ARCHIVED – Fact Sheet - Canada’s Energy Future 2016: Energy Supply and Demand Projections to 2040 - Constrained Oil Pipeline Transportation Case Highlights

This page has been archived on the Web

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please contact us to request a format other than those available.

Canada’s Energy Future 2016: Energy Supply and Demand Projections to 2040 provides projections of Canadian energy supply and demand to the year 2040. Canada’s Energy Future 2016 includes a baseline projection, the Reference Case, based on the current macroeconomic outlook, energy price projections, and government policies and programs that were law or near-law at the time the report was prepared. EF 2016 includes additional projections that vary assumptions on energy prices, energy markets, and infrastructure. For detailed information on the Constrained Oil Pipeline Capacity Case, see Chapter 10 of the full report.

Without development of additional oil pipeline infrastructure, crude oil production grows less quickly but continues to grow at a moderate pace over the projection period.

- The Reference Case assumes that energy infrastructure is built as needed. However, the pace of development of oil pipeline infrastructure is a notable uncertainty for the Canadian energy system. The Constrained Oil Pipeline Capacity Case (Constrained Case) considers the impact on the Canadian energy system if no new major oil export pipelines are built over the projection period, including the Keystone XL, Northern Gateway, Trans Mountain Expansion and Energy East pipeline proposals.

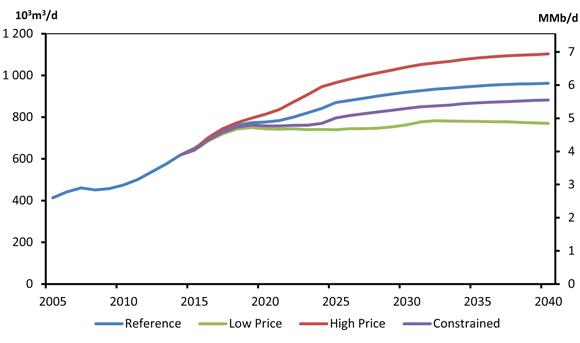

- In the Constrained Case, the increased use of rail, a more expensive shipping mode, leads to lower prices received by Canadian producers, net of transportation costs. Despite somewhat lower prices compared to the Reference Case, crude oil production continues to grow as many projects remain profitable. Oil production in the Constrained Case reaches 882 10³m³/d (5.6 MMb/d) by 2040, eight per cent lower than the Reference Case. Crude oil shipped by rail grows substantially over the projection, reaching 187 10³m³/d (1.2 MMb/d) by 2040.

Total Oil Production, Reference, High Price, Low Price and Constrained Cases

- Total Canadian production in the Constrained Case grows quicker than in the Low Price Case, and production is 15 per cent higher than the Low Price Case by 2040. This suggests that although pipeline infrastructure may impact Canadian oil production, it is one of many factors that may do so. The High and Low Price cases suggest that crude oil prices, driven by global supply and demand dynamics, are also an important - perhaps the most important - determinant of Canadian production.

- In the Constrained Case, Canadian crude oil production continues to grow. However, delayed projects and reduced investment over the projection period reduce total Canadian crude oil production in 2040 by about 80 10³m³/d (506 Mb/d), or eight per cent, compared to the Reference Case. About 84 per cent of the difference is due to reduced bitumen production, with the remainder attributed to lower conventional production.

- The oil exports in the Constrained Case are based on projected crude oil production, domestic refinery consumption and the need for diluent. Domestic refinery consumption of crude oil is the same as in the Reference Case. Due to less oil production (less to be diluted) and more crude-by-rail transportation (which requires less diluent than pipeline transportation), the need for imported condensates in 2040 is reduced from about 127 10³m³/d (800 Mb/d) in the Reference Case to about 104 10³m³/d (654 Mb/d) in the Constrained Case.

- In the Constrained Case, energy use in oil sands, including upgrading, is 2 185 PJ by 2040, eight per cent lower than in the Reference Case. In the conventional sector, energy use is 175 PJ by 2040 or six per cent lower than in the Reference Case.

- The price projections for WTI and Brent in the Constrained Case are the same as in the Reference Case. However, Canadian net-back prices, WCS and MSW, are lower in the Constrained Case when export pipeline capacity is insufficient to transport supply.

- This case assumes that the U.S. Gulf Coast will be the primary market for growing heavy crude exports, and that light crude oil exports compete with Bakken oil supply in the Midwest and East Coast markets.

- In the Reference Case, the WCS price is assumed to be approximately 82 per cent of the WTI price, which accounts for unconstrained transportation costs and the difference in quality between WCS and WTI. For the Constrained Case, in years when the pipeline capacity is insufficient to move oil supply, the WTI-WCS differential widens relative to the Reference Case by about US$10/bbl. This is the approximate extra cost that would be incurred to transport Canadian heavy crude to the U.S. Gulf Coast by rail instead of by pipeline.

- For light oil, the WTI-MSW price differential is US$5.50/bbl in the Reference Case. This is approximately the transportation cost to ship light crude oil from Edmonton to Cushing, Oklahoma. In the Constrained Case, the WTI-MSW differential increases relative to the Reference Case by about another US$5/bbl, starting in 2021. The U.S. has an abundant supply of domestic light crude oil. In this analysis, when light oil transportation capacity is insufficient, MSW must decline to compete for market share with oil from the U.S. Bakken transported on the Enbridge pipeline system.

- The lower WCS and MSW prices in the Constrained Case reduce oil-directed capital expenditure in western Canada. Delays to project start-up dates for some oil sands projects are also incorporated in the medium term. Over the projection period capital expenditures are reduced by 15 per cent in the conventional oil sector, and by nine per cent in the oil sands.

- Date modified: