ARCHIVED – Chapter 2. Recent Context and Key Assumptions

This page has been archived on the Web

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please contact us to request a format other than those available.

The Canadian energy system is constantly evolving. Factors such as economics, infrastructure, and societal preferences influence the production, transportation, and consumption of energy in Canada. Technology, and climate policies and programs increasingly impact energy markets. This chapter provides an overview of recent energy market developments and climate policies. It also describes the key assumptions and recent developments underpinning the analysis in the report.

Crude Oil Markets

Current Context

Crude oil prices are a key driver of the Canadian energy system and are determined by global supply and demand. Canada is a major crude oil producer and prices are an important driver of future production growth. Increased Canadian oil production is largely due to technological improvements over the past decade. The prices of refined petroleum products (RPPs), such as gasoline and diesel, are related to crude oil prices and can influence energy demand.

From 2011 to mid-2014, global crude oil prices typically ranged between US$100 and US$120 per barrel (bbl). From June 2014, prices dropped steadily, with the Brent crude oil price falling to less than US$30/bbl in January 2016. In Canada, the price of Western Canadian Select (WCS) dropped to US$17/bbl. Global prices began to rebound in 2016, and by 2017, Brent prices reached US$65/bbl. The price rise and subsequent drop are evidence of an unbalanced global oil market. Years of rising demand and higher prices resulted in a global supply surplus, and record crude inventory builds.

Recent developments suggest a rebalancing of global oil markets. Sustained production cuts by the Organization of the Petroleum Exporting Countries (OPEC) and Russia, combined with unexpected supply outages, particularly in Venezuela, have reduced global oil supply. Global oil demand outpaced supply in 2017 and is expected to do the same in 2018Footnote 2. Both United States (U.S.) and Organization for Economic Co-operation and Development (OECD) crude and product inventory stocks have been reduced and are currently near their five-year averagesFootnote 3. Also, spot prices have been higher than the futures prices for crude oil, a symptom that emerges when oil traders generally view a market as being undersupplied. Prices have increased over 2017 levels and hovered in a tight range around their 20-year average.Footnote 4

Although global prices have risen, production in North America has outpaced incremental infrastructure, leading to discounted prices. U.S. production growth, particularly from the Permian Basin, has put pressure on pipeline capacity to remove oil from the region. This resulted in West Texas Intermediate (WTI) price discounts to Brent at Cushing, OK climbing to nearly US$10 in mid-2018.

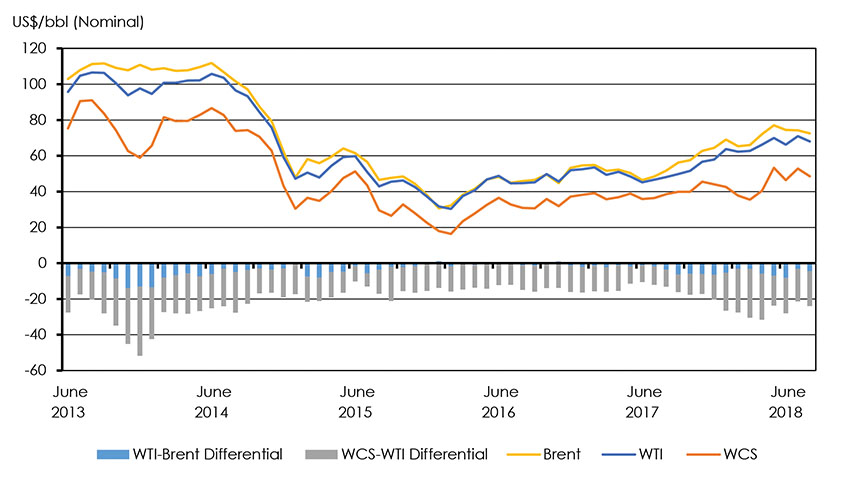

In western Canada, production increased steadily while export capacity remained at 2016 levels or belowFootnote 5 leading to large price discounts for Canadian crude benchmarks. From January to July 2018, WCS has averaged US$21.86 lower than WTI, an increase in the differential of 71% over the same period in 2017. While some discount should be expected based on quality and transportation costs to American refineries compared to other light crude streams, this normally ranges between US$10 and US$15. Western Canadian heavy oil production increased by 9.8% in 2017, and in the first half of 2018 was 8% higher year-over-year. Without incremental pipeline capacity available, some production has shifted to rail, which is more expensive. The WCS-WTI discount has settled over US$30 on some days. Figure 2.1 illustrates Brent, WTI, and WCS prices and differentials over the past five years. Western Canadian light oil benchmarks are also affected, with the Canadian Light Sweet (CLS) differential to WTI averaging US$7.62 per barrel in the first half of 2018, more than double the 2017 US$2.90 differential.

Figure 2.1: Brent, WTI, and WCS Prices and Discounts, 2013-2018

Description

This chart shows the Brent, WTI, and WCS prices and discounts, in nominal USD per barrel, from 2013 to 2018. Brent has declined from $102.9/bbl in June 2013 to $72.5/bbl in June 2018. WTI has declined from $95.8/bbl in June 2013 to $68.1/bbl in June 2018. WCS has declined from $75.4/bbl in June 2013 to $48.6/bbl in June 2018. The WTI-Brent differential has declined from $7.15/bbl in June 2013 to $4.5/bbl by June 2018. The WCS-WTI differential has declined from $20.4/bbl in June 2013 to $19.5/bbl by June 2018.

Expected WCS-WTI Differential Impacts

Most of the Canadian production growth over the next several years comes from large-scale oil sands projects that were commissioned well in advance of the fall in oil prices. It is expected that western Canadian oil exports will surpass pipeline export capacity, in which case the WCS-WTI differential could average anywhere between US$18 and about US$30.

Factors Currently Affecting Crude Oil Markets:

- Global crude oil supply and demand.

- Incremental pipeline and rail capacity.

- Projects in progress (oil sands).

- IMO’s 0.5% sulphur content regulation.

Canadian oil priced off WCS faces further downward pricing pressure from the International Maritime Organization (IMO) sulphur content regulations. The IMO’s global limit of 0.5% sulphur content in fuel used by ships comes into force on 1 January 2020Footnote 6. Canadian heavy crude will have increased competition for coker refinery capacity in the U.S. Gulf Coast resulting in lower WCS prices as Canadian heavy crude competes to maintain access to the fixed available refining capacity. While the degree and duration of the IMO impact on global refining and crude markets is uncertain, it will likely exert downward pressure on WCS prices for the duration of its influence.

International Maritime Organization Sulphur Regulations

The IMO is an agency belonging to the United Nations, whose mission is to regulate, among other things, emissions from the shipping industry. There are currently 174 countries who are members of the IMO.

The IMO’s global limit of 0.5% sulphur content in fuel used by ships comes into force on 1 January 2020Note a. Compliance with the regulation is expected to be high, in the range of more than 70%Note b. The majority of compliance is expected to be through the use of fuel substitution, particularly toward more expensive low sulphur distillatesNote c. This will reduce global demand for heavy sulphur fuel oil (HSFO) as early as June 2019. While HSFO makes up 4% of global oil demand as a bunker fuel for the shipping industryNote d, it is a product of residual oil. Residual oil is an important revenue stream for refiners that process crude streams with higher sulphur content. The regulation is expected to change the economics of refining across the globe in the short term and alter the flow of crude and other products across it.

EF2018 Crude Oil Price Assumptions

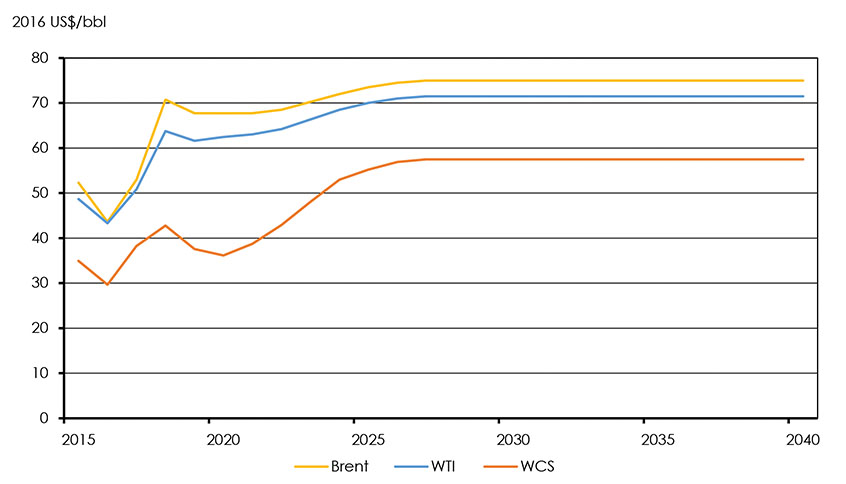

Figure 2.2 shows the Reference Case crude oil price assumptions for EF2018. Brent prices, in constant 2016 US$, are expected to decline in 2019 from current levels and remain at US$68/bbl for the next few years. In 2022, Brent is expected to start increasing and reach US$75/bbl by 2027, where it remains over the projection period. This medium-term price increase reflects the need to develop higher cost resources to replace continuously declining existing supplies and meet increasing global oil demand. The flat, long-term trajectory suggests that oil supply can then grow to meet modest global demand growth at a long-term US$75/bbl price level. The current Brent-WTI discount is assumed to decrease steadily from its current high levels, reaching US$3.50/bbl by 2024, roughly reflecting transportation costs from Cushing, OK to the Gulf Coast.

Figure 2.2: Brent, WTI and WCS Price Assumptions, Reference Case

Description

This chart shows Brent, WTI, and WCS price assumptions, in 2016 USD/bbl, for the Reference Case. Brent increases from $53/bbl in 2017 to $75/bbl by 2027, and remains at $75/bbl until 2040. WTI increases from $50.8/bbl in 2017 to $71.5/bbl by 2027, and remains at $71.5/bbl until 2040. WCS is $38.3/bbl in 2017, increasing to $42.8/bbl in 2018. After 2018, WCS decline to a low of $36.2/bbl in 2020, before increasing to $57.5/bbl in 2027, where it remains for the remaining projection period.

The combined effect of Canadian crude discounts and the IMO regulations are assumed to push the real WCS-WTI differential to US$26.30/bbl in 2020. As discounts are gradually alleviated, prices discounts converge to a sustained value of US$14/bbl by 2027 that reflect quality differences and transportation costs to the Gulf Coast.

CLS is assumed to strengthen as WTI increases, but its discount will increase as production continues to outpace incremental pipeline capacity over the next year, reaching a high of US$7.69/bbl in 2019. The differential will narrow as capacity additions are assumed to come online gradually thereafter, reaching a long-term value of US$2.60/bbl with WTI in 2027Footnote 7, and an implied CLS value of almost US$69/bbl in the long term.

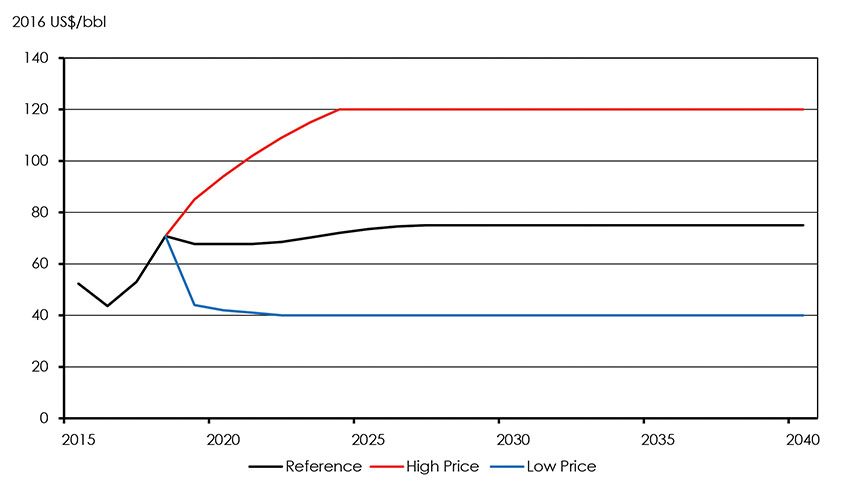

Figure 2.3 shows the Brent price assumptions for the Reference, High and Low Price Cases. The High Price Case presents a future where supply is not as robust and prices need to rise to levels around US$120/bbl to balance crude oil markets in the longer term. The Low Price Case reflects an environment where supply availability is more robust and begins to outpace demand growth, sending prices to $40/bbl in the long term.

Figure 2.3: Brent Price Assumptions, Reference, High Price and Low Price Cases

Description

This chart shows Brent price assumptions, in 2016 USD/bbl, for the Reference, High Price, and Low Price Cases. Brent reaches $70.8/bbl in 2018 for each case. In the Reference Case, Brent increases to $75/bbl by 2027, where it remains until 2040. In the High Price Case, Brent increases to $120/bbl by 2024, where it remains until 2040. In the Low Price Case, Brent decreases to $40/bbl by 2022, where it remains until 2040.

Natural Gas Markets

Current Context

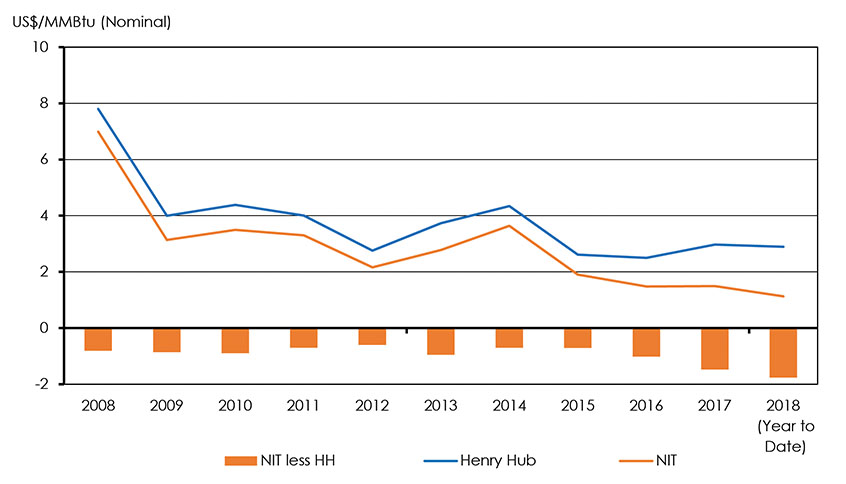

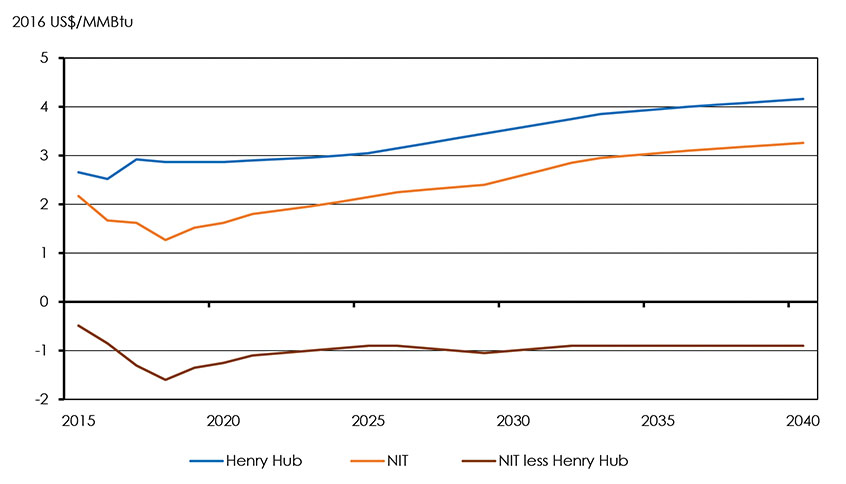

North American natural gas prices have declined considerably over the past decade. Lower prices have been driven by large increases in production, made possible by horizontal drilling and multistage hydraulic fracturing. Henry Hub prices averaged US$7.80 per million British thermal units (MMBtu) in 2008, and declined by almost 50% by 2013. Over the past five years, prices have averaged just over US$3.00/MMBtu. From a low of US$2.49/MMBtu in 2016, prices have increased through 2017, and averaged US$2.89/MMBtu in the first half of 2018. Despite gains in U.S. production, much of which has been natural gas produced with oil, increased demand and increased liquefied natural gas (LNG) exports from the Gulf of Mexico contributed to moderately recovering prices. Figure 2.4 compares historical Alberta (Nova Inventory Transfer (NIT)) and Henry Hub prices for the past 10 years.

Figure 2.4: Henry Hub vs NIT Price, 2008-2018

Description

This chart shows Henry Hub and NIT prices, in nominal USD/MMBtu, from 2008 to 2018. Henry Hub price decreased from $7.8/MMBtu in 2008 to $2.9/MMBtu in 2018. NIT price decreased from $6.99/MMBtu in 2008 to $1.3/MMBtu in 2018. The Henry Hub to NIT differential fell from $0.8/MMBtu in 2008, to $1.8/MMBtu in 2018.

From 2010 to 2013, Canadian natural gas prices averaged just under C$3/GJ. In 2014, prices briefly rebounded and have since continued to decline. Prices averaged C$1.50/GJ in 2017, and C$1.13/GJ in the first half of 2018. Canadian natural gas exports were formerly priced off Henry Hub, minus the cost of transport. However, rapidly rising U.S. production from the Marcellus Basin in Pennsylvania and Ohio now represents the competition for much of Canada’s exports and Marcellus gas sells at a discount to Henry Hub. Canadian natural gas production is also being driven by the value of condensate and natural gas liquids (NGLs) that are co-produced with the gas. This means that some Canadian producers can accept a lower price for their natural gas because of the revenues earned from the accompanying condensate and NGLs. As production shifts westward in western Canada to access the sources richer in condensate and NGLs, pipeline capacity has not kept pace with production. Additional pipeline capacity is being constructed in those areas. The construction can cause interruptions to existing pipeline capacity resulting in periods when some gas in western Canada is sold at very low or even negative prices to find a market. From 2008 to 2015, the average NIT-Henry Hub differential was $0.78/MMBtu, but it averaged US$1.50/MMbtu in 2017 and over $1.75/MMBtu for the first six months of 2018. NIT even exhibited negative pricing on several days throughout 2017 and 2018.

Factors Currently Affecting Natural Gas Markets:

- Increased North American production.

- U.S. LNG exports.

- WCSB and export pipeline capacity.

- Oil sands demand for natural gas.

- Potential Canadian LNG exports.

As producers in western Canada seek new markets in the U.S. or to better compete in existing markets by lowering their costs, pipeline operators have been adjusting capacities on pipelines out of the region and making arrangements to lower transport costs. To access overseas natural gas markets, there are several proposed projects to export LNG from Canada’s west coast, the economics of which have been improving over the past year.

EF2018 Natural Gas Assumptions

In the Reference Case, Henry Hub prices remain flat and stay under US$3.00/MMBtu until 2025 as the market continues to be in a state of over-supply. This is largely due to growing U.S. oil production and the natural gas production associated with it. The natural gas price is assumed to gradually increase thereafter as U.S. industrial demand and LNG exports outpace supply growth, reaching a long-term price of US$4.16/MMBtu in 2040.

The prospect of Canadian LNG export facilities also has important implications for energy supply and demand trends. The future of Canadian LNG exports has been uncertain. Globally, LNG trade is expected to increase as the demand for natural gas rises by over 45% in the next 25 years. Gas markets are expected to be well supplied in the near term and new exports will be required by the mid-2020sFootnote 8. The demand increase could prove to be an opportunity for Canadian LNG export volumes.

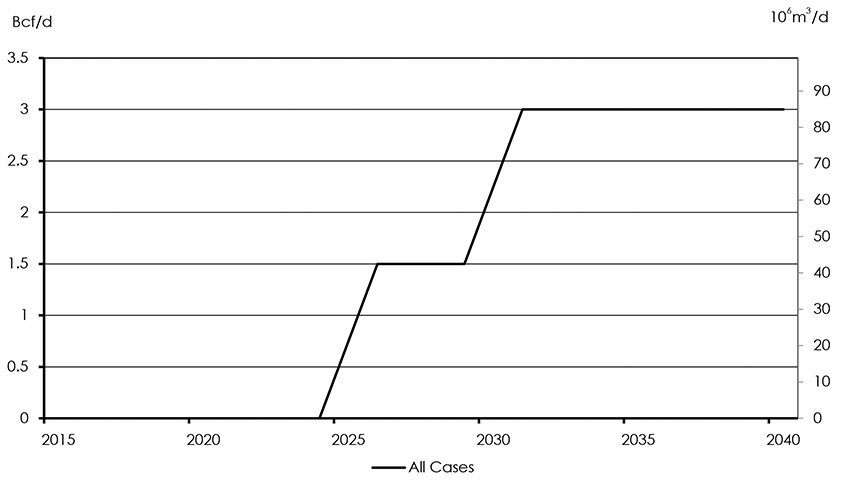

All EF2018 Cases assume LNG exports from British Columbia (B.C.)’s coast beginning in 2025. LNG exports start at 0.75 billion cubic feet per day (Bcf/d) (21.3 million cubic metres per day (106m3/d)) in 2025 and double in 2026 to reach 1.50 Bcf/d (42.5 106m3/d). Phase II is assumed to come online in 2030, increasing total LNG exports to 2.25 Bcf/d (63.7 106m3/d) in 2030 and 3.0 Bcf/d (85.0 106m3/d) in 2031. Figure 2.5 shows the assumed LNG export volumes included in EF2018 analysis for all Cases. The Canadian LNG export volumes included in this analysis are an assumption of what might happen. They do not reflect volumes associated with a particular project or export license. On 2 October, LNG Canada announced a positive final investment decision for its proposed export project. The project will initially export 14 million tonnes per annum (mtpa) (the equivalent of ~1.8 Bcf/d or 51 106m3/d) from two processing units and will have the capability to expand to four in the future. This decision came after the EF2018 analysis period was completed. At this point, the EF2018 LNG assumptions are considered applicable to any new large scale LNG facility, whether it turns out to be the LNG Canada project or a competitor. Additional details should become available once construction of a project is underway and these can be included in future editions of Energy Futures.

Figure 2.5: LNG Exports, All Cases

Description

This chart shows LNG exports for all cases. Exports remain at 0 Bcf/d until 2025. In 2025, exports increase to 0.75 Bcf/d. From 2026 to 2029, exports are 1.5 Bcf/d, and in 2030, exports increase to 2.25 Bcf/d. From 2031 to 2040, exports are 3 Bcf/d.

EF2018 assumes that Canadian natural gas price discounts persist in the near term and are slowly alleviated by 2025 as infrastructure is built and markets for excess natural gas are found. Figure 2.6 shows the NIT-Henry Hub differential decreases from its current high of US$1.60/MMBtu to US$.90/MMBtu in 2025, bringing NIT to US$2.15/MMBtu (C$2.51/GJ). The NIT-Henry Hub differential increases again in 2027 as producers prepare their reserves and boost production for the upcoming phase of LNG exports, reaching US$1.05/MMBtu in 2029, and returning to its long-term levels of US$0.90/MMBtu. While the differential varies, NIT increases constantly over the Reference Case outlook, reaching a value of US$3.26/MMBtu (C$3.69/GJ) by 2040.

Figure 2.6: Henry Hub and NIT Price Assumptions, Reference Case

Description

This chart shows the Henry Hub and NIT price assumptions, in 2016 USD/MMbtu, for the Reference Case. Henry Hub prices increase from $2.9/MMBtu in 2017 to $4.2/MMBtu in 2040. NIT prices increase from $1.6/MMBtu in 2017 to $3.3/MMBtu in 2040. The NIT - Henry Hub differential decreases from $0.5/MMBtu to $0.9/MMBtu in 2040.

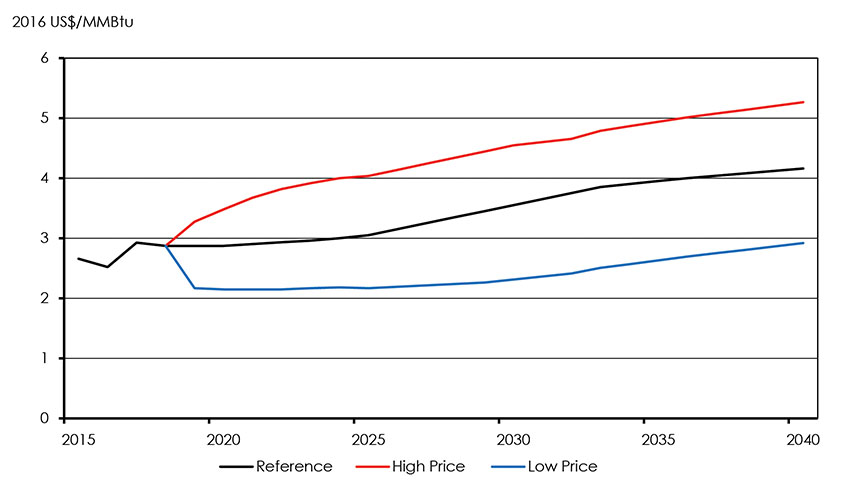

Figure 2.7 shows the Henry Hub natural gas price assumptions for the Reference, High Price, and Low Price Cases. In the High Price Case, Henry Hub rises to US$5.26/MMbtu by 2040. In the Low Price Case, Henry Hub declines to US$2.15/MMbtu by 2020, and gradually rises to US$2.92/MMbtu by 2040.

Figure 2.7: Henry Hub Price Assumptions, Reference, High Price and Low Price Cases

Description

This chart shows the Henry Hub price assumptions, in 2016 USD/MMBtu, for the Reference, High Price and Low Price cases. For each case, prices in 2017 and 2018 are $2.92/MMBtu and $2.87/MMBtu, respectively. Prices increase to $4.2/MMBtu by 2040 in the Reference Case, and $5.3/MMBtu in the High Price Case. In the Low Price Case, prices decrease to $2.15/MMBtu in 2020 and remain there until 2022. After 2022, Henry Hub prices increase to $2.9/MMBtu by 2040 in the Low Price Case.

Climate Policy

Canadian climate policy has evolved rapidly since 2015. Over the past several years, all levels of government have made major policy announcements and continue to move forward with previously announced and implemented climate related plans.

EF2018 includes many recently announced and implemented climate policies. In order to determine whether a policy was included in the analysis, the following criteria were applied:

- The policy was publically announced prior to 1 August 2018.

- Sufficient details exist to model the policy.Footnote 9

- Goals and targets, including Canada’s international climate targets, are not explicitly modelled. Rather, policies that are announced, and in place, to address those targets are included in the modelling and analysis.

See Table A.1 in Appendix A for a list of some recent climate policies and how they are handled in EF2018.

