

| BC Foothills | 16 | Conventional | Colr;Mnvl |

| BC Foothills | 16 | Conventional | Tri;Perm;Miss |

| BC Foothills | 16 | Tight | LwrTri |

| BC Foothills | 16 | Tight | Tri |

| BC Foothills | 16 | Tight | Montney |

| Southwest Saskatchewan | 17 | Tight | UprColr |

| West Saskatchewan | 18 | Conventional | Colr |

| West Saskatchewan | 18 | Conventional | MdlMnvl;LwrMnvl;Miss |

| East Saskatchewan | 19 | Conventional | Solution Gas |

See the Excel Appendix file [EXCEL 6929 KB] for all charts and tables in this Appendix, and for Appendices A, B, and C.

- Date modified: