Results

On this page:

- Greenhouse gas (GHG) emissions

- Energy demand

- Electricity

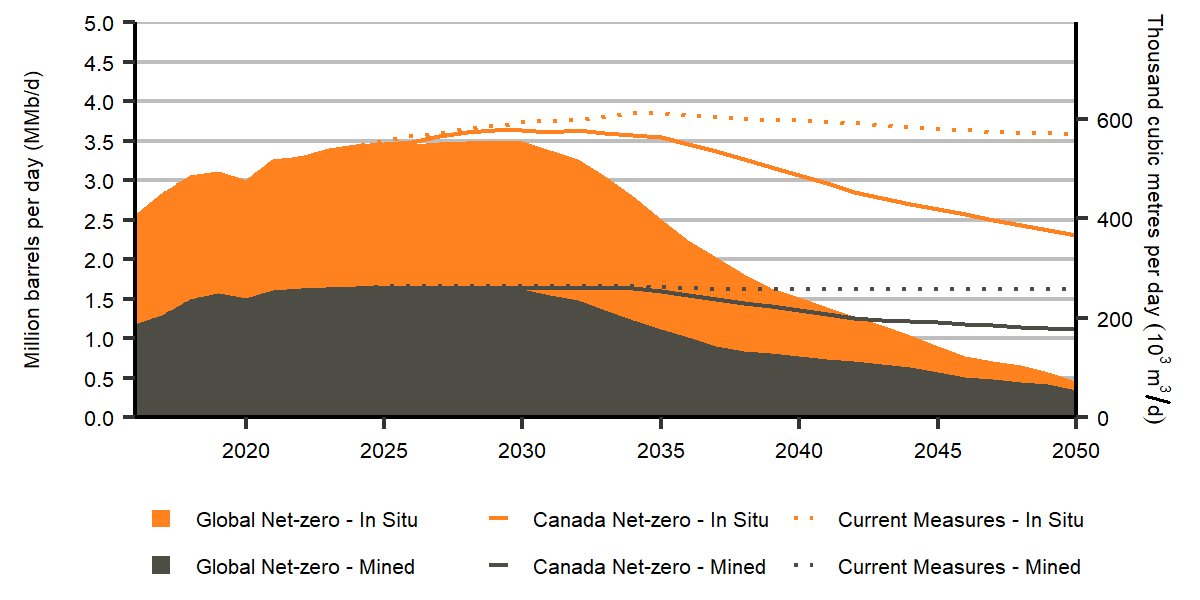

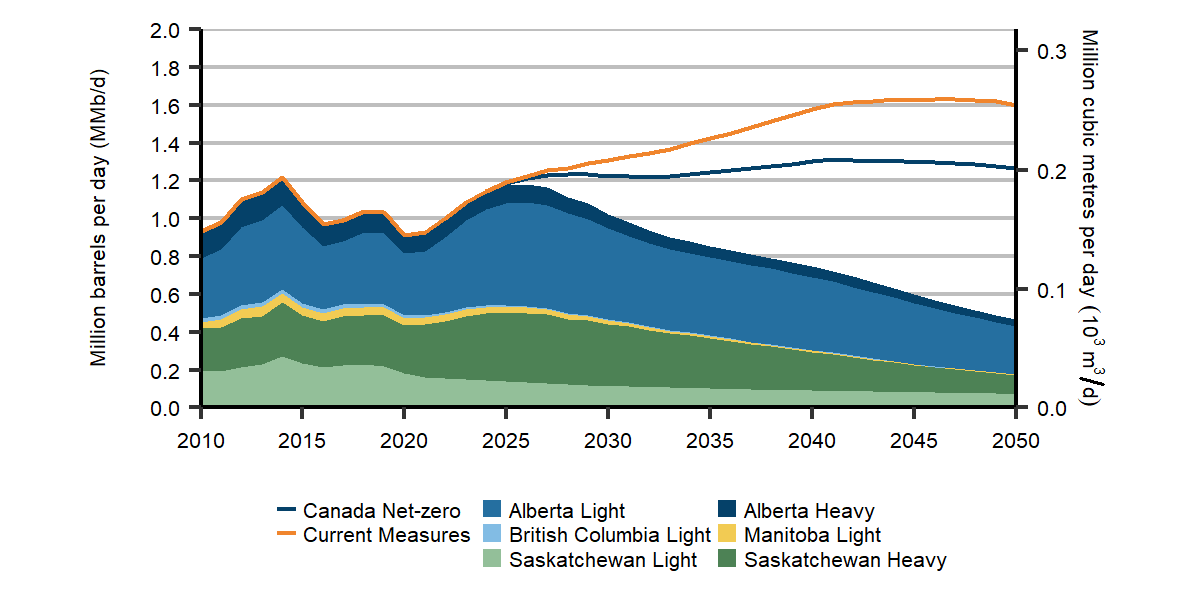

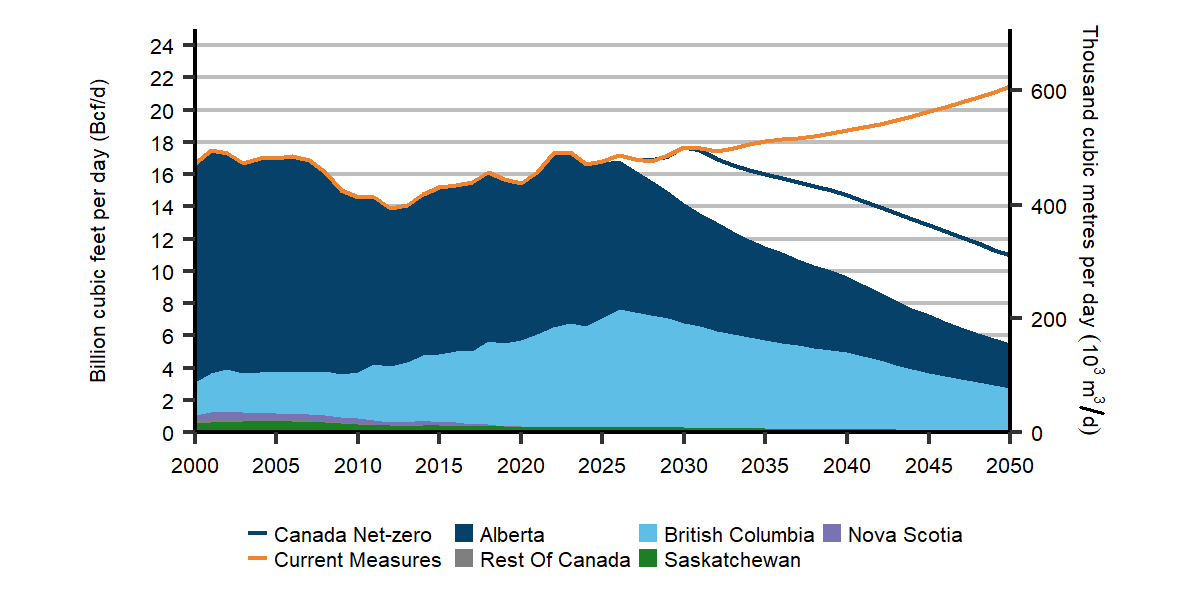

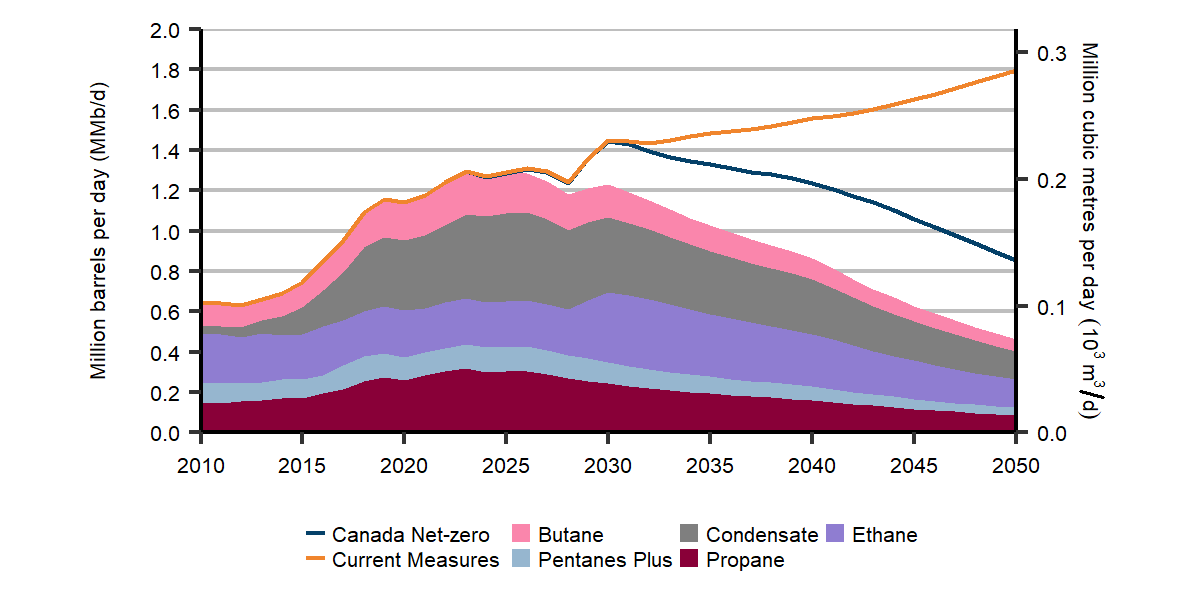

- Oil and natural gas production

- Hydrogen

- Negative emissions

- Macroeconomics

This chapter presents results of the EF2023 projections. These projections are not a prediction, but instead illustrate possible futures based on the scenarios and assumptions described in the previous chapter. Many factors and uncertainties will influence future trends. Key uncertainties are discussed in each section of this chapter.

The data supporting this discussion, including full data tables for all three scenarios, is available in the “Access and Explore Energy Futures Data” chapter.

All dollar figures throughout the report are in Canadian dollars unless stated otherwise.

Greenhouse gas (GHG) emissions

In December 2015, most countries in the world, including Canada, adopted the Paris Agreement. The overarching goal of the agreement is to hold “the increase in the global average temperature to well below 2°C above pre-industrial levels” and pursue efforts “to limit the temperature increase to 1.5°C above pre-industrial levels.” These efforts are because the United Nation’s Intergovernmental Panel on Climate Change indicates that crossing the 1.5°C threshold risks far more severe climate change impacts, including more frequent and severe droughts, heatwaves and rainfall. Fundamental to achieving the goal of the agreement is dramatically reducing global GHG emissions.

Canada’s long-term climate goal is reaching net-zero GHG emissions by 2050.Footnote 7 Given that reaching net-zero emissions by 2050 is the central focus of both our net-zero scenarios in EF2023, GHG emission trends are vital to our analysis. Around 80% of Canada’s total emissions are related to the production and consumption of energy, so the GHG emission and energy supply and demand projections in EF2023 are tightly linked.

Which sectors emit the most in Canada? How do emissions change over the projection?

Discover the data for yourself using our interactive visualization tool. View emissions by sector.

Canada’s GHG emission profile

From 2000 to 2019, Canada’s GHG emissions have fluctuated between just below 700 megatonnes (MT) to around 750 MT. In 2020, emissions fell 8% from 2019 levels. Much of this decrease was a result of lower energy use in response to actions to reduce the spread of COVID-19, such as travel restrictions and closing businesses. The decrease in emissions from 2019 to 2020 is the largest drop in emissions recorded over the period for which data is available (1990 to 2021).

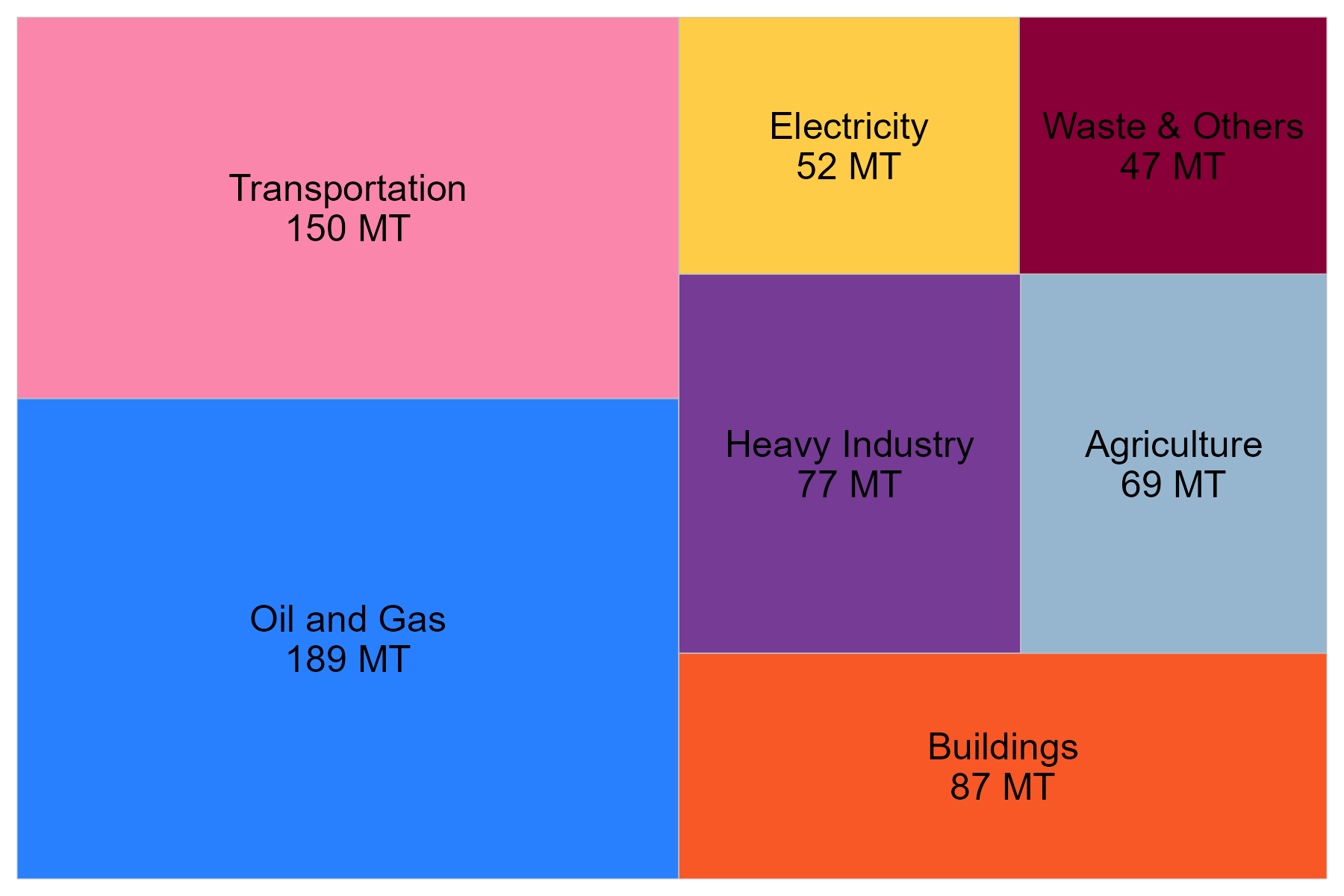

In 2021, emissions were 653 MT, or a 1.2% increase from 2020 levels, but 7.3% lower than in 2019. Figure R.1 shows Canada’s GHG emissions in 2021,Footnote 8 categorized by economic sector.Footnote 9

Figure R.1: GHG emissions by economic sector, 2021

Description

Description: This square area chart shows the relative share of GHG emissions by economic sector in 2021. The oil and gas sector emitted 189 MT, transportation 150 MT, buildings 87 MT, heavy industry 77 MT, agriculture 69 MT, electricity 52 MT, and waste & others 47 MT.

Of the sectors in Figure R.1, GHG emissions fell in electricity (-56%), heavy industry (-13%), transportation (-4%), and waste and others (-10%) from 2005 to 2021. GHG emissions increased in oil and gas (+13%), buildings (+2%), and agriculture (+8%) over that same period. Consistent with the past 30 years, about 80% of GHG emissions in 2021 were related to the production and consumption of energy, mostly from the combustion of fossil fuels. The remaining 20% of emissions are from other activities such as agriculture, waste management, and certain industrial processes.

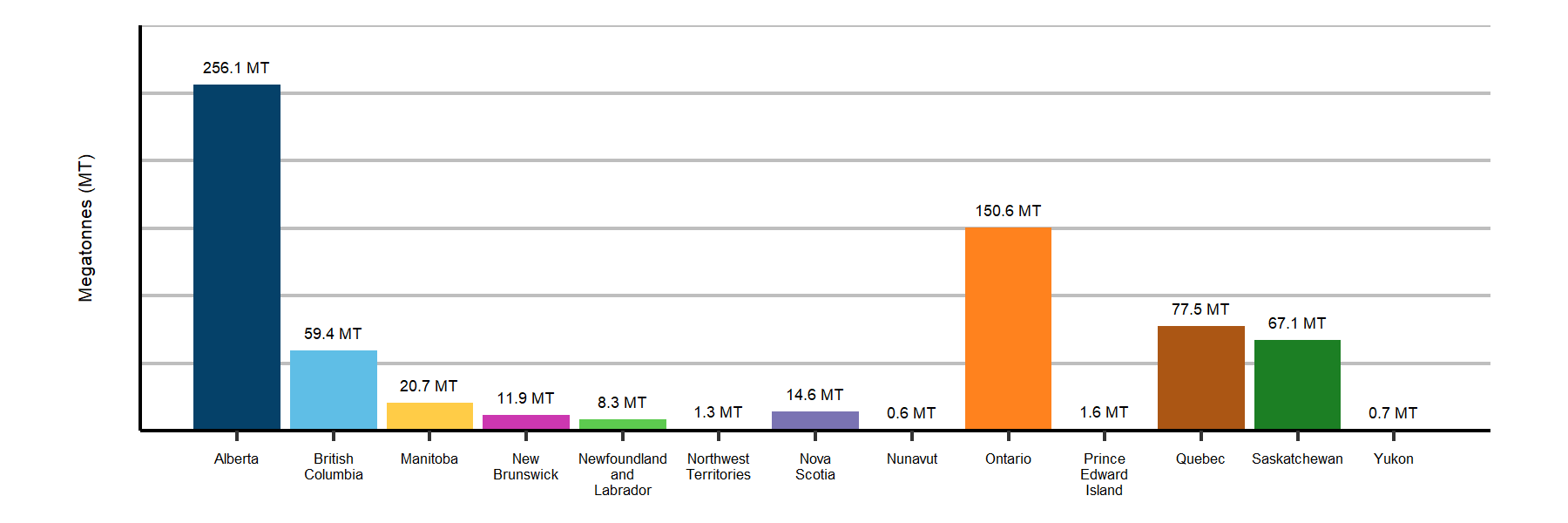

Canada’s GHG emission profile varies significantly among the provinces and territories, as shown in Figure R.2.

Figure R.2: GHG emissions by province and territory, 2021

Description

Description: This column chart shows GHG emissions by province in 2021.

Alberta emits the most, at slightly over 250 MT, followed by Ontario, Quebec, Saskatchewan, and BC.

Detailed data and a more thorough description of Canada’s GHG emission profile can be found in Canada’s National Greenhouse Gas Inventory Report, published by Environment and Climate Change Canada (ECCC).

GHG emission projections

This section provides an overview of our projections of GHG emissions in all three scenarios. The sections that follow explore the energy and GHG emissions trends for the individual segments of the energy system.

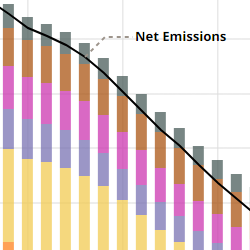

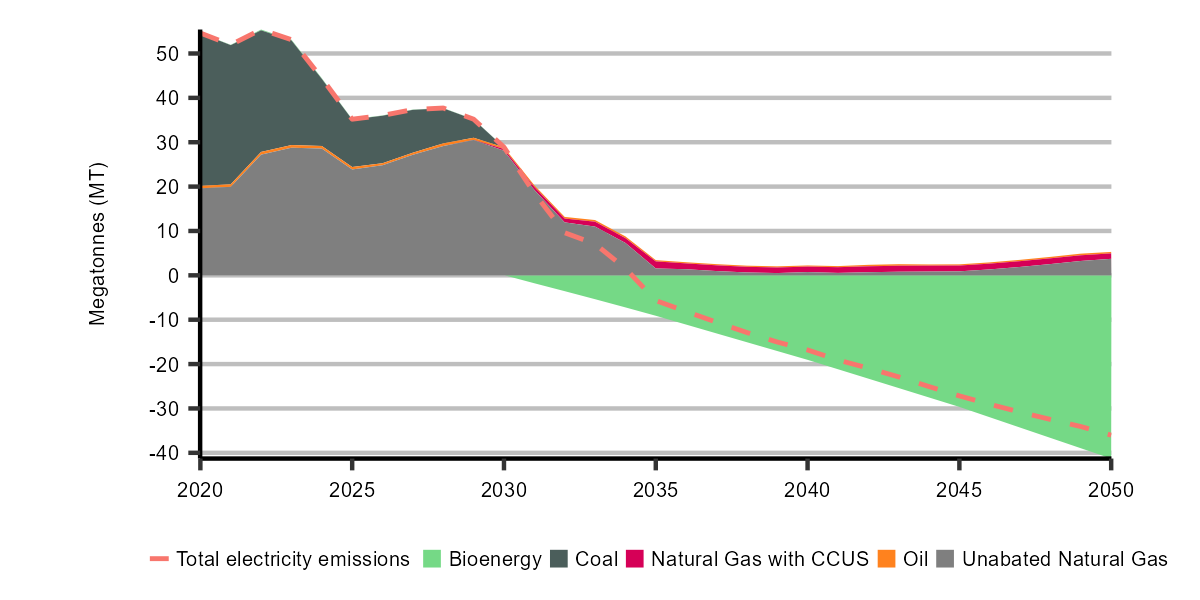

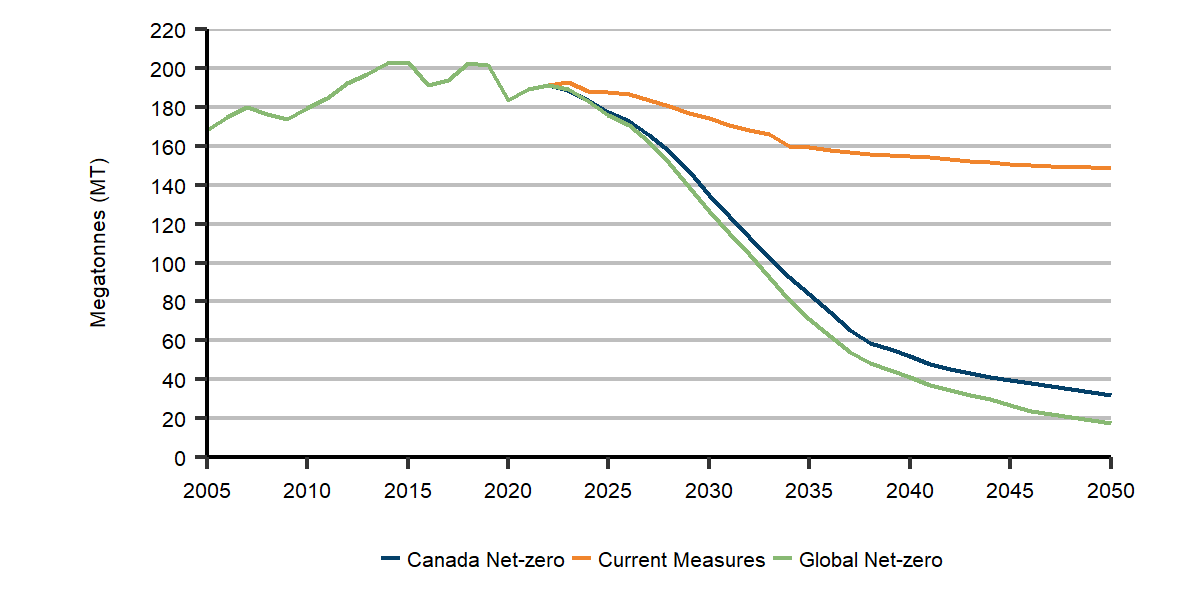

Net economy-wide GHG emissions fall to zero by 2050 in the Global and Canada Net-zero scenarios, which is a predetermined outcome due to the nature of the analysis. Total emission trends are similar in the two scenarios given they share similar climate policy assumptions. In the Current Measures Scenario, we project emissions to be 566 MT by 2050, 13% lower than 2021 levels. This projection of GHG emissions in the Current Measures Scenario only includes policies currently in place during the analysis and does not reflect recently announced policies that are in development. Figure R.3 shows total net emissions in all three scenarios and figure R.4 shows emissions by economic sector in the Global Net-zero Scenario.

Figure R.3: Total GHG emissions, all scenarios

Description

Description: This line chart shows total GHG emissions in all three scenarios.

Emissions increase from 2020 to 2023, and then gradually decline to 0 MT in both net-zero scenarios. Emissions decline modestly throughout the projection period in the Current Measures Scenario.

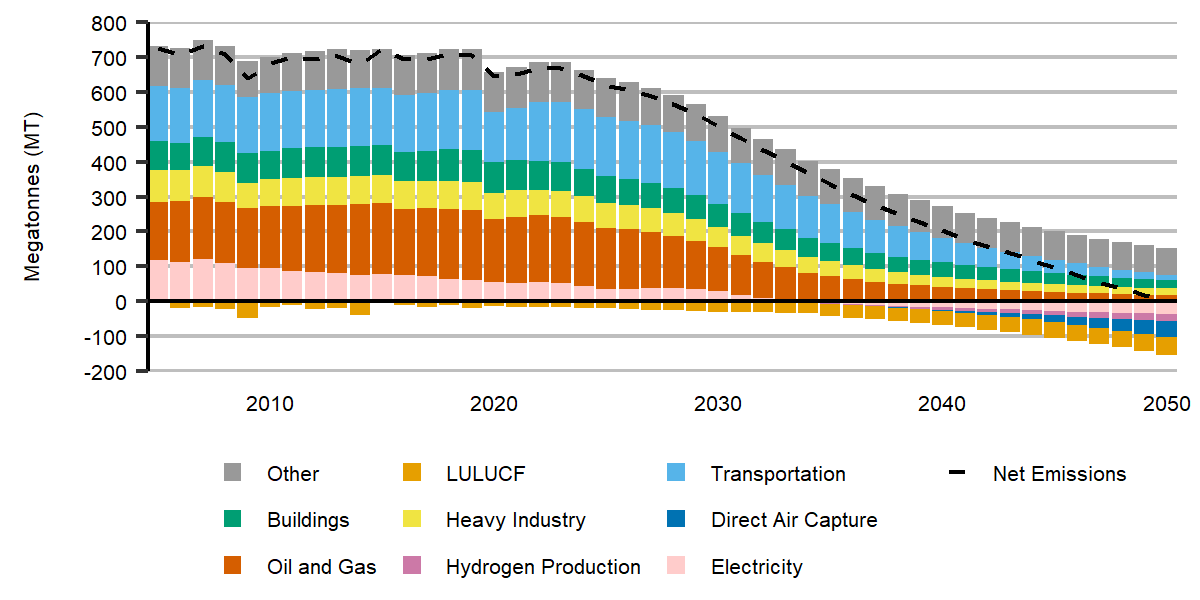

Figure R.4: GHG emissions by economic sector, Global Net-zero Scenario

Description

Description: This stacked column chart shows the evolution of total sectoral GHG emissions in the Global Net-zero Scenario. The sectors are electricity, hydrogen production, oil and gas, direct air capture, heavy industry, buildings, transportation, LULUCF, and other.

The figure shows that net emissions gradually decline to zero by 2050. Transportation and oil and gas show the steepest decline in the projection period. In the 2040s, electricity, hydrogen production, and direct air capture follow LULUCF in becoming increasingly significant sources of negative emissions.

Which GHG emissions are included in EF2023

Parties to the United Nations Framework Convention on Climate Change (UNFCCC) estimate and report their historical GHG emissions according to guidelines developed by the UNFCCC. This report is referred to as a country’s National Inventory Report (NIR). The UNFCC’s guidelines for calculating GHG emissions aim to make reporting by countries transparent, consistent, comparable, complete, and accurate. ECCC is responsible for preparing and submitting Canada’s national GHG inventory to the UNFCCC.

Each country’s NIR covers emissions (and removals) of GHGs, including carbon dioxide, methane, nitrous oxide, and various other gases that have heat-trapping potential. GHG emissions are calculated as those that occur within a country. For example, if country A produces and exports natural gas to country B, any GHG emissions resulting from producing that natural gas (such as the GHG emissions from facilities that process raw natural gas) are attributed to country A, while emissions related to the combustion of that natural gas are attributed to country B.

The historical GHG emissions that we report in EF2023 align with Canada’s NIR. The latest historical emissions data available is from 2021. The GHG emission projections in EF2023 are estimates resulting from the Energy Futures Modeling System, relying on inputs based on the scenario premise and assumptions we describe in the previous chapter. In various publications, such as the Emission Reduction Plan and Biennial Report to the UNFCCC, ECCC produces the official analysis of Canada’s current emissions outlook and performance against its climate commitments.

In both net-zero scenarios, all sectors have much lower emissions by 2050, compared to 2021 levels. Table R.1 shows the GHG emissions in each sector in 2050, and briefly describes the transformations that occur in each sector.

Table R.1: Change in emissions from 2021 to 2050 by economic sector, and key outcomes, Global and Canada Net-zero scenarios

| Sector | 2021 | 2050 | Key outcomes – Net-zero scenarios | |

|---|---|---|---|---|

| Global Net-zero | Canada Net-zero | |||

| Total | 653 MT | 0 MT | 0 MT |

|

| Buildings | 87 MT | 25 MT | 25 MT |

|

| Heavy industry | 77 MT | 19 MT | 19 MT |

|

| Transport | 150 MT | 15 MT | 14 MT |

|

| Electricity | 52 MT | -37 MT | -36 MT |

|

| Oil and gas | 189 MT | 17 MT | 32 MT |

|

| Low-emitting hydrogen production | 0 MT | -21 MT | -25 MT |

|

| Direct air capture (DAC)Definition* | 0 MT | -46 MT | -55 MT |

|

| Agriculture | 69 MT | 50 MT | 49 MT |

|

| Waste and others (coal production, light manufacturing, construction, and forest resources) | 47 MT | 26 MT | 26 MT |

|

| Land Use, Land-Use Change and Forestry (LULUCF)Definition* | -17 MT | -50 MT | -50 MT |

|

Energy demand

This section first discusses secondaryFootnote 10 (or “end-use”) energy demandFootnote 11 projections by reviewing energy use by sector of the economy and their associated GHG emissions. We then describe the primary energy demandFootnote 12 projections. End-use demand includes consumption of energy, including electricity and hydrogen, but not the energy used to produce electricity and hydrogen.

We make projections about energy demand by simulating the energy choices of households and businesses, including the energy technologies and fuels they use. Economic activity, population growth, technology characteristics, energy prices, and climate policies all influence the model’s outcomes.

Our energy demand projections also rely on projections about the need for energy services. Energy services are not the energy or technologies we use, but rather the things that energy enables us to do, like heat our homes, travel from place to place, or run equipment at a business. This includes projections of the output from various industries, the number of homes and businesses requiring heating and cooling, and the number of kilometres that passengers and goods move. The eventual level of energy services required may be different than in our scenarios, which would impact our projections of energy use.

In all three scenarios, energy use increases in the near term

We estimate Canadian end-use energy demand increased 4% in 2022, largely a result of increasing industrial and oil and gas activity, as well as a return to near pre-pandemic transportation levels. We project that demand growth continues in 2023 and 2024, but at a slower pace.

In the long term, energy use falls in both net-zero scenarios

While we project continuing economic and population growth, end-use demand declines by 22% from 2021 to 2050 in the Global Net-zero Scenario and 12% in the Canada Net-zero Scenario. As we describe in the following sections, this decline is largely due to switching to different technologies and fuels, more efficient use of energy, and lower activity levels in some sectors. In particular, switching from fossil fuel to electricity can reduce overall energy demand significantly because electric devices often use energy more efficiently. For example, 30% or less of the energy in gasoline is used to propel vehicles with much of the remainder being lost to heat. In an electric vehicle (EV), much more of the energy stored in the vehicle’s battery is converted to movement. The combined impact of these changes reduces Canada’s energy intensity. The energy intensity of the economy, often measured as energy use per $ of real gross domestic product, declines by 2.2% per year in the Global Net-zero Scenario, and 1.7% per year in the Canada Net-zero Scenario. Energy intensity has typically fallen about 1% per year on average in recent decades.

In the Current Measures Scenario, energy use is relatively stable

In the Current Measures Scenario, energy use is relatively stable until 2040. After 2040, energy use begins slowly increasing again. This increase is because climate policies do not strengthen beyond 2030, but the economy and population continue to grow, increasing energy use. Figure R.5 shows the changes in end-use energy demand in each scenario.

Figure R.5: Change in end-use energy demand by sector, 2021 to 2050, all scenarios

Description

Description: This column chart shows the percentage change in end-use energy demand by sector from 2021 to 2050. It compares the 1990 to 2019 historical period with the three scenarios during the 2021 to 2050 period. The sectors are residential, commercial, industrial, and transportation.

Both net-zero scenarios show declines in end-use energy demand in all sectors. Conversely, Current Measures sees an increase in all sectors, although at a slower rate than during the 1990 to 2019 period.

In all scenarios, households and businesses continue to receive the energy services much like they do today, like being able to reliably heat their homes or travel from place to place. As described in the following sections, we project considerable changes to the types of fuels and technologies that power the energy system in the future, but little change to the energy services Canadians receive.

Key trends: energy demand

Rapid adoption of devices that use electricity, like EVs and heat pumps in the net-zero scenarios.

In both net-zero scenarios, clean fuels such as hydrogen and bioenergy, along with CCUS, play an increasing role in areas that are harder to electrify.

Energy efficiency improves steadily over the projection period.

Residential and commercial

The residential sector made up 13% of Canada’s end-use energy demand, and 6% of its GHG emissions in 2021. The commercial sector, which includes buildings like offices, restaurants, and schools, made up 11% of Canada’s end-use energy demand, and 7% of its GHG emissions in 2021. Most energy use in both sectors is electricity and natural gas, and in some regions refined petroleum products (RPPs) and biomass are also key fuels. When combined, GHG emissions in both sectors are referred to as the “buildings sector” for the purposes of GHG emission reporting. GHGs in the buildings sector are primarily the result of burning natural gas and fuel oil for heating buildings and water.

In the Global and Canada Net-zero scenarios, we project that energy use patterns change considerably in both sectors. The electrification of space and water heating, along with rapid improvements in the efficiency of buildings, are core to this sector’s transformation.

In the Global Net-zero Scenario, we project that building shell efficiency (or how well buildings resist losing heated or cooled air to the outside environment) of the entire residential building stock improves by 50% from 2021 to 2050. In the commercial sector, this improvement is slightly slower at 43%. Efficiency gains are driven by energy retrofits of existing buildings and increasingly strict building codes for new buildings, with all new homes built to a “net-zero-ready” standard by 2030. Efficiency improvements are similar in the Canada Net-zero Scenario. These efficiency improvements are important because residential and commercial floorspace both grow around 50% over the projection period as new houses and buildings are built. In the Current Measures Scenario, less ambitious policy measures result in slower improvements in efficiency.

Fuel-switching is necessary to achieve net-zero

In both net-zero scenarios, efficiency improvements support achieving net-zero, but switching existing fossil fuel heating devices to non-emitting options is necessary to achieve net-zero emissions. In many regions, heating needs are currently met with natural gas or heating oil furnaces. Due to our assumptions about climate policies and technology cost reductions, electric heat pumps steadily become the device of choice when households and businesses replace their furnaces. Heat pumps also grow in regions that currently rely heavily on electric baseboard heating. Because heat pumps are very energy efficient, switching from baseboard heating to heat pumps helps limit electric demand growth in the building sector. Currently, heat pumps are gaining popularity in some regions in Canada but are used sparingly in many regions. More information about the characteristics of heat pumps is in the text box “Spotlight on Heat Pumps.” Importantly, our projections are based on parameters about the willingness of households and businesses to adopt new technologies like heat pumps. However, societal preferences change over time, which could change the adoption rates of heat pumps, or any of the other technologies we discuss in this chapter.

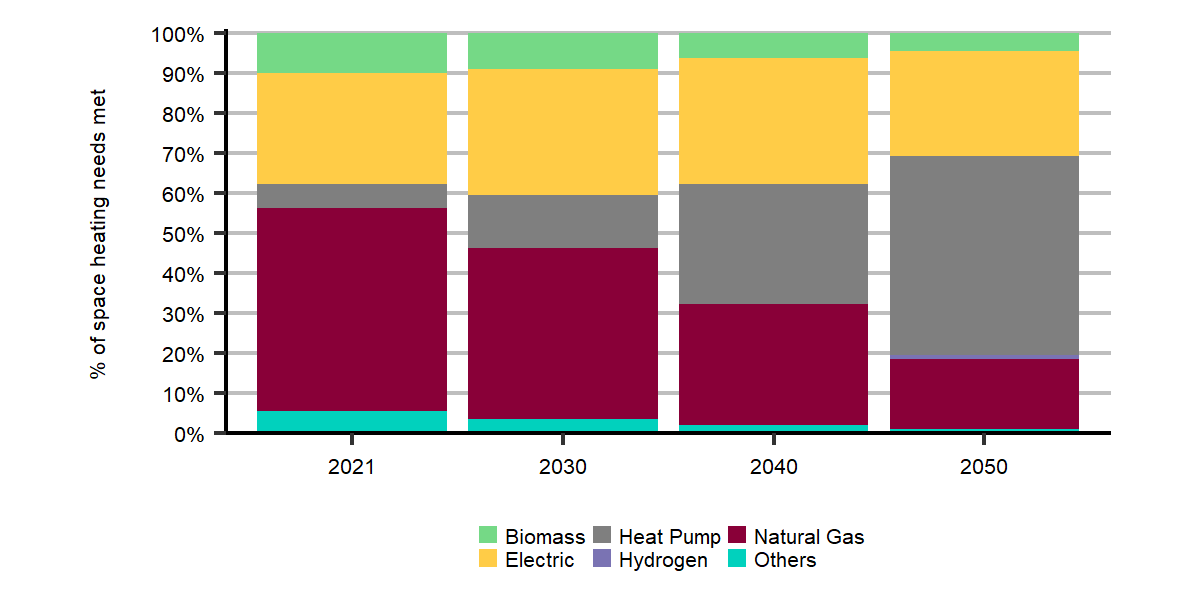

Heat pump use increases in both net-zero scenarios, but some gas and oil furnaces remain

In both net-zero scenarios, heat pumps provide about 50% of residential space heating needs by 2050, up from 6% in 2021, as shown in Figure R.6. This is similar in the commercial sector as heat pumps provide around half of space heating needs by 2050. While heat pumps dominate new heating technology installations by the mid-2030s, the rate of change in the residential and commercial sectors tends to be slow as most households and businesses usually replace devices near the end of their useful lives. As a result, we project that some natural gas and heating oil furnaces remain in 2050 in both net-zero scenarios. Efficiency improvements and blending fossil fuels with low-carbon fuels such as hydrogen and renewable natural gas helps reduce the emissions from these buildings. By 2050, approximately 13% of the energy used in gas-fired residential and commercial space and water heating is renewable natural gas, and 7% hydrogen.

Figure R.6: Residential space heating by technology, Global Net-zero Scenario

Description

Description: This stacked column chart shows the share of residential space heating by technology in the Global Net-zero Scenario for each decade until 2050. The technologies are biomass, heat pump, natural gas, electric, hydrogen, and others.

In 2021, natural gas made up around 50% of all residential space heating. This share decreases to less than 20% by 2050 and is largely replaced by a growing share of electric heat pumps.

Spotlight on heat pumps

Electric heat pumps are a key technology for building decarbonization in our net-zero scenarios. Heat pumps have been used globally for decades and most Canadians already have technologies that operate under the same principles in their homes: refrigerators and air conditioners. Heat pumps work by moving heat from one space (a source) to another (a sink). The two most common sources for heat pumps are the outside air and the ground. Electricity is used to transfer heat from the air or ground to a sink, either the indoor air or water of a building. This process can be reversed so that the building acts as a source and the air or ground acts as a sink, cooling the building instead of heating it. Therefore, heat pumps can be used year-round in Canada to regulate indoor temperatures.

Since heat pumps move heat instead of generating it, they can achieve efficiencies far beyond those of conventional heating methods like a natural gas furnace. Heat pumps currently on the market can achieve efficiencies of 300-550% depending on the temperature of the source and the size of the heat pump.

Air-source heat pumps are lower cost and cheaper to install than ground-source heat pumps and subsequently makeup most of the installed heat pumps across Canada, both now and in our scenarios. However, as the outside air temperature decreases, air source heat pumps become less efficient. Currently, cold climate air-source heat pumps can still achieve efficiencies of 180% at -15°C and still function well up to -25°C. Below this temperature, however, they have difficulty supplying enough heat to a home. As temperatures decrease, homes lose heat more quickly and more energy is required to extract heat from the air.

Canadians that live in climates that drop below -25°C and wish to install heat pumps have two options to heat their homes even on the coldest of days. First, when installing a heat pump, they can leave their current heating system as a backup or install a new backup at the same time. This backup can be any conventional technology used to heat a home, such as a natural gas furnace or electric resistance heating. Secondly, Canadians can choose to invest in a ground-source heat pump instead. Even in the coldest climates in Canada, the ground retains significantly more heat than the air and therefore can efficiently provide heat all winter.

Further information on heat pumps, including functionality, technical specifications, and installation is available from Natural Resources Canada’s Heating and Cooling With a Heat Pump.

Total energy use in the residential sector declines by 22% from 2021 to 2050 in the Global Net-zero and Canada Net-zero scenarios. While overall demand decreases, electricity use grows at 1.2% per year over the projection period, largely because of steady growth of electric heating with heat pumps. As more homes switch to heat pumps and electric hot water heating, demand for natural gas falls steadily. In the Global Net-zero Scenario, residential natural gas demand is 72% lower in 2050 compared to 2021, and 73% lower in the Canada Net-zero Scenario. Energy use from at-home charging of EVs is accounted for in the transportation sector, which we describe later in this chapter.

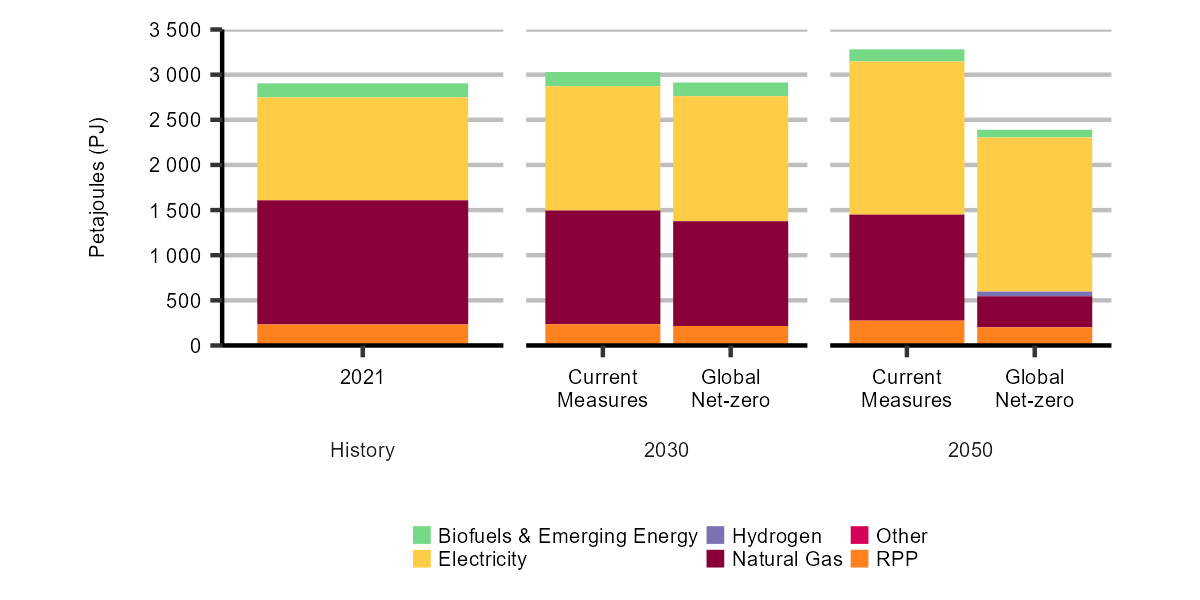

In the Current Measures Scenario, the residential and commercial sectors show steady improvements in efficiency plus some switching to electricity-based heating. However, the pace of change is much slower than in the net-zero scenarios. Natural gas demand in these sectors declines by 18% from 2021 to 2050, while electricity use also increases at a pace similar to the past two decades. Figure R.7 shows total electricity and natural gas demand in the Global Net-zero and Current Measures scenarios.

Figure R.7: Combined residential and commercial buildings energy use by fuel, Global Net-zero and Current Measures scenarios

Description

Description: This stacked column chart shows combined residential and commercial buildings' energy use by fuel in 2021 and in the Global Net-zero and Current Measures scenarios. The fuels are biofuels & emerging energy, hydrogen, electricity, natural gas, RPP, and other.

Electricity and natural gas were the main fuels in 2021, and their share remains similar in the Current Measures scenario over the projection period. The Global Net-zero Scenario sees a significant overall decrease in energy use, most of which comes from a decline in natural gas use as it is gradually replaced by electricity.

Residential and commercial GHG emissions

GHG emissions from residential and commercial buildings follow the energy demand trends we describe above. GHG emissions from the buildings sector track closely to the volume of natural gas and heating oil used. In the Global Net-zero Scenario, GHG emissions in the buildings sector fall from 87 MT in 2021 to 25 MT in 2050, a 71% decrease, with very similar reductions in the Canada Net-zero Scenario. In both net-zero scenarios, emissions from the buildings sector remain positive in 2050 but Canada overall achieves net-zero due to negative emissions occurring in other sectors. In the Current Measures Scenario, emissions decline more slowly in the buildings sector, reaching 64 MT in 2050, a 27% decline.

Industrial

The industrial sector accounted for 54% of Canada’s end-use energy demand in 2021, making it the largest in terms of energy use. The industrial sector is diverse, with several sub-sectors, including oil and natural gas, and various heavy industries like cement, pulp and paper, and iron and steel. The sector is also diverse in terms of energy use, with natural gas making up the largest share of fuel use at 49% in 2021, followed by RPPs (28%), electricity (14%), and biofuels (8%). The main use of energy in the industrial sector is to produce heat, which is used in different industrial processes. Energy commodities such as RPPs and natural gas liquids are also used as non-energy feedstockDefinition* in sectors such as chemicals and fertilizer production.

How does energy demand change over time in the industrial sector?

Discover the data for yourself using our interactive visualization tool. Check out the projected energy mix for end-use demand in the industrial sector.

Industrial GHG emissions are mainly from oil and gas and heavy industry

In 2021, the oil and natural gas sector emitted 189 MT, 29% of Canada’s total emissions. Heavy industry made up 12% of total emissions in 2021, or 77 MT.

This section focuses mostly on the energy use and GHG emission trends in heavy industry. We describe the trends for the oil and natural gas sector in the “Oil and natural gas production” section.

In both net-zero scenarios, new technology, CCUS, and fuel switching are key changes in heavy industry

In the Global and Canada Net-zero scenarios, the changes that occur in the sector to reduce GHG emissions is varied due to unique processes specific to each industrial subsector. However, the primary factors driving change are technological innovation, the application of CCUS technology, and fuel switching. In heavy industry, there are two major emissions sources: emissions from the combustion of fossil fuels to create high temperature heat and process emissions that occur from chemical or physical reactions in the production process itself.

Lower costs and stronger climate policies drive new technology deployment

New industrial technologies are adopted in the net-zero scenarios as they become more widely available at lower costs, and as producers look for options to respond to strengthening climate policies. For example, in the aluminum production sector, the use of inert anodes becomes an increasingly economic choice. Compared to carbon anodes,Definition* the benefit of inert anodesDefinition* is that carbon dioxide (CO2) is no longer released as a byproduct of the aluminum smelting process.

Another example of technology innovation occurs in the iron and steel industry. Most new steel produced in Canada occurs by reacting iron ore with coal, which creates both combustion and process emissions. In both net-zero scenarios, iron and steel producers use a mix of technologies that rely on electricity, natural gas with CCUS, and hydrogen to decarbonize the industry. Steel can also be recycled using 100% electricity and producers increasingly use this pathway where scrap steel is available.

CCUS becomes an important decarbonization option in the industrial sector

CCUS becomes an important decarbonization option where a production process requires high-temperature heat and/or has significant process related emissions. CCUS is a suite of technologies that capture CO2 from facilities to either store it in geological formations underground or use in other processes, like permanent mineralization in concrete. Instead of being permanently stored, there are also other potential uses for captured carbon, such as producing synthetic fuels.

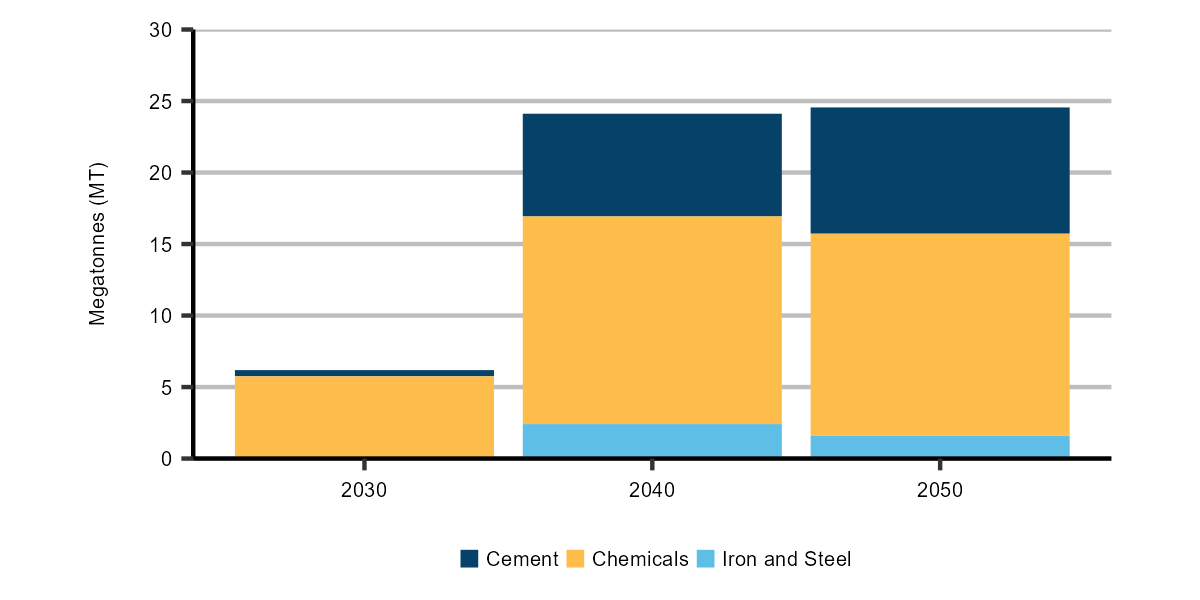

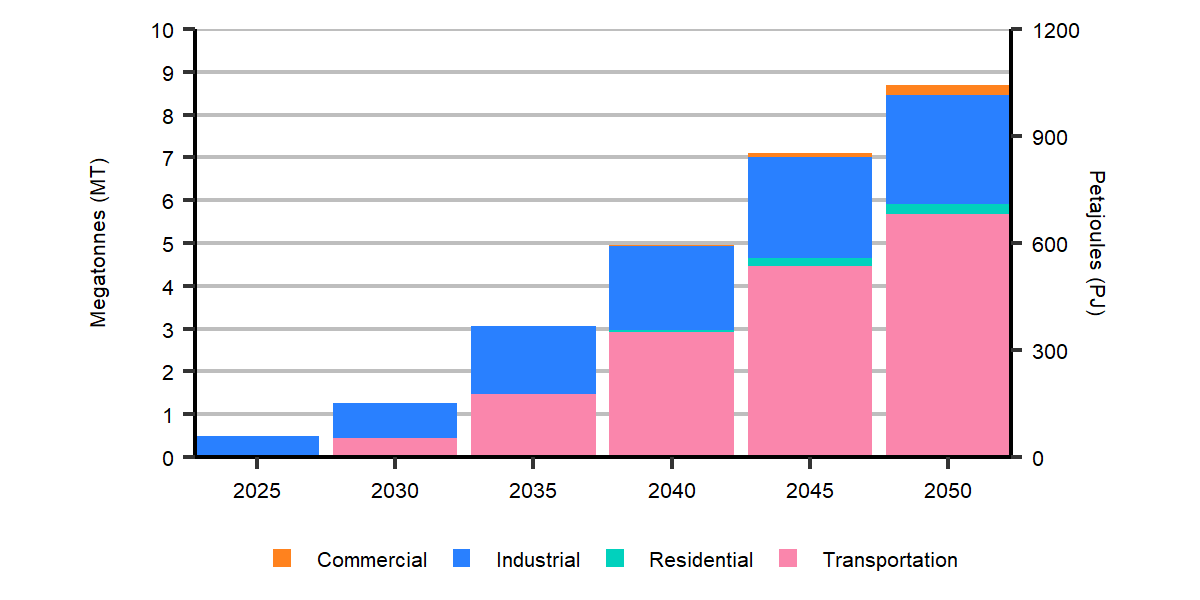

In heavy industry, several sectors increasingly use CCUS over the projection period in both net-zero scenarios, as shown in Figure R.8. We project the heavy industry sector captures a total of 6 MT of GHG emissions in 2030, increasing to 24 MT by 2040 in the Global Net-zero Scenario, after which CCUS in the sector is relatively stable. This excludes the carbon captured in the electricity and oil and gas sectors, which we describe later in this chapter. In the Canada Net-zero Scenario, CCUS plays a similar role in heavy industry.

Figure R.8: GHG emissions captured using CCUS in heavy industry, Global Net-zero Scenario

Description

Description: This stacked column chart shows industrial CCUS in 2030, 2040, and 2050 in the Global Net-zero Scenario. It is broken down into three sectors: cement, chemicals, and iron and steel.

In 2030, most CCUS is deployed in the chemicals sector. CCUS then increases fourfold by 2040, with the cement and iron and steel sectors also becoming major adopters of CCUS.

Fuel-switching is an important trend in both net-zero scenarios

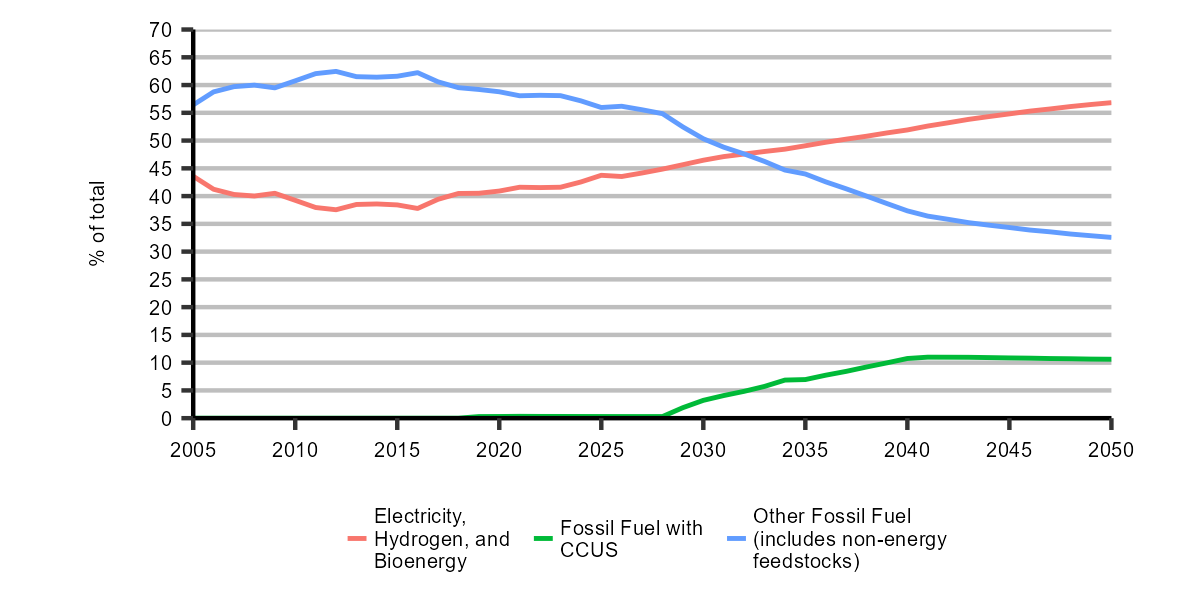

Various climate policies change the relative cost of fuels and industries respond by switching to low- or non-emitting energy sources when feasible. As shown in Figure R.9, the share of low- or no-carbon energy sources grows steadily over the projection period. The use of low-carbon hydrogen as a share of total heavy industrial energy demand increases from less than 1% in 2021 to 6% in 2050 in the Global Net-zero Scenario, and similar in the Canada Net-zero Scenario. Other energy sources, such as electricity, biomass, biofuels, and renewable natural gas, increase their share in both net-zero scenarios. These low- or no-carbon energy sources offset energy from fossil fuels, whose combined share of the heavy industrial sector’s energy use falls from around 60% of energy use in 2021 to 32% in 2050.

Figure R.9: Share of energy type in the industrial sector, excluding the oil and natural gas sector, Global Net-zero Scenario

Description

Description: This line chart shows the share of different energy categories in the projection period in the Global Net-zero Scenario. The categories are electricity, hydrogen, and bioenergy, fossil fuel with CCUS, and other fossil fuels (includes non-energy feedstock).

The share of other fossils fuel has been declining since the early 2010s, and is outpaced by electricity, hydrogen, and bioenergy by the early 2030s. Fossil fuel with CCUS starts increasing in the late 2020s, until it plateaus at slightly over 10% by the early 2040s.

Energy use changes are much slower in the Current Measures Scenario

In the Current Measures Scenario, energy use in the industrial sector undergoes some change, such as efficiency improvements and some limited applications of CCUS. However, the pace of change is much slower than in both net-zero scenarios. This is because of our assumptions about climate policies and technology costs in this scenario give less incentive for industries to change their energy use patterns.

Total industrial energy use increases less than 10% in both net-zero scenarios

We project total energy use in the heavy industry sector to be relatively flat in both net-zero scenarios, increasing less than 10% from 2021 to 2050, compared to nearly 20% in the Current Measures Scenario. New technologies and energy efficiency improvements reduce energy use in the sector.

In the Global Net-zero Scenario, total energy use in the entire industrial sector, including energy use in oil and gas, light industry, and for direct air capture processes, declines by 27% to 2050. Declining energy use for oil and natural gas production drives this trend and is partly offset by the emergence of direct air capture (DAC) facilities later in the projection period, which use large amounts of electricity and natural gas. In the Canada Net-zero Scenario, oil and natural gas production are higher and total industrial energy use is higher than the Global Net-zero Scenario, but still declines by 10% by 2050. In the Current Measures Scenario, total industrial energy use grows steadily, although somewhat slower than over the past two decades.

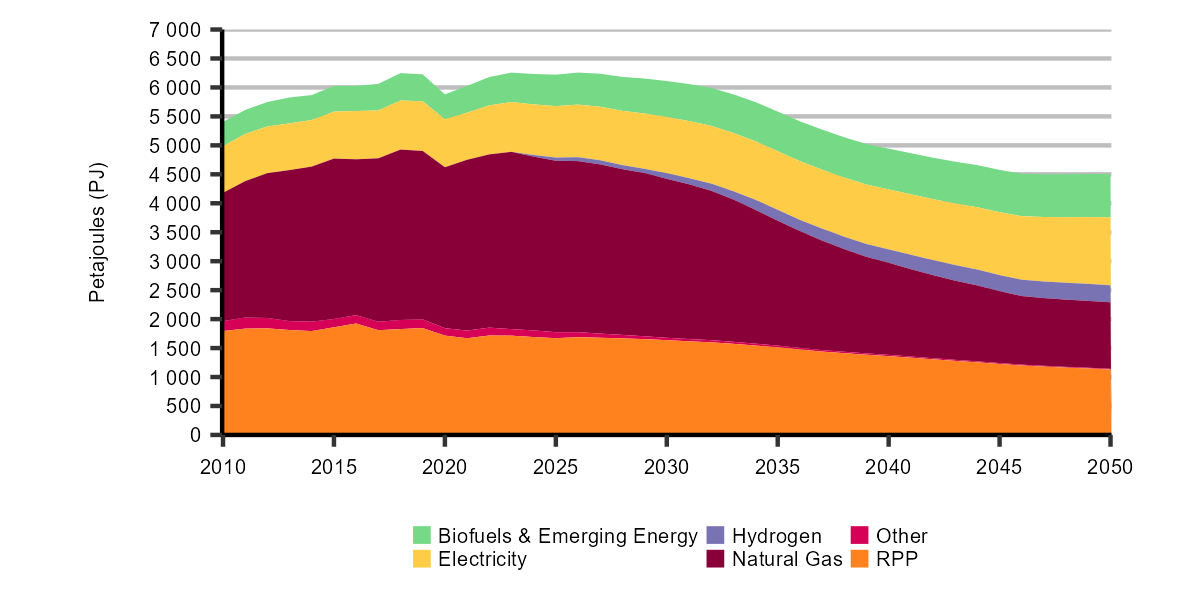

Figure R.10 shows total industrial demand by fuel in the Global Net-zero Scenario. By 2050, the share of electricity, clean fuels such as bioenergy and hydrogen, and fossil fuels with CCUS more than triples from current levels.

Figure R.10: Total industrial energy use by fuel, Global Net-zero Scenario

Description

Description: This stacked area chart shows industrial demand by fuel type in the Global Net-zero Scenario over the projection period. The fuel types are biofuels & emerging energy, hydrogen, other, electricity, natural gas, and RPP.

RPP has gradually been trending downwards since the early 2010s and this continues in the projection period. Similarly, industrial demand for natural gas declines starting in the mid-2020s. Hydrogen, electricity, and biofuels & emerging energy increase in the projection. Overall, industrial energy demand gradually declines until 2050.

Industrial GHG emissions

The key trends we describe in the previous section, technological innovation, CCUS, and fuel switching, result in steadily decreasing GHG emissions from the heavy industry sector in both net-zero scenarios. In both net-zero scenarios, emissions decline by nearly 75% from 2021 levels. This implies that heavy industry GHG emissions are positive in 2050, although Canada still achieves net-zero due to negative emissions occurring in other sectors. Emissions fall by 15% in the Current Measures Scenario.

DAC facilities, which we consider to be a part of the broader industrial sector, result in net-negative emissions by 2050 in both net-zero scenarios. Emissions from the oil and gas sector drop significantly in both net-zero scenarios. We describe our energy use and GHG emission results for both of these sectors later in this chapter.

Transportation

The transportation sector accounted for 21% of Canada’s end-use energy demand in 2021. This demand includes energy used to transport people and goods using a variety of modes, including on-road vehicles, rail, airplanes, and boats. Almost all energy use in this sector is RPPs derived from crude oil. Gasoline, the primary fuel for on-road passenger vehicles, made up 53% of total transportation demand in 2021. In the freight sector, diesel is the most common fuel, making up 32% of total transportation demand in 2021. Aviation fuel, biofuels, and heavy fuel oil made up much of the remaining energy use in 2021. Electricity is a small but growing portion of energy demand in the transportation sector.

The transportation sector’s GHG emissions in 2021 were 150 MT, or nearly a quarter of Canada’s total emissions. Emissions from the sector have declined by 4% since 2005. Transporting passengers accounted for 57% of GHG emissions in the transportation sector, with freight making up 33% and the remaining emissions coming from off-road vehicles.

How does energy demand change over time in the transportation sector?

Discover the data for yourself using our interactive visualization tool. Check out the projected energy mix for end-use demand in the transportation sector.

Passenger transportation

In both our net-zero scenarios, the primary change in the passenger transportation sector is the movement towards electric passenger vehicles and away from internal combustion engine (ICE) vehicles. Emissions from ICE vehicles remaining on the road also decline.

The use of EVs increases substantially in all scenarios

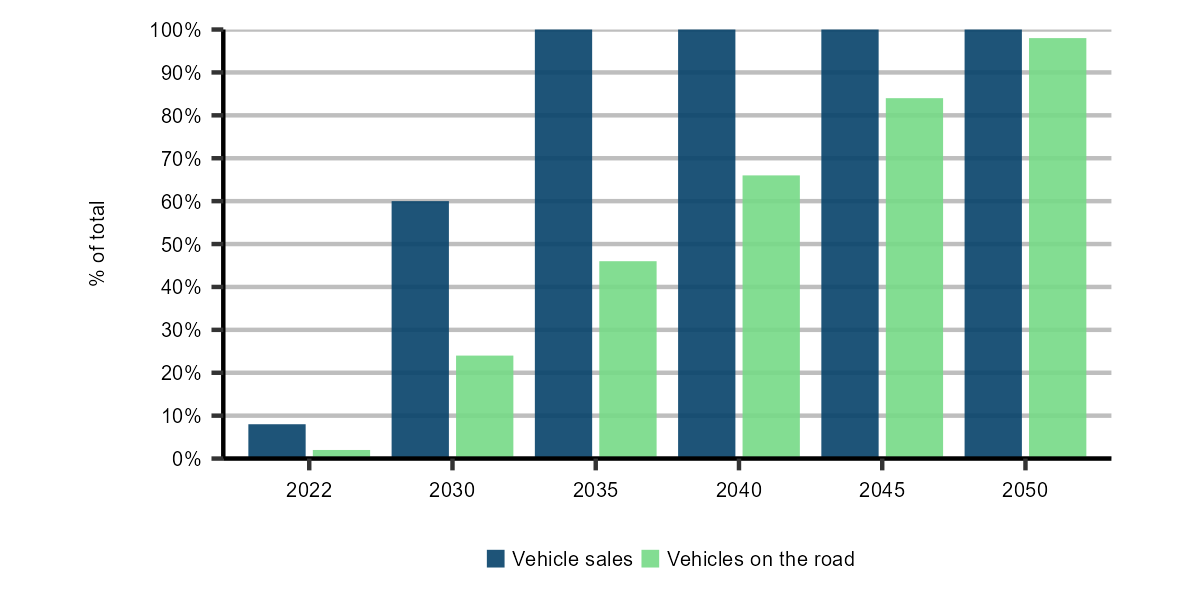

EV sales, including plug-in hybrid-electric vehicles (PHEVs), made up over 8% of all vehicles sales in Canada in 2022, up from 2% in 2018. We project this trend to accelerate in the Global and Canada Net-zero scenarios, with nearly all passenger vehicle sales being EVs by 2035. However, the total stock of vehicles on the road changes more slowly, as vehicles can stay on the road for 15 or more years. Though sales of new ICE vehicles are nearly zero by 2035, there are some older vehicles on the road by 2050 in both net-zero scenarios. In the Current Measures Scenario, EV sales grow at a slower rate than in the net-zero scenarios but still become a competitive choice for consumers, making up 50% of all vehicle sales by 2035, and 75% in 2050. Figure R.11 shows the share of EV sales and passenger vehicles on the road that are EVs in the Global Net-zero Scenario.

Figure R.11: EVs as a share of total vehicle sales and vehicles on the road, Global Net-zero Scenario

Description

Description: This column chart shows the share of EV sales and vehicles on the road over the projection period in the Global Net-zero Scenario.

From less than 10% of total vehicle sales in 2022, EVs make up 60% of all vehicle sales in 2030 and 100% by 2035. The share of vehicles on the road that are EVs follows to reach nearly 50% in 2035, over 80% in 2045, and nearly 100% by 2050.

The electrification of the passenger vehicle fleet is driven by the policies we assume in the net-zero scenarios. The federal mandatory zero-emission vehicle sales targets and similar policies in British Columbia (BC) and Quebec, federal and provincial EV incentives, and increasing carbon pricing all increase the availability and cost-effectiveness of EVs compared to ICE vehicles. In addition, we assume the costs of batteries, which are major component of the cost of EVs, decline over the projection period.

Emissions from the remaining ICE vehicles decrease significantly

While EVs gain an increasing market share over the projection period, emissions from ICE vehicles also decline in all three scenarios. Policies, including Canada’s light-duty vehicle GHG emissions standards and Clean Fuel Regulations, result in lower overall emissions per kilometre travelled by ICE vehicles. This includes greater blending of biofuels into the liquid fuel supply and better fuel efficiency of new ICE vehicles. Combined with wide-scale adoption of EVs, the emissions per kilometre travelled by passenger vehicles fall by around 95% in both the Global and Canada Net-zero scenarios from 2021 to 2050. In addition to the switch to EVs, public transportation continues to play a key role in moving people. Transit is increasingly powered by electricity and bioenergy in the net-zero scenarios.

Air travel emissions reduce due to aircraft efficiency improvements and use of clean fuels

In all three scenarios, demand for aviation fuel recovers to pre-pandemic levels by 2023. In the Global Net-zero Scenario, we project energy use for passenger aviation remains relatively stable after 2023 as newer, more efficient aircraft help to improve fuel efficiency of air travel, and the trends are similar in the Canada Net-zero Scenario. In the net-zero scenarios the main source of GHG emissions reductions in the sector are through increased use of biofuels and hydrogen-based fuels.

Passenger transportation energy use declines across all scenarios

Led by large-scale adoption of EVs, we project total energy use in the passenger transportation sector to decline by 43% from 2021 to 2050 in the Global Net-zero Scenario and similar levels in the Canada Net-zero Scenario. This drop in energy use is largely due to EVs being far more energy-efficient compared to ICE vehicles.Footnote 13 By 2050, electricity makes up nearly 50% of the energy use in the passenger transportation sector in both net-zero scenarios, up from below 1% in 2021. Low-carbon aviation fuel, conventional jet fuel, gasoline, and ethanol make up much of the remaining fuel mix in 2050. In the Current Measures Scenario, passenger transportation energy use declines slowly after rebounding to pre-pandemic levels in 2023. Increasing number of EVs and improving efficiency of ICE vehicles are reasons for this decline.

Freight transportation

In both net-zero scenarios, we project a few key shifts in the energy use and technologies used to transport goods. Electric trucks and vans increase significantly in some segments of the freight sector but in the heavy freight sector we project that other options are viable, including increasing use of hydrogen fuel cell technology. Biofuels also become an economically attractive fuel in the net-zero scenarios, providing a low-carbon fuel that can be used in existing diesel engines, or blended with fossil fuel-derived diesel to reduce the emission intensity of that fuel.

Light-duty freight vehicles are typically used to move smaller loads over relatively short distances. In both net-zero scenarios, electric trucks and vans gradually become the most economic choice of vehicle to serve this purpose. Nearly all light-duty freight vehicle sales are electric by 2040 in both net-zero scenarios.

Hydrogen-based vehicle use grows significantly in the heavy freight sector in the net-zero scenarios

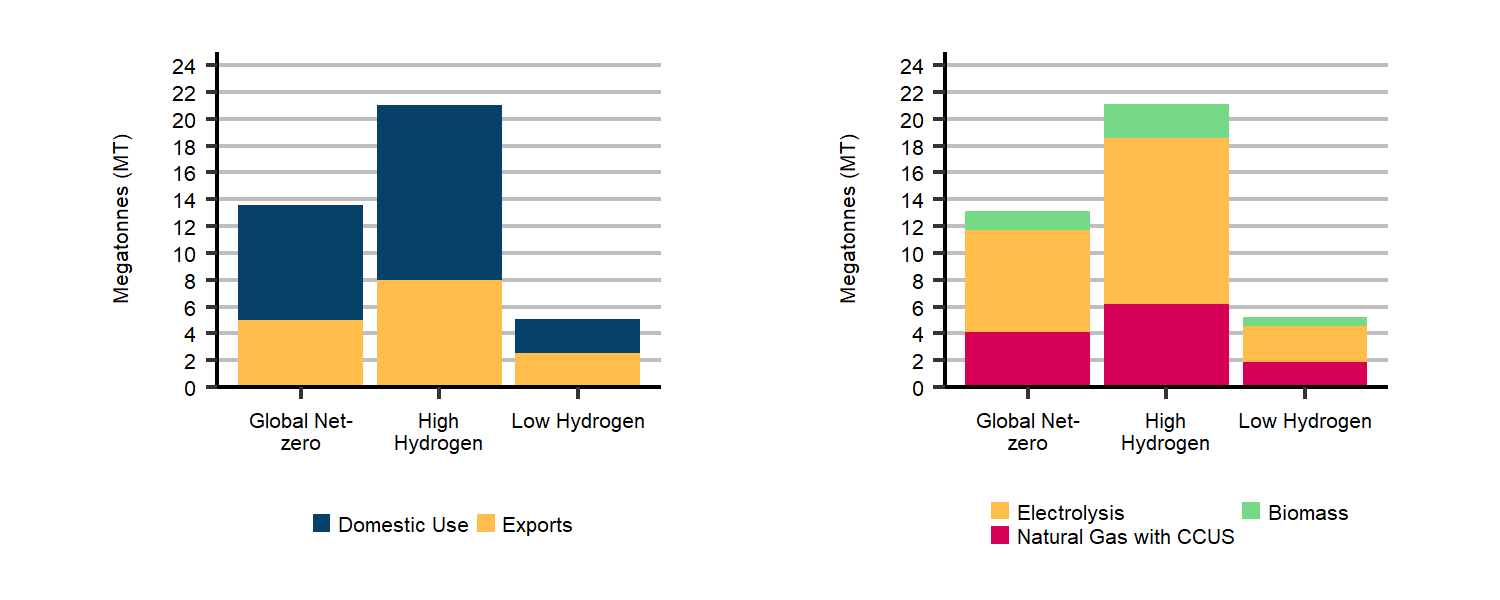

For heavier freight, electric-powered vehicles take a share of the market in our net-zero scenarios, as do other technologies. A robust hydrogen supply develops in both net-zero scenarios, in part due the demand for hydrogen to use in trucks, rail locomotives, and marine vessels equipped with fuel cell technology. Fuel cells convert hydrogen to electricity, which then drives electric motors. Compared to batteries, compressed hydrogen paired with fuel cells is more energy-dense, which is beneficial when moving heavy goods over long distances. The use of hydrogen in the freight sector grows from nearly 0.5 MT in 2030 to almost 5 MT in 2050 in the Global Net-zero Scenario, with slightly more in the Canada Net-zero Scenario. Electricity demand for freight transportation reaches over 90 terawatt-hours (TWh) by 2050 in the Global Net-zero Scenario. Given the relatively high efficiency of EVs, this represents a large portion of freight activity. Unlike the passenger sector, where electrification of personal vehicles has significant momentum, the relative mix of technologies in the freight sector is more uncertain. Depending how technologies and markets evolve, we may see more or less hydrogen, electricity, or other clean fuels in the future. We explore this uncertainty further in the “What if” case for hydrogen supply and demand, located in the hydrogen results section.

Renewable diesel use grows to 35% of the diesel fuel supply by 2050 in the Global Net-zero Scenario

We also project steady growth of biofuel use in the freight sector. The most common biofuels used today are ethanol and biodiesel. These biofuels are often blended into petroleum-based fuels for use in ICE vehicles. However, the rate at which these fuels can be blended into the petroleum-based fuel stream is limited, usually anywhere from 5 to 20% depending on the characteristics of the engine. In the Global and Canada Net-zero scenarios, renewable diesel, often referred to as hydrogenation-derivedDefinition* renewable diesel, emerges as the leading biofuel over the projection period. Renewable diesel is chemically equivalent to diesel derived from fossil fuels. This means it is a “drop-in” biofuel and can be used as a direct replacement for petroleum-based diesel or blended at a much higher ratio than biodiesel. Renewable diesel can be derived from many different processes, allowing a diverse set of biomass feedstocks to be used. By 2030, in the Global Net-zero Scenario, we project renewable diesel’s share of the diesel fuel supply to reach 7%, then grow to 35% by 2050.

In the Current Measures Scenario, the freight sector gradually becomes more efficient, with improvements mostly focused on engine efficiency and aerodynamics. We also project much lower uptake of electric and hydrogen fuel cell vehicles, and less use of biofuels.

Freight energy use decreases in the net-zero scenarios, and increases in the Current Measures Scenario

Total energy use in the freight transportation sector increases in the near term as shipping volumes recover to pre-pandemic levels. In the longer term, demand trends downward in both net-zero scenarios. This decrease is primarily due to growth of electric and hydrogen fuel cell freight vehicles, both of which are more energy efficient compared to ICE vehicles. This effect is partially offset by steadily growing demand for freight transportation services. In the Current Measures Scenario, energy use in the freight sector increases by 25% over the projection period.

Figure R.12 shows end-use demand by fuel in the transportation sector, including passenger, freight and off-road energy use in the Global Net-zero Scenario, and total end-use demand in the other two scenarios.

Figure R.12: Transportation sector end-use demand by fuel, Global Net-zero Scenario

Description

Description: This stacked area chart shows end-use demand by fuel from the transportation sector in the Global Net-zero Scenario. The fuels are electricity, hydrogen, bioenergy, and fossil fuels. The stacked area is compared with lines representing total transportation demand in the Canada Net-zero and Current Measures scenarios.

Fuel demand reaches a peak in the early- to mid-2020s in both net-zero scenarios, followed by a gradual decline. In these scenarios, demand for motor gasoline and diesel declines sharply, and gradually gets replaced by electricity, hydrogen, and bioenergy. Demand remains mostly flat in the Current Measures scenario in the projection period.

Transportation GHG emissions

Emissions from the transportation sector decline steeply in both net-zero scenarios while staying relatively flat in the Current Measures Scenario. We project that GHG emissions in the Global Net-zero Scenario fall by 90% from 2021 to 2050, and to a similar level in the Canada Net-zero Scenario. In both net-zero scenarios, these reductions are driven by our assumptions about policies like the federal mandatory zero-emission vehicle sales targets and steadily increasing economy-wide carbon pricing. Declining costs of certain technologies such as batteries in EVs and hydrogen vehicles also factor into our projections. While Canada achieves net-zero by 2050 in our net-zero scenarios, some emissions from the transportation sector remain in 2050, mainly in the aviation and freight sectors. In the Current Measures Scenario, emissions fall steadily after 2025, with continued emission reductions in the passenger sector offsetting growing emissions in the freight sector.

Primary energy demand

In this analysis, primary demand is the total amount of energy used in Canada. Primary demand is calculated by adding the energy used to generate electricityFootnote 14 and hydrogen to total end-use demand, and then subtracting the end-use demand for electricity and hydrogen. Primary demand is higher than end-use demand due to factors such as heat loss in thermal electric generation, and the energy required for the hydrogen production process.

In both net-zero scenarios, total primary demand falls, largely a result of declining fossil fuel use

Coal use continues its current declining trend, largely due to the phase out of coal-fired power generation. Demand for RPPs falls, largely due to much greater use of electricity in the transportation sector. One source of crude oil demand that is relatively stable over the projection period is for non-energy products such as asphalt, lubricants, and petrochemical feedstocks.

Natural gas demand declines in both net-zero scenarios, and increases in the Current Measures scenario

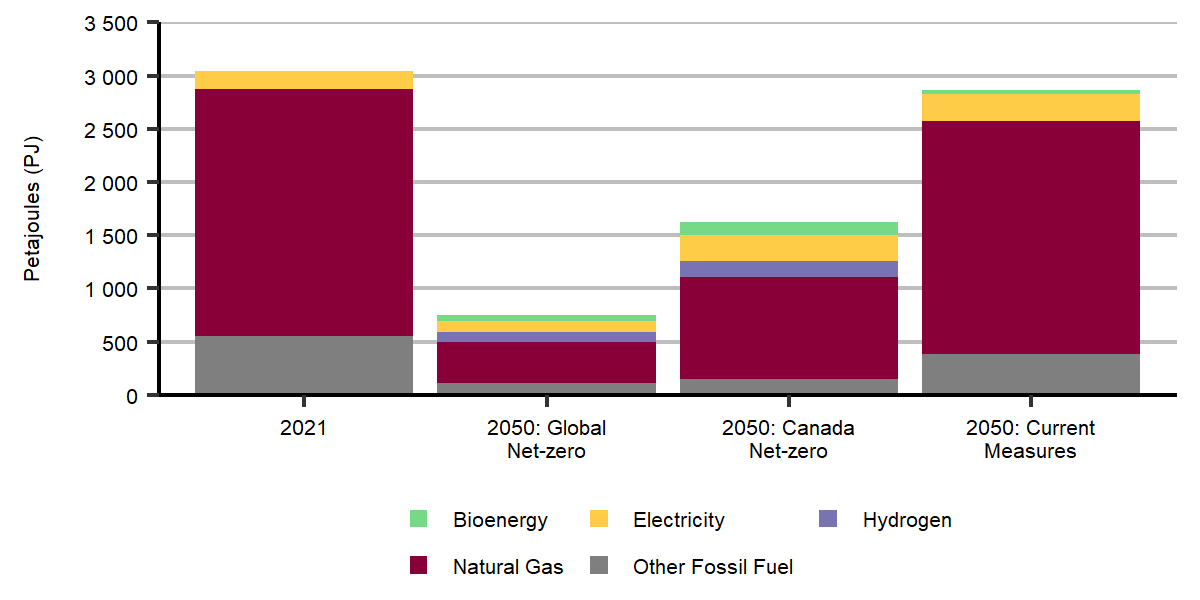

Natural gas demand falls due to electrification of home heating, less natural gas use in the upstream oil and natural gas sectors, and efficiency improvements in the residential and industrial sectors. The decrease in natural gas demand is less than for coal and RPPs, as we project that natural gas becomes increasingly used in the power generation sector when coupled with CCUS, and as a feedstock for hydrogen production. In the Current Measures Scenario, primary energy demand is relatively flat until 2040, before increasing in the last decade of the projection period. Figure R.13 shows primary demand by fuel for all three scenarios.

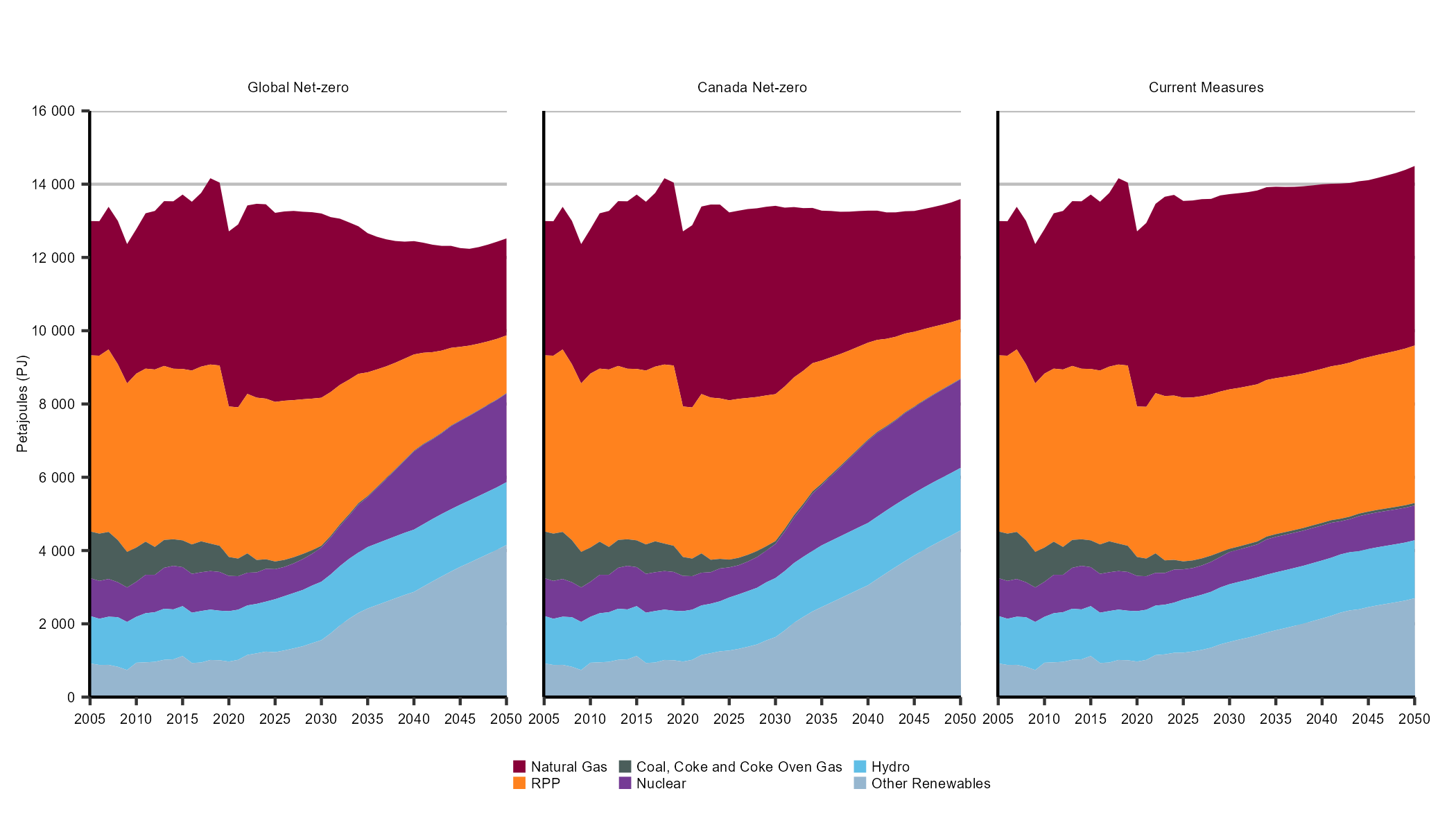

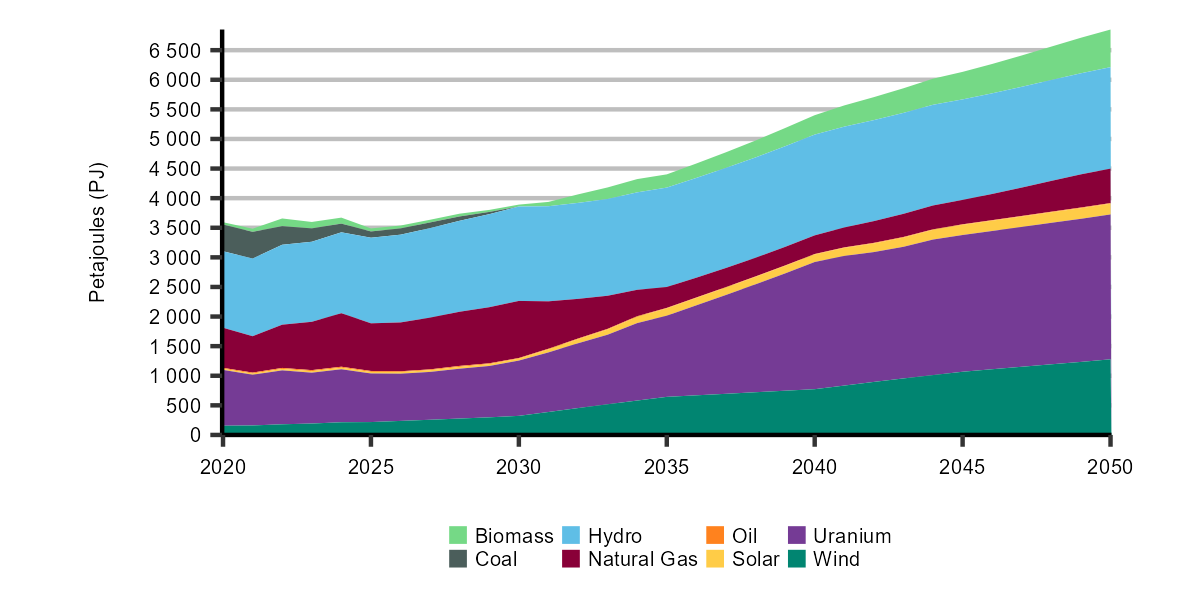

Figure R.13: Primary energy demand by fuel, all scenarios

Description

Description: These three charts show primary energy demand by fuel over time in the Global Net-zero, Canada Net-zero, and Current Measures scenarios. The fuels are natural gas, coal, coke and coke oven gas, hydro, RPP, nuclear, and other renewables.

All scenarios see a significant growth in other renewables, especially the net-zero scenarios. These scenarios also see a pronounced increase in nuclear starting in the 2030s and a gradual decline in natural gas and RPP starting in the mid-to-late 2020s.

Key uncertainties: energy demand

Energy use drivers: The need for energy in each sector is driven by our projections of activity in that sector, like economic output of various industries or population growth. Different outcomes for any of the energy use drivers could impact the long-term energy outlook.

Technology: We make assumptions about the costs of various energy technologies in the future. Costs that are different than we assume will change the decision-making of energy users and the energy use projections in our scenarios. We explore some of these uncertainties in the “What if” cases throughout this report.

Behavioural change: Energy users’ decision-making changes as societal preferences change over time. For example, preferences could evolve towards more or less dense cities, more remote work, or bigger or smaller homes, all of which can influence energy use projections.

Electricity

Canada’s electricity system is currently among the lowest emitting in the world, with 81% of the sector’s generation coming from low- or non-emitting sources. This is largely due to Canada’s hydroelectric generation resources, which supplied over 61% of Canada’s electricity in 2021. Nuclear generation and, increasingly, wind and solar, also contribute to Canada’s high proportion of non-emitting power generation.

To develop the electricity production projections in EF2023, we rely on a model that simulates the operations and the investment decisions of the electricity sector, while also ensuring reliability of the system. The model builds new generation, storage and transmission infrastructure based on minimizing the total system costs throughout the projection period. We also incorporate our assumptions about policies and the costs and operational characteristics of various generation technologies. Factors beyond these can impact the development of a wide array of energy projects, including electricity projects. Examples include concerns about air quality, safety, noise, competing land-uses, or visual impacts. Societal preferences and how they may evolve in the future, are largely beyond the scope of our analysis but have potential to impact the projections for any of the electricity generation technologies we describe in this section.

Canada’s electricity system is regionally diverse

The generation mix in each province and territory is largely determined by the resources it has available. Quebec, Manitoba, Newfoundland and Labrador, Yukon, and BC have significant amounts of hydro generation, whereas Alberta, Saskatchewan, and remote and northern communities rely more on fossil fuel generation. Ontario and New Brunswick both have diverse electricity mixes, including nuclear. This regional diversity means that the emission reduction pathways in our net-zero scenarios are unique to each region’s specific circumstances.

The electricity sector has exhibited the greatest reduction in emissions among Canada’s major sectors, cutting emissions by more than half from 2005 to 2021. Many provinces reduced emissions from this sector during that time, with the biggest reductions from Ontario and Alberta. Ontario phased out coal-fired generation by 2015 and Alberta is likely to do so by the end of 2023. In total, the electricity sector accounted for 8% of Canada’s emissions in 2021.

Electricity use increases while emissions decrease in the net-zero scenarios

In the Global and Canada Net-zero scenarios, electricity becomes the cornerstone of Canada’s energy system. In both scenarios we project the amount of electricity generated and consumed in Canada in 2050 more than doubles from current levels. While the need for electricity grows, we project the electricity system also reduces emissions to net-zero by 2035 in both scenarios. This reduction in emissions is led by growth in wind, nuclear, hydroelectric, and natural gas-fired generation with CCUS, and the phase out of coal-fired electricity generation. After 2035, GHG emissions from the electricity sector become net-negative, meaning the sector removes more emissions than it emits through deployment of bioenergy coupled with CCUS technology (BECCS)Definition*.

Key trends: electricity

Electricity use more than doubles over the projection period in both net-zero scenarios.

We project the most growth in wind generation in all scenarios, including the Current Measures Scenario, despite less ambitious climate policies and more modest technology cost improvements.

The electricity system decarbonizes and becomes net-negative by 2035 with the deployment of BECCS generation facilities.

What energy sources does your region use to generate electricity?

Discover the data for yourself using our interactive visualization tool. Check out the projected energy sources for electricity generation.

Electricity use

As described in the “Energy demand” section of this chapter, we project that electricity demand grows significantly in all end-use sectors in both net-zero scenarios. This growth is driven by wide-scale adoption of EVs and heat pumps, and electrification of some industrial activities. In addition, as we describe in more detail in the “Hydrogen” section of this chapter, hydrogen production becomes a significant source of new electricity demand in the future. Finally, we project construction of direct air capture (DAC) facilities, which become another new source of electricity demand later in the projection period. We describe the role of DAC in the “Negative emissions” section later in this chapter.

Figure R.14 shows electricity demand by sector in the Global Net-zero Scenario. Overall, we project electricity demand to grow 120% from 2021 to 2050 in the Global Net-zero Scenario, and 135% in the Canada Net-zero Scenario. In both scenarios, the annual rate of demand growth is almost triple that of the 1995 to 2019 period. In the Current Measures Scenario, electricity demand grows more slowly than in the net-zero scenarios, increasing by 62% over the projection period.

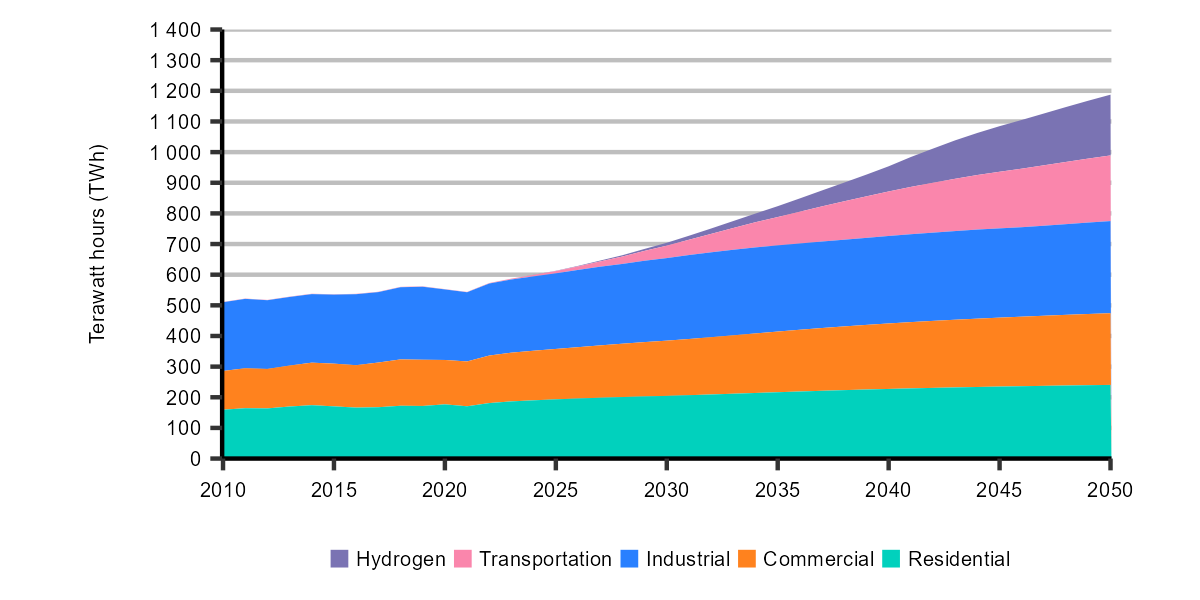

Figure R.14: Electricity use by sector, Global Net-zero Scenario

Description

Description: This stacked area chart shows projected electricity demand in the Global Net-zero Scenario in the residential, commercial, industrial, transportation, and hydrogen sectors.

Electricity demand grows steadily in the residential, commercial, and industrial sectors. Transportation and hydrogen production, which are near zero in 2021 become major drivers of growth in the projection.

Our electricity projections are also influenced by changes in day-to-day and seasonal electricity use patterns. As new uses of electricity emerge, the annual peak in electricity demand in a system will likely change. This change will influence how electricity systems evolve as utilities and system operators need to reliably meet the annual peak in electricity demand, which might occur for only an hour or two in a year.

In both net-zero scenarios, the annual hourly peak of electricity demand grows in all regions

This increase is because of growing electricity use overall, but also growing use of devices that increase electricity use more during a certain period during the day or in a particular season. For example, EVs typically draw relatively large amounts of electricity over a short period when owners plug them in. Similarly, greater use of heat pumps means that overall electricity demand is more sensitive to weather than it is now.

What if electricity vehicle charging patterns result in higher peak electricity demand?

Sales of EVs in Canada have quickly increased in recent years, reaching over 8% of total vehicle sales in 2022. While ICE vehicles rely on RPPs like gasoline and diesel as their source of energy, EVs are powered by electricity stored in large batteries, which drive electric motors, propelling the vehicle. EV batteries are charged using the same electricity grid we use to power other aspects of our daily lives.

EVs need more electricity than most other household devices

Most currently available EVs consume about 3,000 to 6,000 kilowatt-hours (kWh) in a year based on 20,000 km of driving. A new refrigerator uses about 500 kWh per year. Currently, most EV charging occurs through a charger installed in a garage or at a dedicated public charging station. Most EV charging occurs at a fairly high rate of power transfer in order to charge batteries quickly. Most home chargers can charge a depleted battery in 4 to 12 hours. Many public EV charging stations are much quicker than home chargers.

EV owners tend to plug their vehicles into chargers when they arrive home. For many drivers, this is often in the late afternoon when they return from work. Residential electricity demand is often already high during these hours, including higher use of stoves and electronics. It is also often the hottest part of the day in the summer, meaning more air conditioning units may be running. If charging patterns are not managed as the share of EVs grows, EV charging could contribute to much higher electricity use during peak times. The level of peak electricity demand throughout the day and over the year affects how electricity systems develop. Utilities and system operators need to continually meet the electricity needs of users, but also have sufficient capacity to meet annual peak electricity demand, which might be for only a few hours in a year.

How EV charging patterns affect peak electricity demand largely depends on how much utilities and grid operators can more evenly spread charging out across the hours of the day. Charging patterns can be influenced through market mechanisms, such as offering consumers lower electricity prices during certain hours of the day when demand is lower. Most home chargers can be controlled by consumers or grid operators to delay charging to lower demand hours.

“What if” EV charging during peak hours is not managed?

In the Global Net-zero Scenario, we assume that a combination of price signals, technologies, and behavioural changes result in charging that is more evenly spread across the hours of the day. In this “What if” analysis, we explore how uncoordinated EV charging might impact the electricity system and ultimately the total amount of electricity generating capacity required. This analysis, the Uncoordinated Charging Case, models an outcome where more drivers charge their EVs during peak hours.

Peak electricity demand in each province and territory increases throughout the projection period in the Global Net-zero Scenario as total electricity demand increases and electricity use patterns change. For example, peak electricity demand in Ontario was 22.2 gigawatts (GW) in 2021. In the Global Net-zero Scenario, peak demand is 177% higher by 2050, reaching 61 GW. This increase in peak demand is similar in magnitude in many other provinces and territories.

However, while total electricity use is identical in both cases, peak demands by 2050 in most provinces and territories in the Uncoordinated Charging Case are between 1 and 5% higher than in the Global Net-zero Scenario. Despite this higher peak in demand, the overall impact on system-wide needs for new capacity is relatively small, as we project some changes to the generation mix compared to the Global Net-zero Scenario, as well as changes to the operations of the electricity system.

Energy systems become more flexible, potentially accounting for uncoordinated charging

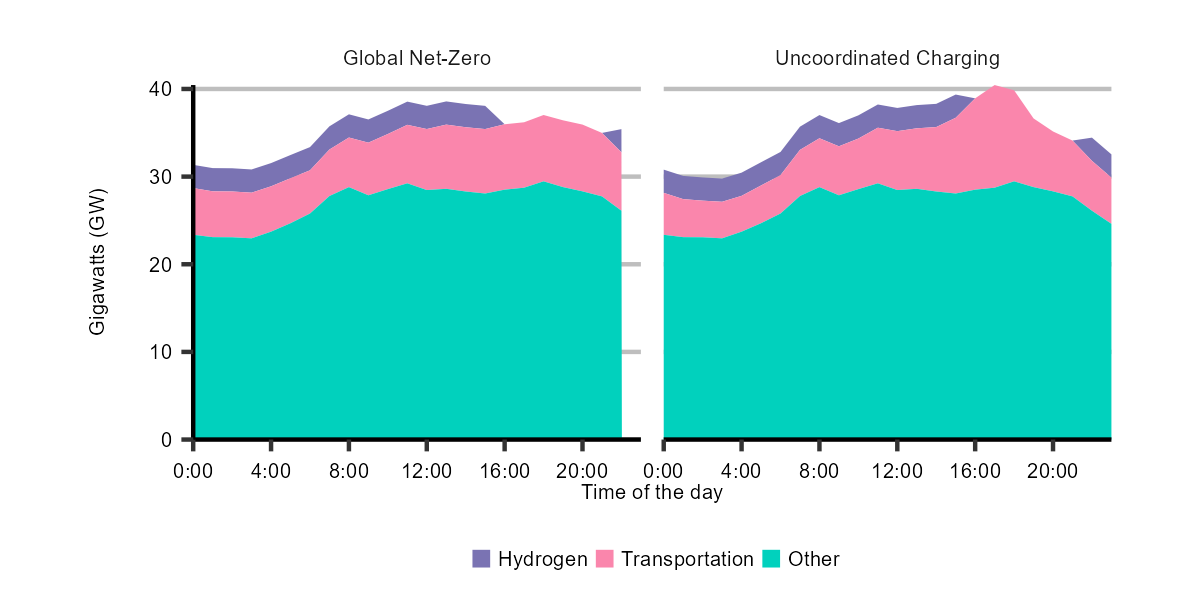

Figure R.15 shows an example winter day in 2050, showing hourly electricity demand in BC with coordinated and uncoordinated EV charging. The emergence of hydrogen as a new source of electricity demand requires building more electricity generation capacity. However, hydrogen production is a flexible source of electricity demand. During periods of high demand, hydrogen production using electricity can be reduced to accommodate the needs of the electricity system. That flexibility allows the electricity systems in several regions to accommodate the higher peak demand in the Uncoordinated Charging Case without significant additional investment in generating capacity.

We project that many provinces utilize this flexibility in both the Global Net-zero Scenario and Uncoordinated Charging Case to offset peak periods of demand. Without this demand flexibility, the difference in peak demand in the two scenarios would have been higher, requiring more investment in new generation in the Uncoordinated Charging Case.

Figure R.15: Example daily hourly electricity demand in British Columbia by use, winter of 2050, Global Net-zero Scenario and Uncoordinated Charging Case

Description

Description: These stacked area charts show a hypothetical example of what hourly electricity demand could look like in British Columbia in the winter of 2050. The charts are broken down by demand from the hydrogen, transportation, and other sectors. The first chart is from the Global Net-zero Scenario. The second chart shows demand with uncoordinated charging.

Demand from the transportation sector sees a significant peak starting at 16:00 in the Uncoordinated Charging chart and remains more stable during the day in the Global Net-zero Scenario. Demand for hydrogen drops to zero in both scenarios during the peak demand times of around 16:00 to 20:00.

Wind generation increases while solar decreases in the Uncoordinated Charging Case

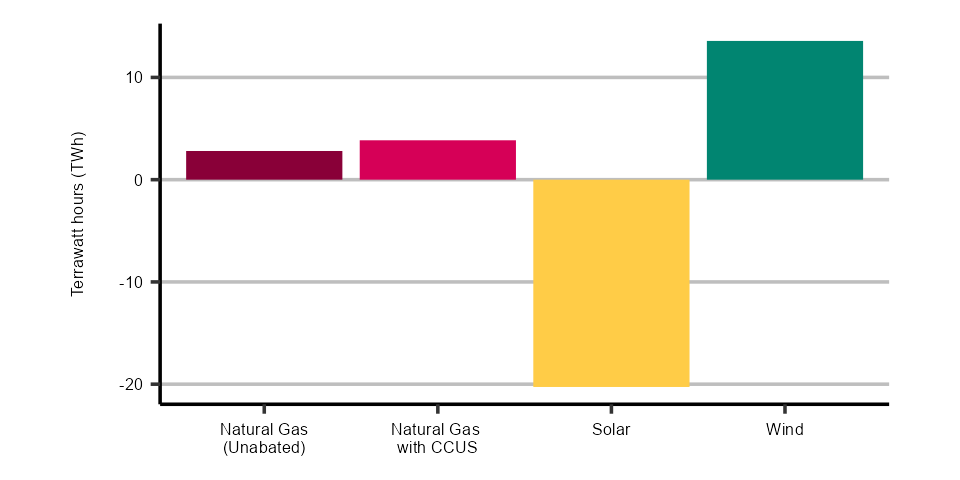

As shown in Figure R.16, compared to the Global Net-zero Scenario, we project more wind and less solar generation in the Uncoordinated Charging Case. In this case, electricity use is higher during the early evening and lower during the day. Because solar generates more during the day than in the evening, solar generation is less valuable in the Uncoordinated Charging Case relative to the Global Net-zero Scenario and less solar generation is built. Conversely, wind tends to blow more during the evening period, so becomes a more valuable asset to the electricity system in the Uncoordinated Charging Case. By 2050, wind generation is 4% higher in the Uncoordinated Charging Case compared to the Global Net-zero Scenario, while solar generation is 32% lower.

Natural gas without CCUS is used more often in the Uncoordinated Charging Case

Finally, in some provinces, we project higher generation from natural gas with and without CCUS. To accommodate the highest peaks in generation throughout the year, some provinces have natural gas-generating facilities without CCUS that are utilized very rarely in the Global Net-zero Scenario. In the Uncoordinated Charging Case these assets are utilized more often in order to meet higher and more frequent peaks in electricity demand. As a result of more frequent natural gas use, there are slightly higher GHG emissions from the electricity sector in the Uncoordinated Charging Case.

Figure R.16: Difference in generation between the Global Net-zero Scenario and the Uncoordinated Charging Case in 2050, by select fuel

Description

Description: This column chart shows the difference in electricity generation between the Global Net-zero Scenario and the Uncoordinated Charging Case in 2050.

In the second scenario, solar generation decreases by around 20 TWh and is compensated by an increase in generation from wind, natural gas with CCUS, and natural gas (unabated).

Greater use of EVs, along with greater electricity use across the energy system, would likely require investments in local distribution system infrastructure to ensure sufficient capacity to deliver electricity during high demand periods. This need for additional infrastructure could be increased by uncoordinated EV charging, but this is beyond the scope of this analysis. The analysis in EF2023, and in this “What if,” focuses on the bulk power system and does not model local electricity distribution systems.

Electricity production

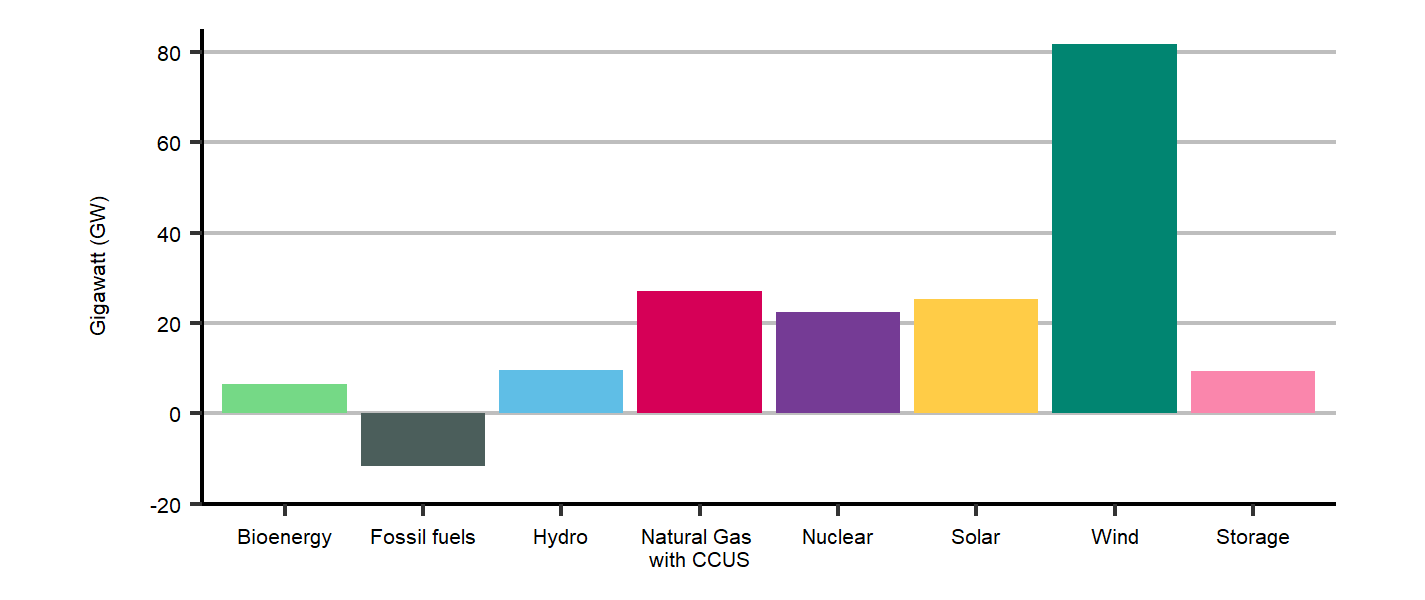

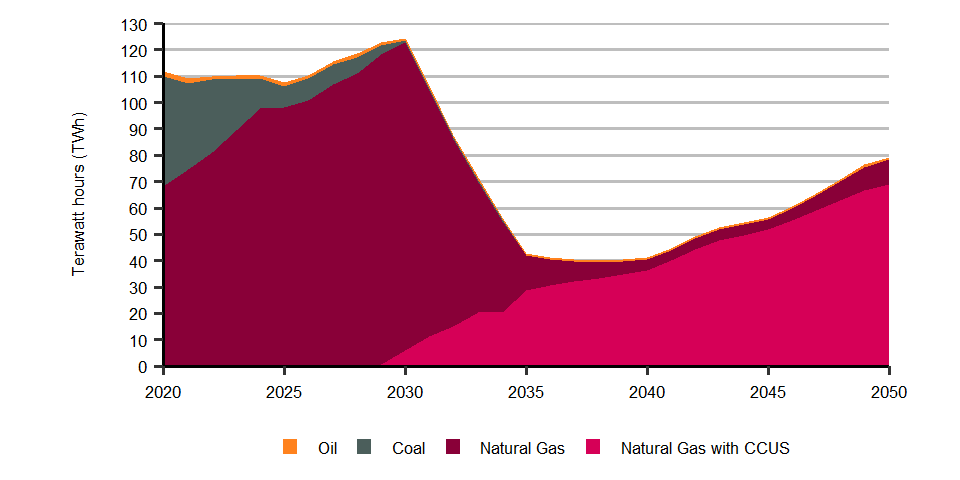

To meet rapidly growing electricity demand while also decarbonizing electricity production, we project significant changes to Canada’s electricity system in both net-zero scenarios. Our assumptions about policies like carbon pricing and the proposed Clean Electricity Regulations mean that almost all electricity-generating facilities built over the projection period are low- or non-emitting, or even net-negative in terms of GHG emissions. Given the diversity of Canada’s electricity system today, there is considerable variety in how each region’s electricity system evolves in our net-zero scenarios. Technologies deployed include wind, solar, hydro, nuclear, fossil fuel with CCUS, and BECCS. Meanwhile, power generation from coal and natural gas not equipped with CCUS drops quickly over the first decade of the projection and is near zero after 2035. Figure R.17 shows the difference in capacity, by fuel, from 2021 to 2050 in the Global Net-zero Scenario.

Figure R.17: Change in electricity capacity from 2021 to 2050, by fuel, Global Net-zero Scenario

Description

Description: This column chart shows the change in electricity capacity in the Global Net-zero Scenario compared to 2021 levels by source. The sources are bioenergy, fossil fuels, hydro, natural gas with CCUS, nuclear, solar, and wind.

Wind sees the most significant increase in capacity, at nearly 80 GW. It is followed by natural gas with CCUS, solar, nuclear, hydro, and bioenergy. Fossil fuels see a decline in electricity generation capacity.

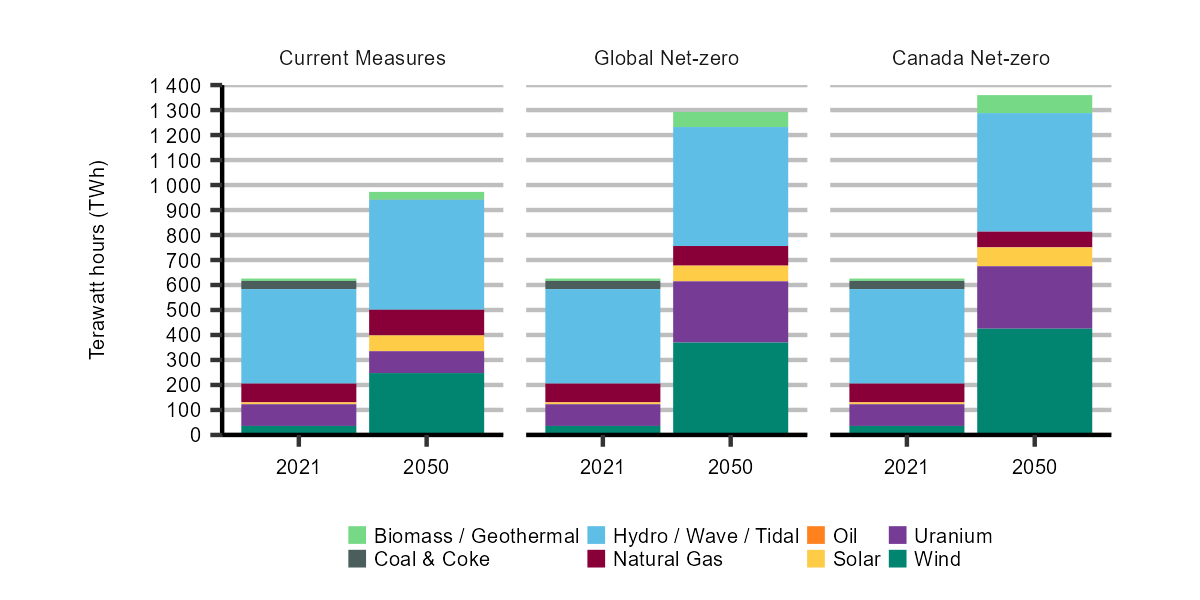

We project that electricity production grows more slowly in the Current Measures Scenario when compared to the net-zero scenarios. There are also fewer policies aimed at reducing the sector’s GHG emissions. Still, while not as dramatic as in the net-zero scenarios, in-place policies, along with our assumptions of modest technology cost improvements, result in strong growth in low-emitting generation sources. Figure R.18 shows electricity generation by fuel in each scenario.

Figure R.18: Electricity generation by fuel, all scenarios

Description

Description: This stacked column chart shows electricity generation by fuel in 2021 and in 2050 in all three scenarios. The fuel types are biomass / geothermal, hydro, oil, uranium, coal and coke, natural gas, solar, and wind.

Wind sees the most significant growth in all scenarios. Uranium sees a significant growth in the net-zero scenarios.

Wind and solar

In all three of the scenarios in EF2023, we project substantial growth of wind generation and steady growth of solar. Our modeling suggests that the low capital and operating costs of both resources make them among the most attractive options for utilities and power producers to increase electricity generation to meet growing demand while also reducing GHG emissions.

Onshore wind generation increases significantly in all scenarios

Electricity generation from onshore wind increases the most among all generation technologies considered in our analysis. We project that wind generation grows ninefold in both the Global and Canada Net-zero scenarios, making up over a quarter of all electricity produced in Canada by 2050. In the Current Measures Scenario, wind generation does not grow as quickly as in the net-zero scenarios, but still increases substantially from current levels, and seven times higher by 2050.

Onshore wind generation grows the most in Alberta, Saskatchewan, and Ontario. This is in part due to strong wind resources in these provinces. In addition, wind generation often matches periods of high electricity demand in these regions, making the energy it generates particularly valuable. For example, in Alberta, it is often windier during the winter, coinciding with periods when demand from electric heat pumps is also high.

Offshore wind grows in both net-zero scenarios

This technology currently not deployed in Canada, but increasingly used in Europe and Asia. Grid-connected offshore generation reaches 23 TWh by 2050. All of that generation comes from offshore wind facilitiesFootnote 15 built off the coast of Nova Scotia. As we discuss in the hydrogen section, additional offshore wind capacity is built off the coast of Nova Scotia and Newfoundland & Labrador and is directly connected to hydrogen electrolysis facilities aiming to export hydrogen to international markets.

Solar generation grows steadily in all three scenarios

Like wind, solar generation becomes one of the most economic choices for utilities and power producers in most regions. In the Global Net-zero Scenario, utility-scaleDefinition* solar generation becomes an important aspect of the electricity system in many provinces, with total Canadian generation growing from 2.5 TWh of generation in 2021 to 50 TWh in 2050. By 2050, solar generation makes up around 5% of total electricity generation in both the Global and Canada Net-zero scenarios. In the Current Measures Scenario, solar generation grows at a similar rate as in the net-zero scenarios.

We also project steady growth of distributedDefinition* solar generation installed primarily on rooftops of residential and commercial buildings. The growth is driven by declining costs and supporting policies such as net-zero building policies and voluntary actions by companies to reduce their environmental footprint. Total installed rooftop capacity reaches 8.2 GW by 2050, meeting 2.5% of residential and commercial electricity demand in the Global Net-zero Scenario. Figure R.19 shows generation from wind and solar in the Global Net-zero Scenario.

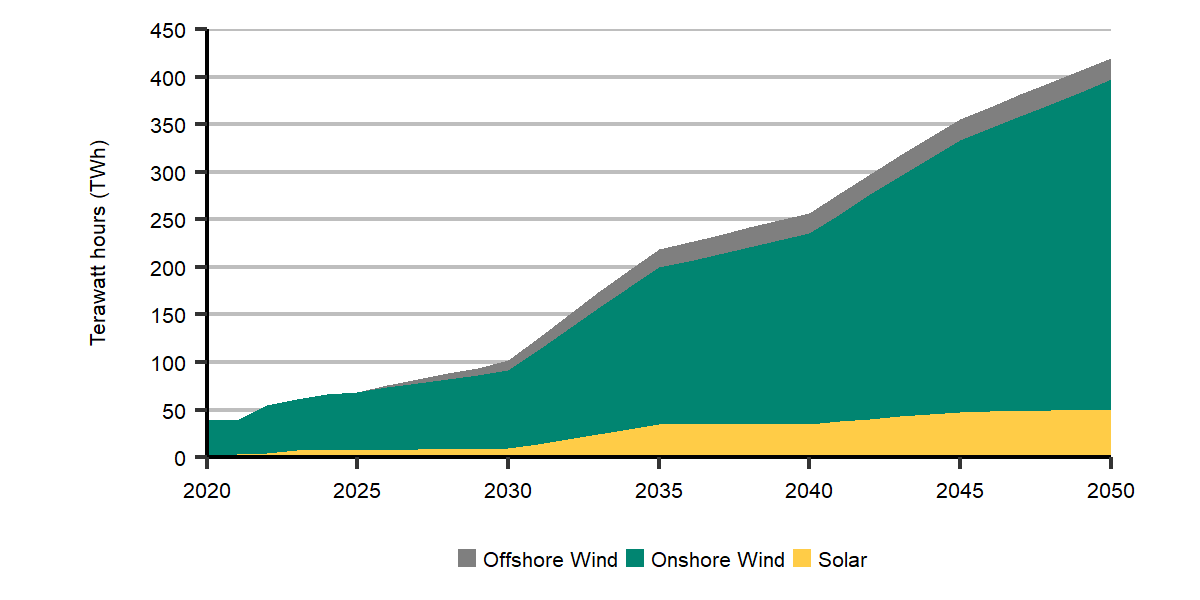

Figure R.19: Generation from onshore wind, offshore wind, and solar, Global Net-zero Scenario

Description

Description: This stacked area chart shows generation from onshore wind, offshore wind, and solar over time in the Global Net-zero Scenario.

Generation from offshore wind becomes noticeable starting in the late 2020s. Onshore wind sees a significant growth starting in the 2020s that continues until the end of the projection period. Solar starts seeing significant growth in the early 2030s.

Matching electricity supply and demand

Compared to most power generation technologies, wind and solar are unique in that their power output is tied to weather patterns, specifically wind speeds and sunlight. Other generating technologies, like hydroelectric or fossil fuel-based generation, can usually adjust their output, although different resources can adjust more quickly and cost effectively than others. This adjustment is important, because electricity systems must constantly balance electricity production and consumption in real time.

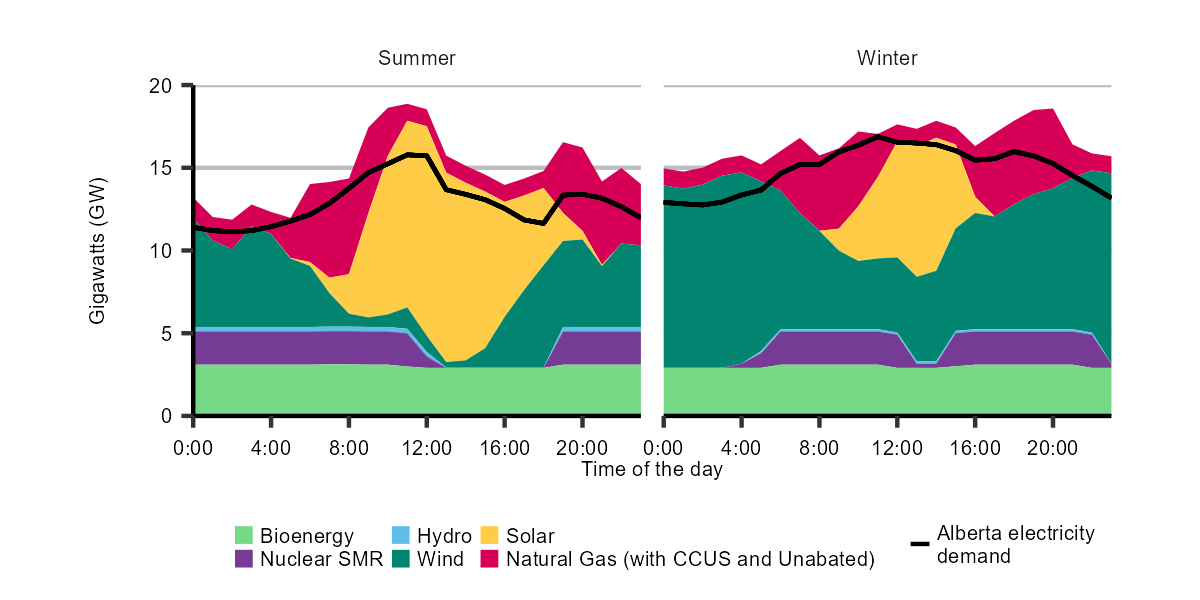

Electricity consumption can vary significantly over a day and from season to season in response to factors like the patterns of daily life and weather conditions. Wind and solar become important sources of bulk power in all our scenarios but adjustable sources of power remain critical to balancing electricity systems. Our modeling takes this necessity into account, ensuring the electricity needs of users are met, and regional electricity demand and supply are in balance on an hourly basis. Figure R.20 shows our projections of hourly electricity demand and generation on two typical days in Alberta in the summer and the winter of 2050.

Figure R.20: Example hourly electricity supply and demand in Alberta for a day in summer and winter, 2050, Global Net-zero Scenario

Description

Description: These two stacked area charts show an example of a hypothetical hourly electricity supply and demand load in summer and winter in Alberta, by energy source. The energy sources are natural gas, natural gas with CCUS, solar, wind, hydro, nuclear, and bioenergy. Each chart has a line representing Alberta electricity demand to compare to the stacked area.

The summer chart shows significant generation from solar from around 8:00 to 18:00. Solar generation is reduced in terms of length and quantity in the winter chart. Conversely, wind generation is lowest during the day in the summer and increases at night and in the early morning. Wind generation is highest in winter, especially at night and in the early morning. Natural gas and nuclear SMR generation vary to account for changing demand and variable generation levels.

Hydroelectricity

Hydroelectricity is currently the core of many provincial electricity systems, making up 90% or more of generation in Newfoundland and Labrador, Manitoba, Quebec, and BC. Hydroelectric generation is emission-free, and most facilities can vary power generation to help grids balance electricity supply and demand.

Hydroelectric generation grows steadily and at a similar rate in all three scenarios

Hydroelectric generation increases around 26% from 2021 to 2050 in each scenario. Total hydroelectric generation as a share of total Canadian generation falls from 61% in 2021 to 38% in 2050 in the Global Net-zero Scenario, as other generation sources increase more quickly. Our projections of hydroelectric power include the Site C project in BC, which is currently under construction. Our technology cost assumptions indicate that building a new hydroelectric facility is relatively expensive compared to many other options.

Most growth in hydroelectric power occurs in provinces with existing hydroelectric facilities

The geography of those regions presents more opportunities for additional hydroelectric projects or expansions. In both net-zero scenarios, hydroelectric generating capacity increases the most in Quebec (+11% from 2021 to 2050) and Manitoba (+40%). Most hydroelectricity growth comes from projects that are currently under construction and projected new developments. The remainder comes from upgrades to existing hydroelectricity units.

Nuclear

Nuclear power is a key component of Ontario and New Brunswick’s electricity systems. Nationally, nuclear power generation made up 14% of total electricity generation in 2021.

In all three scenarios, we project nuclear generation to vary over time as some of the large nuclear facilities are refurbished, meaning the units are modernized to extend their usable life. We assume Ontario’s nuclear fleet is refurbished as per the schedule laid out by the Ontario Independent System Operator in its 2022 Annual Planning Outlook.

Small modular reactors (SMRs) increase significantly in both net-zero scenarios

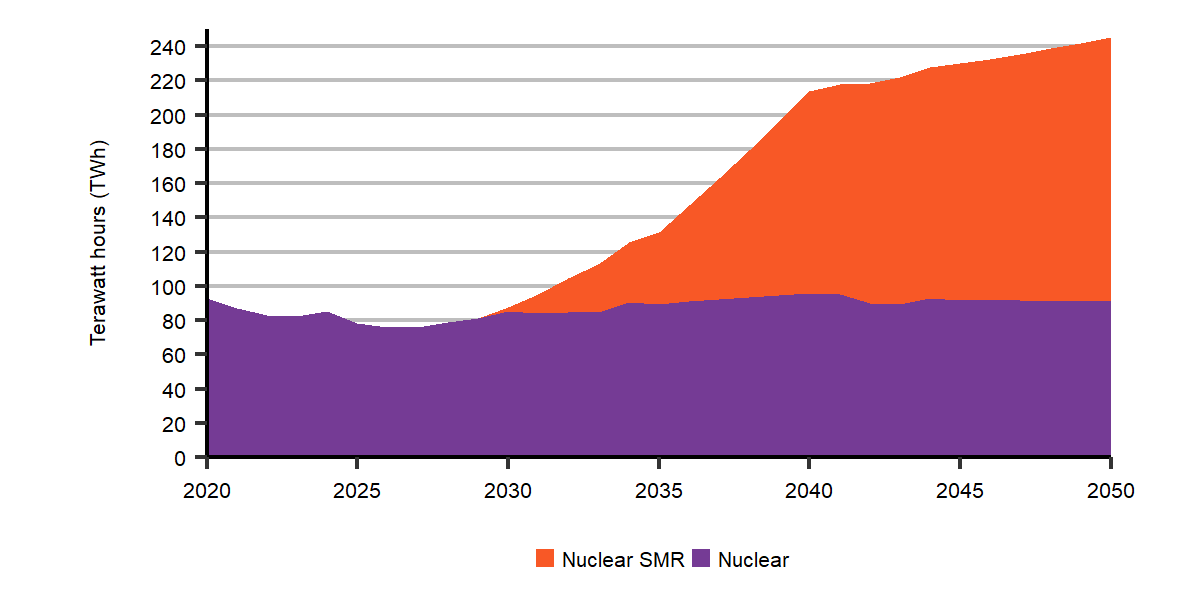

In all three scenarios, we do not project any new large-scale nuclear facilities are built over the projection period, as other generation technologies more cost-effectively meet growing electricity demand given our assumptions. However, in both net-zero scenarios, we project considerable growth for small modular reactors (SMRs), particularly in the 2035 to 2050 period. Along with renewable technologies, these nuclear SMR units play a pivotal role in Canada’s electricity system in the net-zero scenarios. By 2050, generation from SMRs make up 12% of total electricity generation by 2050 in both net-zero scenarios, with large additions in Ontario, Alberta, and BC. In the Current Measures Scenario, nuclear generation remains close to current levels through much of the projection period, with very limited growth in SMRs. Figure R.21 shows nuclear generation over the projection period in the Global Net-zero Scenario.

Figure R.21: Nuclear generation by technology, Global Net-zero Scenario

Description

Description: This stacked area chart compares nuclear and nuclear SMR electricity over the projection period in the Global Net-zero Scenario. Nuclear generation increases modestly over the projection period, and nuclear SMR grows significantly starting in the 2030s to make up most of total nuclear generation in 2050.

What if small modular reactor (SMR) technology matures less quickly and is more costly?

Canada has a long history with nuclear power, with three large-scale power facilities operating in Ontario, and one in New Brunswick. About 14%, or 82 TWh, of Canada’s electricity came from nuclear power in 2021. Recently, some governments, utilities, and power producers have focused on SMRs as a potential way to meet future electricity demand growth with a carbon-free generation option. In 2020, the Government of Canada released its SMR Action Plan, and in 2022 the governments of Ontario, Saskatchewan, New Brunswick, and Alberta released A Strategic Plan for the Deployment of SMRs. In the fall of 2022, Ontario Power Generation began site preparation activities and applied to the Canada Canadian Nuclear Safety Commission for a license to construct an SMR at the existing Darlington nuclear site.

SMRs are an emerging class of nuclear reactors that are smaller than conventional nuclear power plants in terms of size and power output. The modular aspect of SMRs means many components of a facility are factory-built, shortening plant construction times. SMRs can be used to generate electricity and to produce steam for some industrial applications such as in-situ oil sands operations.

SMR building costs fall and generation increases in the Global Net-zero Scenario

In EF2023, our electricity sector analysis relies on assumptions about the costs of various technologies. The electricity model then projects the future electricity generating mix based on the demand for electricity and the costs and characteristics of a wide range of options to generate electricity. In the Global Net-zero Scenario, we assume the capital cost of building and connecting a new SMR to the grid is 2022$9,180 per installed kilowatt (kW) of capacity in 2030, falling to 2022$7,080/kW in 2050.

Given these assumptions, and the costs and characteristics of other generating facilities, we project nuclear power generation to more than double from current levels by 2050 in the Global Net-zero Scenario. All of that growth is from SMRs, which are almost all built in the post-2035 period. About 52% of this growth occurs in Ontario, where the nuclear industry is already well-established, along with notable additions of SMRs in Quebec, BC, and Alberta.

Low SMR Case: “What if” SMR building costs remain high?

As SMRs are an emerging technology, there is considerable uncertainty as to how much the technology will ultimately cost, especially 25 years or more in the future. To explore this uncertainty, we modeled the Low SMR Case, where we assume higher capital costs for SMRs than in the Global Net-zero Scenario. In the Low SMR Case, we assume that the capital cost of building a new SMR is 2022$10,170/kW in 2030, falling to 2022$9,173/kW in 2050.