Carbon Pricing

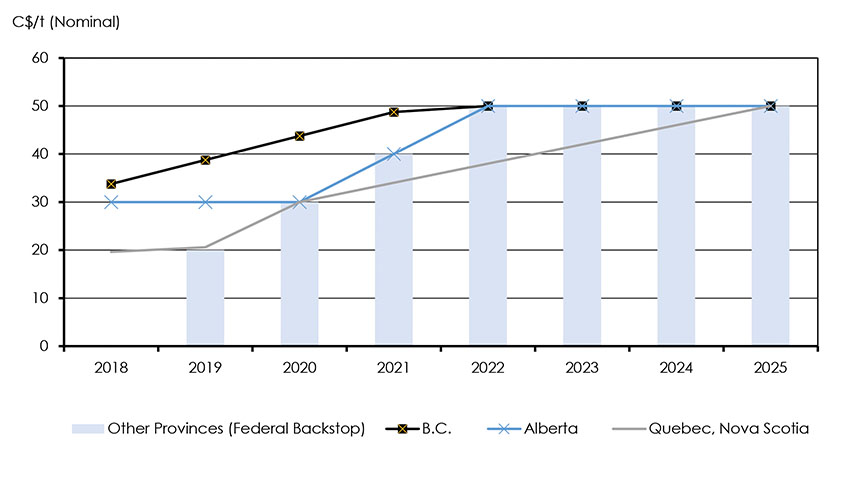

Carbon pricing systems continue to evolve in Canada, as various provinces and territories have announced their intentions for their own carbon pricing systems under the Pan-Canadian Framework. Figure 2.8 breaks down the EF2018 carbon price assumptions by province from 2018 to 2025. EF2018 assumes that the Federal backstop carbon price is binding in the Reference Case. For provinces that have not declared their own carbon pricing system, or have price carbon at a level below the backstop schedule, the backstop schedule–beginning at $20 per tonne in 2019 and rising to $50 per tonne in 2022–is used.

For provinces that have chosen cap-and-trade systems, the future price of carbon will be determined by the supply and demand for emission permits. The outlook for this market price will be uncertain, similar to other market prices such as crude oil and natural gas. Like crude oil and natural gas prices, EF2018 makes simplifying assumptions for the future outlook of carbon pricing. For the two cap-and-trade provinces, Quebec and Nova Scotia, the carbon price is assumed to remain below the federal backstop in the early 2020s, before converging to $50 per tonne in 2025. Post-2025, carbon prices in all provinces and territories remain at $50/tonne in nominal terms Footnote 10.

Figure 2.8: Carbon Pricing by Province, 2018-2025

Description

This chart shows carbon pricing by province from 2018 to 2025, in nominal CND per tonne. In 2018, British Columbia’s carbon price is $33.8/t, Alberta’s is $30/t, Manitoba’s is $25/t, and Quebec’s is $19.6/t. For the remaining provinces, the carbon price is $0/t in 2018, increasing by $10 per year, reaching $50/t by 2022, where it remains until 2040. For British Columbia, Alberta, and Manitoba, carbon prices also increase to $50/t by 2022. For Quebec, prices reach $50/t in 2025.

Carbon Pricing Exemptions and Allocations

Many carbon pricing systems have exemptions and/or permit allocations. One example is the output based allocation approach used for large emitters in the Alberta and federal backstop systems. This system provides an allowable level of emissions for large emitters, and facilities pay for the emissions above that level or receive credits for their emissions below it. This system reduces the average carbon cost for these facilities, but maintains the incentive for emission reductions. In this analysis, emitters face the full carbon price at an end-user level to capture the incentive effect of the carbon price, while the impact of the output based allocations in reducing the overall cost to firms and income effects of the carbon prices is captured in the industrial macroeconomic projections. Other examples include emission units distributed free of charge to industrial emitters in Quebec to avoid carbon leakage in its cap-and-trade system, or point of sale rebates for heating oil in the Northwest Territories, as its residents already face heating costs higher than the national average.

While EF2018 attempts to include available details on current climate policies and carbon pricing systems, these systems are complex, continually being refined, and involve several uncertainties. The primary uncertainty is the federal government’s jurisdiction to enforce the pan-Canadian benchmark for pricing carbon in the event that provinces that have not implemented their own plans that meet the minimum standards, or are actively opting out of implementing a carbon pricing plan. EF2018 makes many simplifying assumptions on Canadian climate policy implementation for the purposes of creating a reasonable outlook for future Canadian supply and demand trends. It should not be taken as direct analysis on any specific policy initiative.

Electricity

Current Context

Canada’s energy system is entering a period of significant change and the electricity sector is expected to play a key role in the transition to a cleaner economy Footnote 11. In the federal government’s Pan-Canadian Framework, four key areas of transition were identified: growth in renewables and low-emitting sources, increasing interconnections to allow the flow of clean power, modernizing the electricity system, and reducing diesel reliance in remote communities.

In spring 2016, the Alberta government unveiled a climate change and emissions strategy based on recommendations put forth by the Climate Leadership Panel. The Alberta government plans to phase out coal-fired electricity generation by 2030. However, this could take place earlier than planned through coal-to-gas conversions. In 2017, two operators announced their plans to retrofit existing coal units to natural gas-fired units as early as 2020. The strategy also calls for the development of 5 000 megawatts (MW) of renewables by 2030. To reach this target the Alberta Electricity System Operator’s (AESO) launched the first Renewable Electricity Program (REP). This competitive process was a success; attracting 600 MW of new capacity with a record low bid price that averages $37/MW.h. In late 2016, the Alberta government announced its plan to transition from the province’s energy-only electricity market to a capacity market framework. The AESO’s ongoing Comprehensive Market Design work is expected to release rules on the capacity market by the end of the year, with a plan to award capacity contracts in 2020/21.

There are uncertainties regarding future carbon capture and storage (CCS) projects in Saskatchewan. Recently the province announced it will not be retrofitting Boundary Dam 4 and 5 with CCS. The two units will retire in accordance with federal regulations (2021 and 2024 respectively).

Ontario’s nuclear refurbishment is proceeding, as the province plans to refurbish 10 units between 2016 and 2033. Work on the first unit (Darlington Unit 2) began in 2016. Refurbishment work on Darlington unit 3 and Bruce unit 6 are scheduled for 2020. Also, Ontario recently announced its plans to keep its Pickering nuclear plant open until 2024. Ontario is also considering a capacity auction framework under the Market Renewal initiative. In a capacity market, power suppliers will be paid a guaranteed fee for their commitment to make resources available when needed.

Factors Currently Affecting Electricity Markets:

- Moderate electricity demand growth in Canada and U.S.

- Federal and regional climate policies such as coal retirement and carbon pricing systems.

- Decline in cost for non-hydro renewables particularly for solar and wind technologies.

In late 2017, electricity was exchanged between Newfoundland and Nova Scotia for the first time through the Maritime Link transmission line. The new connection, which includes 170 kilometres (km) of subsea transmission cables, connects the Muskrat Falls generating station in Labrador to Nova Scotia. The majority of the energy from Muskrat Falls will serve both Newfoundland as well as provide contractual capacity and energy to Nova Scotia. Muskrat Falls is expected to come online in 2020.

Short-term surplus capacity is a common theme in some Canadian regions as illustrated by record levels of electricity exports, wind curtailments, low hydro capacity factors and high reservoir levels in some regions. Quebec’s reservoir reached historic levels of 140.5 TW.h and British Columbia’s reservoirs recorded the third highest level in the past five years (14.5 TW.h). Ontario wind curtailments reached 26% (3.3 TW.h), the highest level in the past five years.

Remote communities primarily rely on expensive diesel-fired generation, while others rely on smaller local or regional electricity grids based on hydro or trucked-in liquefied natural gas (LNG). Many remote communities in northern Canada are exploring opportunities to reduce their reliance on diesel fuel, improve electricity reliability, and reduce emissions. Solar projects currently exist in many Northwest Territories communities although they tend to have limited functionality in the winter months due to reduced sunlight in the region. Despite this limitation, over 900 kilowatts (kW) of installed solar PV capacity helped offset an estimated 200 000 litres of diesel consumption in 2016.

Electricity Assumptions

EF2018 analysis reflects current utility and system operator expectations of future electricity developments in the respective regions, especially for major planned projects, and to guide assumptions on costs of generation for various types of electricity. Table 2.1 shows assumptions for natural gas, solar, and wind costs, including their capacity factors. The timing and magnitude of other forms of generation added over the projection period (such as hydroelectric and nuclear refurbishments) are based on current schedules and plans from utilities, companies, and system operators.

| Capital Cost (C$/kW) | Fixed Operating and Maintenance Costs (C$/kW) |

Variable Operating and Maintenance Costs (C$/MW.h) |

Capacity Factor | |

|---|---|---|---|---|

| Gas (Combined Cycle) | 1 400-1 850 | 20 | 5 | 70% |

| Gas Peaking | 1 040-1 400 | 18 | 5 | 20% |

| Wind (2020) | 1 541 | 24-55 | 0 | 35-50% |

| Wind (2030) | 1 360 | 24-55 | 0 | 35-50% |

| Wind (2040) | 1 200 | 24-55 | 0 | 35-50% |

| Solar (2020) | 1 613 | 20-25 | 0 | 10-20% |

| Solar (2030) | 1 307 | 20-25 | 0 | 10-20% |

| Solar (2040) | 1 100 | 20-25 | 0 | 10-20% |

Technology

Technology’s influence on the energy system can range from marginal to transformative. Which emerging technologies will achieve widespread use is often difficult to predict. Likewise, the nature of future breakthroughs is unknown. The adoption rate of emerging technologies is a key uncertainty to the projections in EF2018.

The core Cases assume moderate technological progress, reflected by factors such as efficiency improvements and cost reductions for well-established technologies. However, there is a high degree of potential for further technological progress, especially as it relates to the increasing ambition of climate policies across the world and the transition to a low carbon economy. These types of changes pose several key uncertainties for Canada’s energy system, and are explored in the EF2018 Technology Case. There is also potential for disruptive technologies to emerge, altering the ways Canadians use energy. They could result in both increases and decreases in energy usage for a variety of end-usesFootnote 12. Additional context and assumptions for the Technology Case are covered in Chapter 4.

- Date modified: